Applied Materials Q3 Earnings: AI Demand Soars, but Cautious Guidance Triggers After-Hours Selloff

.jpg)

TradingKey - Applied Materials, Inc. (NASDAQ: AMAT) announced its Q3 FY2025 earnings on August 14, 2025, after market close, reporting strong revenue fueled by AI-related semiconductor demand, which beat expectations. However, cautious Q4 guidance, including EPS below analyst estimates, fell short of investor optimism and alongside concerns over China trade restrictions and margin pressures, triggered a 14% drop in after-hours trading.

Source: TradingKey

Key Financial Results

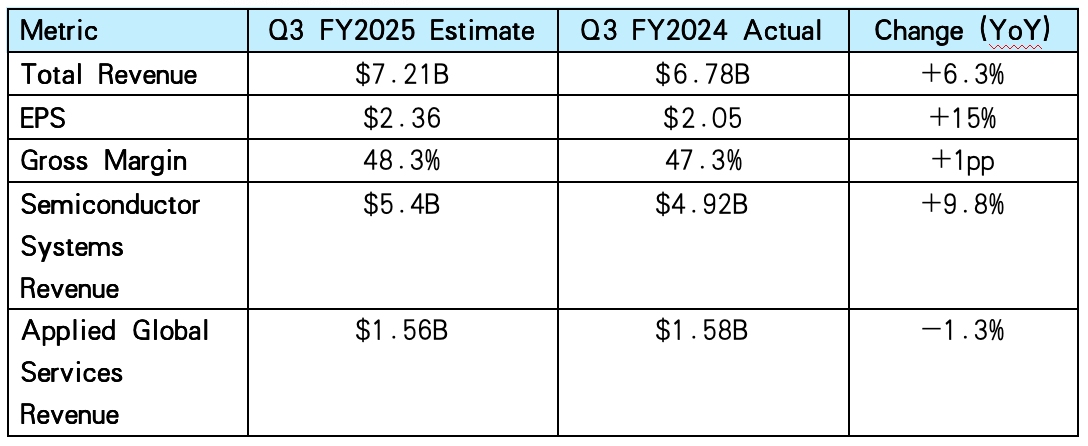

Applied Materials delivered robust Q3 performance, with revenue and EPS growth driven by its Semiconductor Systems segment.

.jpg)

Source: Applied Materials, TradingKey

Segment and Regional Performance

Semiconductor Systems: generating $5.43 billion in revenue, a 10% increase YoY. This growth was fueled by strong demand for advanced node equipment, including 3nm and 2nm technologies, and high-bandwidth memory essential for AI infrastructure. Key products like the SIM3 Magnum Etch System and cold field emission e-beam tools contributed significantly, reflecting strong market acceptance and competitive positioning.

Applied Global Services and Display Segment: The Applied Global Services segment revenue increased modestly to $1.60 billion in Q3 FY2025 from approximately $1.58 billion a year ago, reflecting steady demand for upgrades and spare parts despite ongoing U.S. export restrictions on 200mm wafer equipment to China. The Display segment grew by about 5% to $263 million, supported by rising OLED demand and advances in emerging display technologies. While still a smaller portion of total revenue, the Display segment’s operating margin improved significantly year-over-year from 6.4% to 23.6%.

Geopolitical and Trade Dynamics: China accounted for approximately 35% of revenue in Q3, slightly higher than the prior year, highlighting its ongoing significance despite export control challenges. Taiwan and South Korea contributed about 25% and 16%, respectively. Management noted that licensed sales to multinational companies in China provided revenue support; however, Q4 guidance reflects cautious visibility amid trade tensions and capacity adjustments in the region.

Financial Summary: Applied Materials demonstrated strong operational execution, with improved gross margins reflecting effective cost management and a favorable product mix. The company’s robust free cash flow of $2.05 billion shows solid cash generation capabilities, which continue to support disciplined capital returns through share repurchases and dividends. Management’s emphasis on maintaining financial flexibility amid a complex macroeconomic and geopolitical environment remains a key focus.

Guidance and Management Commentary

Q4 FY2025 Guidance: Applied Materials expects Q4 revenue around $6.7 billion (±$500 million), down 5% YoY, with non-GAAP EPS of $2.11 (±$0.20), a 9% decline. Gross margin is projected near 48.1%, reflecting challenges from China capacity digestion, customer timing, and trade uncertainties.

Management Insights: CEO Gary Dickerson emphasized AI-driven demand and the company’s leadership in gate-all-around transistors and advanced packaging, stating, “Our broad portfolio positions us to capture share in high-growth AI and advanced node markets.” CFO Brice Hill noted supply chain diversification progress but cautioned on China-related headwinds and margin pressures from increased R&D spending. The company reaffirmed its commitment to the $10 billion share repurchase program and a quarterly dividend of $0.46, yielding 1.0%.

Conclusion and Outlook

Applied Materials delivered strong Q3 FY2025 results, led by robust AI-driven demand in its Semiconductor Systems segment. However, a 14% after-hours decline reflected investor concerns over weaker-than-expected Q4 guidance and persistent China-related trade uncertainties. Despite near-term challenges, Applied’s leadership in advanced AI technologies and its diversified geographic footprint position it well for long-term growth in a semiconductor market forecasted to grow 10% to 15% annually. Following the selloff, shares trade at a forward P/E of approximately 17x, potentially offering a compelling entry point for long-term investors in a leading semiconductor equipment company.

TradingKey - Applied Materials, Inc. (NASDAQ: AMAT) will release its Q3 FY2025 earnings on Thursday, August 14, 2025, after market close, with an earnings call at 4:30 p.m. Pacific Time.

Since April 2025, the stock has rebounded sharply from the $120 level, hitting a high of nearly $200 in June, driven by investor enthusiasm driven by demand for AI-related semiconductors. It then saw a pullback to the mid-$180s as of early August, influenced by broader market volatility and some profit-taking. While U.S.-China trade restrictions and regulatory risks remain factors, investor caution ahead of Q3 guidance and general macroeconomic concerns also contributed. Despite this modest correction, Applied Materials’ valuation remains supported by solid demand fundamentals, with shares trading around a P/E of 22x heading into the earnings release.

Source: TradingKey

Market Forecast

Source: Applied Materials, Yahoo Finance, Finviz, TradingKey

Source: Applied Materials, Yahoo Finance, Finviz, TradingKey

Key Investor Focus Areas

AI-Driven Semiconductor Demand and Segment Performance: The Semiconductor Systems segment is expected to remain the main growth driver, fueled by strong demand for AI infrastructure, especially advanced nodes like 3nm and 2nm, and high-bandwidth memory (HBM) products. Foundry/logic and DRAM customers will continue to be key revenue contributors. The Display segment may see further recovery through rising OLED demand, potentially supporting revenue and margins. Commentary on adoption of new technologies such as the SIM3 Magnum Etch System and cold field emission e-beam tools will be important for gauging market share expansion.

China Exposure and Geopolitical Navigation: Revenue from China has fallen from roughly 43% a year ago to about 25% recently due to U.S. export restrictions on advanced semiconductor equipment. Growth in Taiwan and South Korea is expected to partially offset this decline. Management’s insights on handling new trade restrictions, licensing, and geopolitical risks will be critical to assess global revenue stability and diversification.

Capital Allocation and Margin Outlook: Q3 gross margin is projected to slightly contract to around 48.3% from Q2, reflecting cost pressures and product mix changes. Strong cash flow is expected to support continued share repurchases under the $10 billion buyback authorization and dividend payments. Updates on buyback execution, dividend policy, and management’s outlook on long-term cash flow and financial health will be key watch points in the earnings call.

Recent Developments and Regulatory Environment

Advances in Semiconductor Technology: Applied Materials is advancing AI-focused technologies, including gate-all-around transistors and advanced packaging. The SIM3 Magnum Etch System, launched in early 2024, has generated over $1.2 billion in revenue, showing strong market acceptance.

Trade Restrictions and Supply Chain Resilience: U.S. export controls continue to limit equipment sales to China, affecting mature logic and 200mm wafer businesses. Applied is working to mitigate risks through supply chain diversification, though further restrictions remain a concern.

Government Initiatives and Industry Dynamics: Government programs like the CHIPS Act boost capital spending focused on supply chain security and domestic manufacturing, increasing regulatory scrutiny. Innovation in materials and emerging chip architecture offers opportunities but intensifies competitive pressures.

Market Outlook and Growth Drivers: The semiconductor equipment market is expected to grow by over 20% annually, driven by AI, 5G, and IoT demand. Applied’s strengths in deposition and etch tools position it well for advanced node and 3D NAND investments. However, softening consumer electronics demand and competition from ASML and Lam Research could temper growth.

Conclusion

Applied Materials’ Q3 FY2025 earnings will test its ability to sustain AI-driven growth amid geopolitical and margin pressures. Strong Semiconductor Systems performance and Display segment recovery could drive stock price up if revenue exceeds the guidance range. However, China-related trade restrictions and a projected gross margin dip pose near-term risks. With a robust portfolio and leadership in key technology inflections, Applied remains well-positioned for long-term growth, but execution in navigating trade dynamics will be critical to maintaining investor confidence.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.