Google Q3 Earnings Preview: Ads as Foundation, AI as Sword — Can TPU Commercialization Drive a Re-Rating?

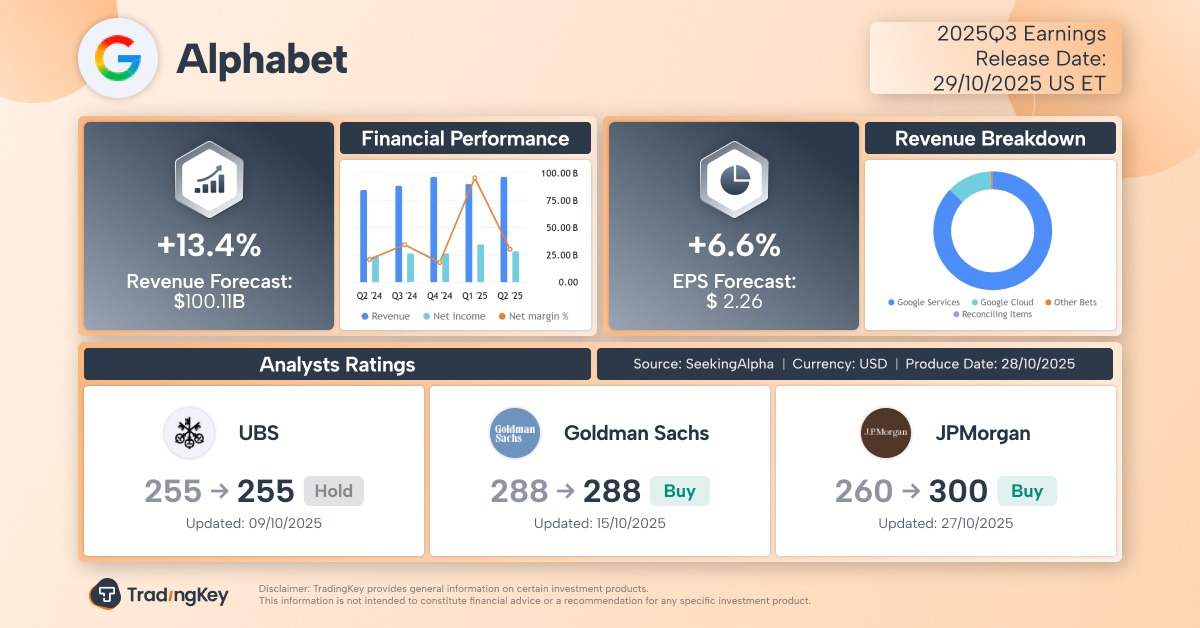

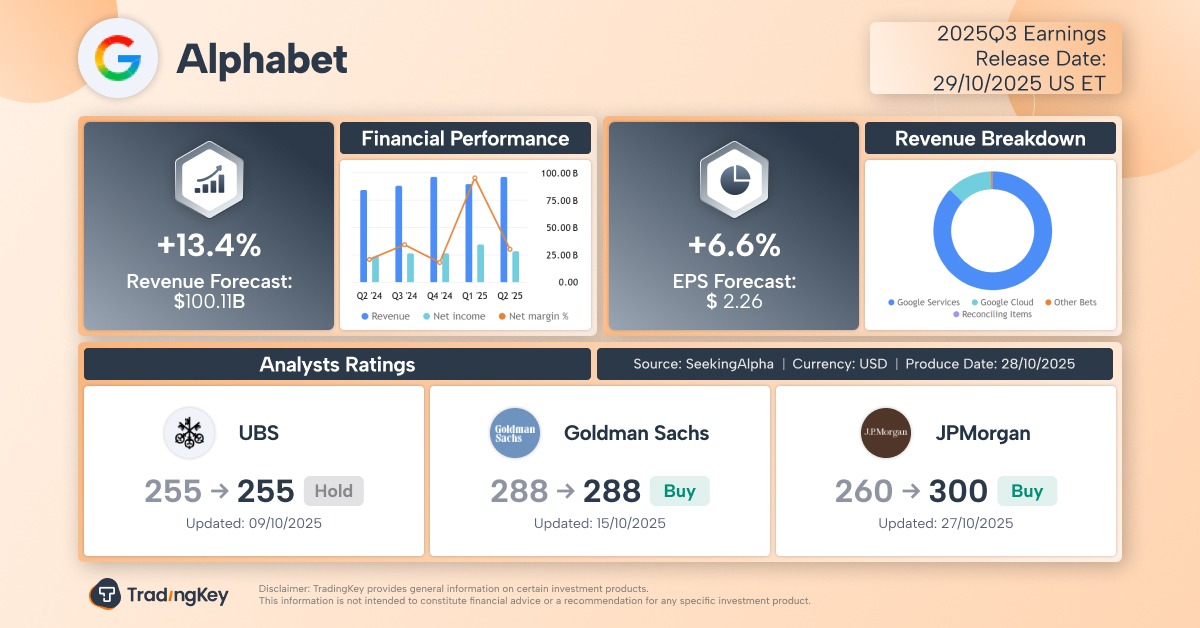

TradingKey - Alphabet (GOOG, GOOGL), the AI and cloud powerhouse, will report its Q3 2025 earnings after market close on Wednesday, October 29. Analysts expect another strong quarter driven by resilient core advertising growth, surging AI cloud demand, and the long-awaited commercialization of its Tensor Processing Unit (TPU) chips — potentially offering Wall Street a fresh catalyst to revalue Google’s stock. With a market cap now exceeding $3 trillion, further upside may still lie ahead.

According to Seeking Alpha, analysts forecast:

- Revenue: $100.11 billion, up 13.4% YoY

- EPS: $2.26, up 6.6% YoY

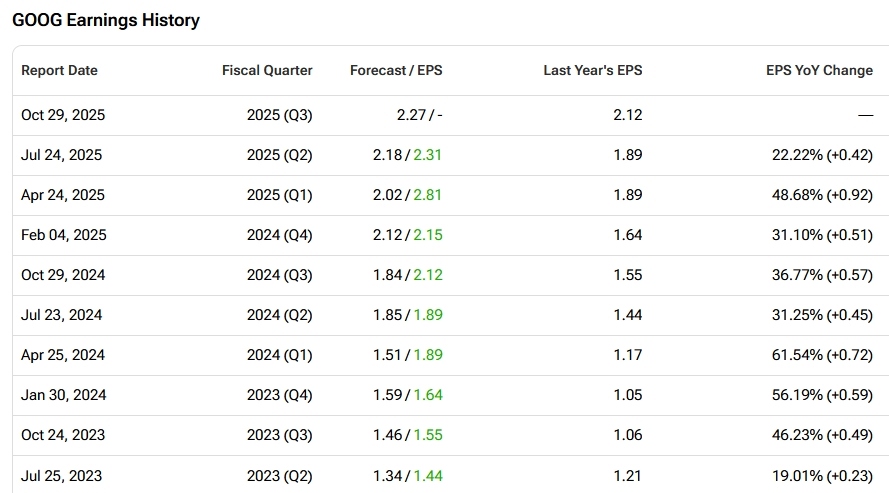

A Track Record of Beating Expectations

Per Tipranks, Google has beaten EPS estimates in nine consecutive quarters, underscoring that Wall Street consistently underestimates the company’s profitability and growth potential.

Analysts adopted a conservative EPS outlook for Q3 due to:

- Anticipated higher-than-expected ad spending

- Profit erosion from massive AI capital expenditures

- Rising R&D costs

Google’s Past EPS Performance, Source: Tipranks

The slight gap between revenue and EPS growth reflects expected cost increases — but these investments are justified as essential for maintaining Google’s competitive edge. Given Google’s historically strong return on invested capital (ROIC), the long-term payoff from new initiatives remains promising.

From Search Giant to AI Leader

Today, Alphabet’s business spans search, digital advertising, cloud computing, and AI software and hardware. Its three main revenue segments are:

- Google Services (Search, YouTube ads) – 85.6% of Q2 revenue

- Google Cloud – 14.13%

- Other Bets

Despite rising competition from AI-powered browsers, analysts expect Google’s core ad business to grow over 10% again in Q3. In the cloud race, Google continues to gain ground with ~30% annual growth, closing the gap on leader Amazon AWS.

A major milestone: After 10 years of development, Google’s TPU chip is finally achieving meaningful commercial traction — highlighted by Anthropic’s tens of billions of agreement to deploy 1 million TPUs for training its Claude AI models.

Advertising: Google’s Lifeblood

In Q2, Google’s total ad revenue rose 10.4% YoY to $71.3 billion, with both Search and YouTube ads exceeding expectations.

For Q3, analysts project:

- Total ad revenue: +10% YoY to $72.45 billion

- YouTube ad revenue: +12.4% YoY to $10.02 billion

This resilience persists despite macro uncertainty and tariff risks.

Justin Post, Bank of America analyst who recently raised Google’s price target from $252 to $280, said that Google’s ad business will continue steady growth. Even if organic search traffic dips slightly, gains across key verticals more than offset it.

AI Browsers Challenge Chrome — But Google Fights Back

With Perplexity’s Comet and OpenAI’s Atlas launching AI-native browsers, concerns have grown that they could erode Chrome’s dominance and reduce reliance on traditional search.

But Google is pushing back with data. CEO Sundar Pichai noted in July that monthly active users of its AI Overviews feature surged from 1.5 billion in Q1 to over 2 billion — proving AI is expanding, not replacing, search behavior.

Embedding Gemini AI into search isn’t cannibalizing traffic — it’s enhancing keyword-based ad monetization.

According to StatCounter, Google still holds over 90% of the global search market — far ahead of Bing (4.08%) and Yandex (1.65%).

Cloud Growth & TPU Breakthrough: A New Narrative

While Amazon AWS leads the cloud market with ~30% share, Microsoft Azure (~20%) and Google Cloud (~13%) are rapidly catching up.

Visible Alpha forecasts for Q3:

- Google Cloud: +30.1%

- Azure: +38.4%

- AWS: +18%

Bank of America expects Google Cloud to grow 32% in Q3, with AI-driven efficiency boosting core margins. Zacks Investment Research projects cloud revenue of $14.66 billion, up 29.1% YoY.

The real story: TPU commercialization. The Anthropic deal — deploying 1 million TPUs — marks a turning point. It validates Google’s decade-long investment in custom silicon and could generate tens of billions in revenue over time.

Beyond Anthropic, TPU customers include Safe Superintelligence, Salesforce, and Midjourney.

This isn’t just about money — it’s about expanding Google’s AI ecosystem. The “King of Search” is proving it can compete with Nvidia in AI hardware, carving out a specialized moat in AI workflows beyond general-purpose GPUs.

Justin Patterson, KeyBanc analyst, said that this deal proves Google Cloud is gaining share. TPUs are strategically vital.

Morgan Stanley called it a major validation of Google’s AI cloud strategy — forecasting it could add 100–900 basis points to cloud revenue growth in 2026 and beyond.

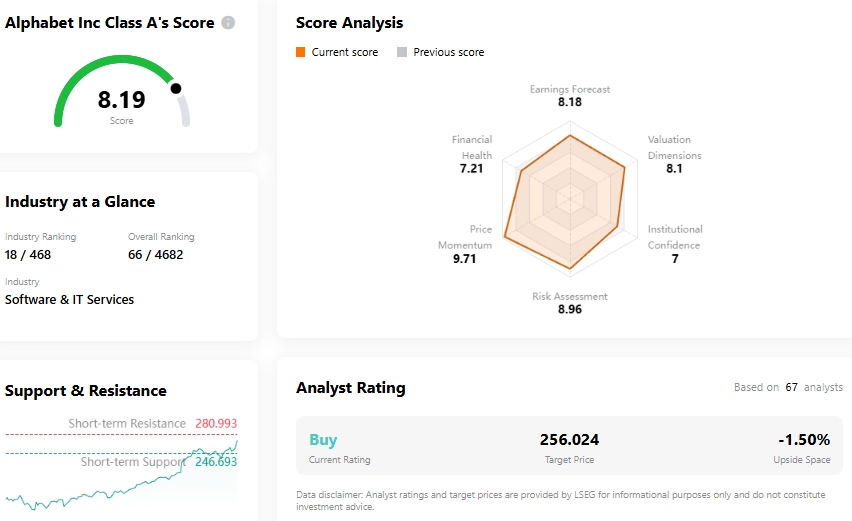

Is Google Undervalued?

Per TradingKey, the Wall Street consensus price target is $256.02 — actually below its current price of $269.27. Yet, Google scores 8.19/10 on TradingKey’s stock rating system — outperforming Nvidia (8.11), Amazon (8.01), and Tesla (7.14).

Google Stock Score, Source: TradingKey

Year-to-date, Google shares are up 42.25%, outpacing the S&P 500’s 16.89%. Benefiting from easing trade tensions and strong Q3 expectations, Google recently hit an all-time high, crossing the $3 trillion market cap threshold.

JPMorgan noted Google is the second-best performer among the Magnificent Seven this year. After an 80%+ rebound since April, investor discussions now focus on what’s next.

With the DOJ’s antitrust ruling on search removing a major overhang, strong financial execution, and leadership in AI innovation, JPMorgan believes Google still has room to run.

BMO Capital Markets added that Google Cloud is well-positioned to gain share, thanks to deep AI integration and growing AI-native workloads.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.