Sensor products maker Sensata beats Q3 revenue, adjusted EPS expectations

Overview

Sensata Q3 revenue beats analyst expectations despite a 5.2% yr/yr decline

Adjusted EPS for Q3 beats consensus, remaining consistent with prior year

Adjusted operating income for Q3 exceeds analyst estimates

Outlook

Sensata expects Q4 2025 revenue of $890 mln to $920 mln

Sensata forecasts Q4 2025 adjusted EPS of $0.83 to $0.87

Result Drivers

DIVESTITURES AND PRODUCT LIFECYCLE - Revenue decline attributed to divestitures and product lifecycle management actions

CLEAN ENERGY POLICY IMPACT - Operating loss includes $259 mln in charges due to changes in clean energy policy and emissions regulations

ORGANIC REVENUE GROWTH - Organic revenue increased by 3.1% compared to Q3 2024

Key Details

Metric | Beat/Miss | Actual | Consensus Estimate |

Q3 Revenue | Beat | $932 mln | $917.20 mln (15 Analysts) |

Q3 Adjusted EPS | Beat | $0.89 | $0.85 (14 Analysts) |

Q3 EPS |

| -$1.12 |

|

Q3 Adjusted operating income | Beat | $179.60 mln | $137.30 mln (7 Analysts) |

Q3 Free Cash Flow |

| $136.20 mln |

|

Q3 Operating income |

| -$122.90 mln |

|

Analyst Coverage

The current average analyst rating on the shares is "hold" and the breakdown of recommendations is 8 "strong buy" or "buy", 9 "hold" and 1 "sell" or "strong sell"

The average consensus recommendation for the electronic equipment & parts peer group is "buy."

Wall Street's median 12-month price target for Sensata Technologies Holding PLC is $39.00, about 19% above its October 27 closing price of $31.60

The stock recently traded at 9 times the next 12-month earnings vs. a P/E of 9 three months ago

Press Release: ID:nBw8k7JNya

For questions concerning the data in this report, contact Estimates.Support@lseg.com. For any other questions or feedback, contact RefinitivNewsSupport@thomsonreuters.com.

Related Articles

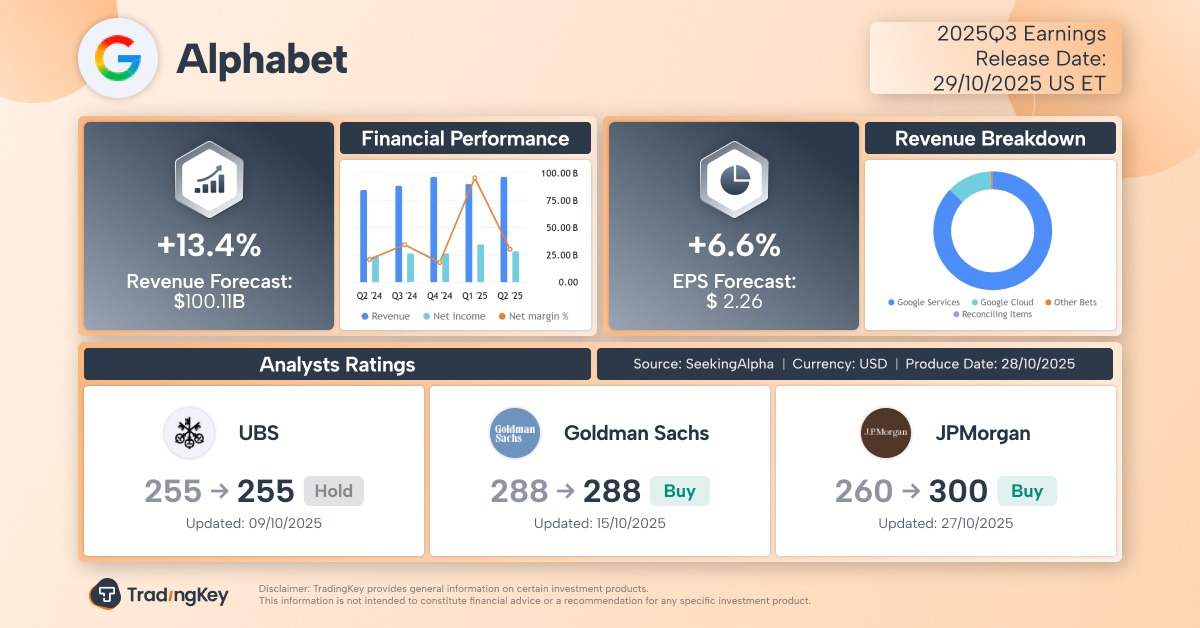

Google Q3 Earnings Preview: Ads as Foundation, AI as Sword — Can TPU Commercialization Drive a Re-Rating?

TradingKey - Alphabet (GOOG, GOOGL), the AI and cloud powerhouse, will report its Q3 2025 earnings after market close on Wednesday, October 29. Analysts expect another strong quarter driven by resilient core advertising growth, surging AI cloud demand, and the long-awaited commercialization of its

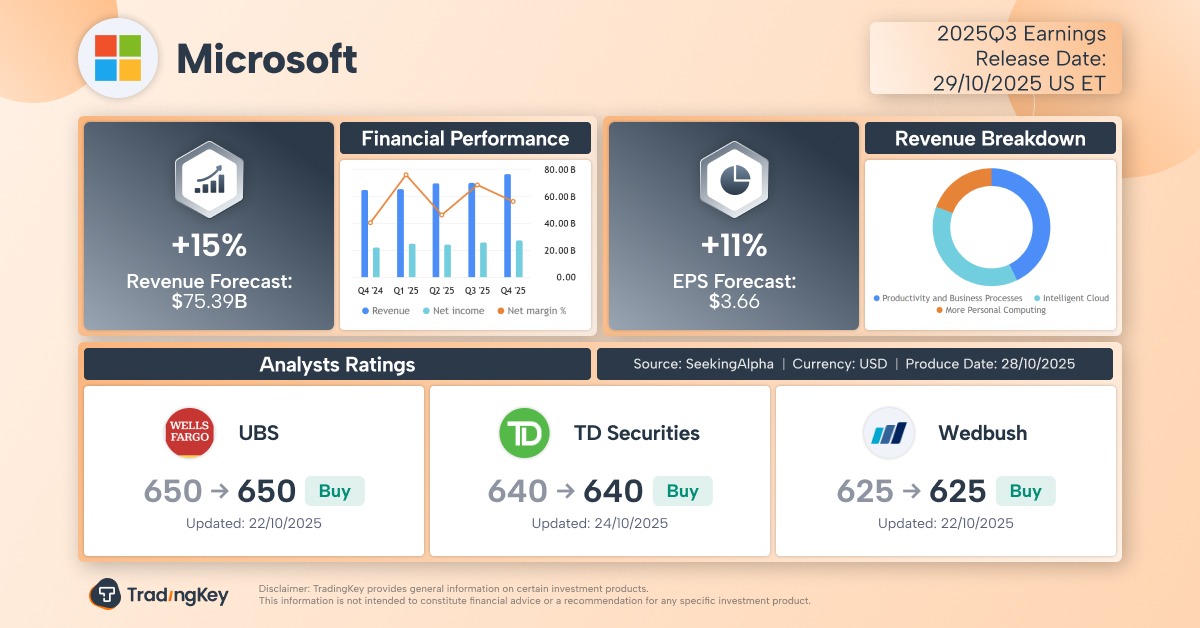

Microsoft Q1 Earnings Preview: AI-Powered Cloud Growth Fuels Wall Street’s “Zero Sell” Consensus

TradingKey - AI giant Microsoft (MSFT) will report its Q1 FY2026 earnings (natural Q3 2025) on October 29. While Microsoft’s stock has shown little movement since its last strong earnings beat, Wall Street analysts expect another quarter of AI-driven cloud growth outpacing peers, with EPS

Fed’s October Rate Cut: "Equity-Gold Allocation" as the Optimal Strategy – Stock ETFs or Individual Stocks? Gold ETFs or Gold Stocks?

TradingKey - Overbought technical conditions triggered profit-taking, driving the sharp declines in U.S. stocks on 10 October and gold on 21 and 27 October.

Fed October Meeting Preview: Rate Cuts to Break 4% and an Earlier End to QT

TradingKey - At the Federal Reserve meeting ending Wednesday, October 29, policymakers are widely expected to follow through on the rate-cutting path outlined in the September Summary of Economic Projections — delivering a 25-basis-point rate cut, the second of 2025. Simultaneously, with bank