Is Taiwan Semiconductor Stock a Buy Now?

Taiwan Semiconductor Manufacturing (NYSE: TSM) is on a roll. On the heels of a three-year slump in chipmaking services, TSMC is facing unprecedented production demand. The artificial intelligence (AI) surge that started two years ago seems to have legs for years, and that's not even the whole story -- modern cars need a ton of processors, and the smartphone market is also coming back from a long downturn.

So, TSMC's stock has doubled in 2024. Its market cap has been hovering around the rare $1 trillion level since October.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

At the same time, TSMC shares are trading at lofty valuation ratios. Is the stock overvalued today, or is TSMC still a great buy at today's high prices?

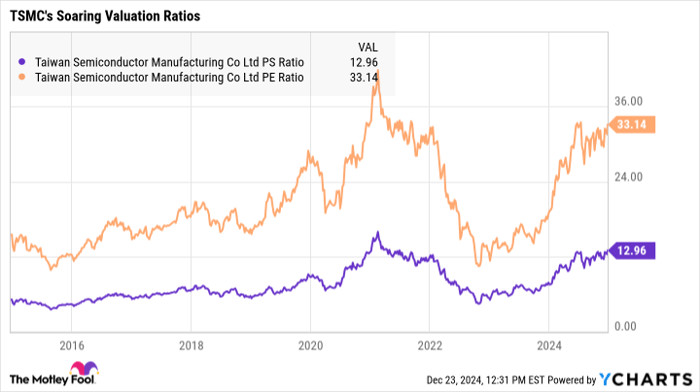

TSMC looks expensive

The company works in a hardware manufacturing industry. It's a high-tech business, far removed from building homes, tractors, or industrial machinery, but it's still a relatively low-margin business that requires very large capital investments. Chipbuilding facilities don't grow on trees, you know.

TSMC's capital expenses added up to $24.6 billion over the last four quarters. That's more than Apple, Tesla, and Nvidia spent on capital investments -- together.

Companies with costly assets tend to grow fairly slowly, and their stocks often trade as very modest valuation ratios. The 10 largest industrial stocks, for example, currently trade at an average price-to-sales ratio (P/S) of 2.5. TSMC's stock is worth 12.8 times sales. It's the same story with price-to-earnings or price-to-free cash flows -- TSMC's stock is soaring at historically high ratios, and it looks expensive next to companies with similar business models.

TSM PS Ratio data by YCharts

Why you still might want to buy this pricey stock

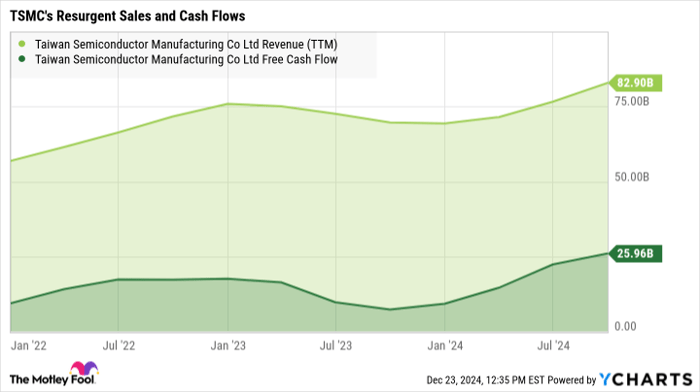

The company backs up its pricey stock valuation with robust business results.

After a temporary dip amid the recent shortage of semiconductor materials and engineers, TSMC's sales and profits are soaring again. Revenues rose 39% year over year in the recently reported third quarter. Net income jumped 54% higher in the same period, and cash profits really soared. TSMC's free cash flows nearly tripled, rising 172% to $185 billion Taiwanese dollars (approximately $5.7 billion in U.S. dollars).

TSM Revenue (TTM) data by YCharts

So you may be paying a premium for TSMC shares, but it's a world-class business and arguably worth every penny of its high stock price. Growth-oriented valuation metrics look quite reasonable with a forward-looking P/E ratio of 23 times next-year estimates and a price-to-earnings-to-growth ratio (PEG) of 1.1. Both figures suggest that the current stock price is just about right -- neither terribly expensive nor particularly cheap.

TSMC is a solid buy -- but not for every investor

The Taiwanese chipmaking giant is a tempting buy in many ways. TSMC is a good way to invest in the AI boom without picking a winner in the chip-design battles. Remember, nearly all the leading AI accelerator specialists rely on TSMC and others to actually make the physical products. Whoever dominates the hardware market in the long run, TSMC will probably benefit from the entire AI sector's success.

But you need to be comfortable with the stock's growth-based valuation first. Otherwise, I'd recommend a lower-priced chipmaker, or perhaps an undervalued provider of AI software and services instead. TSMC may be a fine growth investment, but it's not every Wall Street stroller's cup of refined silicon.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $363,593!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $48,899!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $502,684!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 23, 2024

Anders Bylund has positions in Nvidia. The Motley Fool has positions in and recommends Apple, Nvidia, Taiwan Semiconductor Manufacturing, and Tesla. The Motley Fool has a disclosure policy.

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

USD Dollar Trend Forecast: Dollar Index Falls Below 97.0 to 4-Year Low, Will the Dollar Continue To Fall or Bottom Out in 2026?

TradingKey - In January 2026, the US Dollar Index continued its downward trend from 2025, officially breaking below the key 97.0 level and reaching a low of 95.5, marking a nearly four-year low since February 2022.