20-Year JGB Auction Holds Up — Fiscal and Technical Recession Risks Loom

TradingKey - On July 10, Japan’s 20-year government bond auction concluded without major disruptions. The bid-to-cover ratio and tail spread did not show significant weakness — but amid concerns over economic technical recession and rising fiscal spending, investors remain cautious.

The results showed:

- A bid-to-cover ratio of 3.15, below the 12-month average, but the highest since March

- A tail spread of 0.18 basis points, the narrowest since January, indicating stronger-than-expected demand

As previously reported by TradingKey, this auction was closely watched ahead of the July 20 Upper House elections, as its outcome could signal shifts in political and fiscal expectations. A weak result would likely trigger a chain reaction of selling pressure on long-term bonds.

Analysts at SMBC Nikko Securities described the auction outcome as neutral to slightly positive, with both indicators falling within an acceptable range.

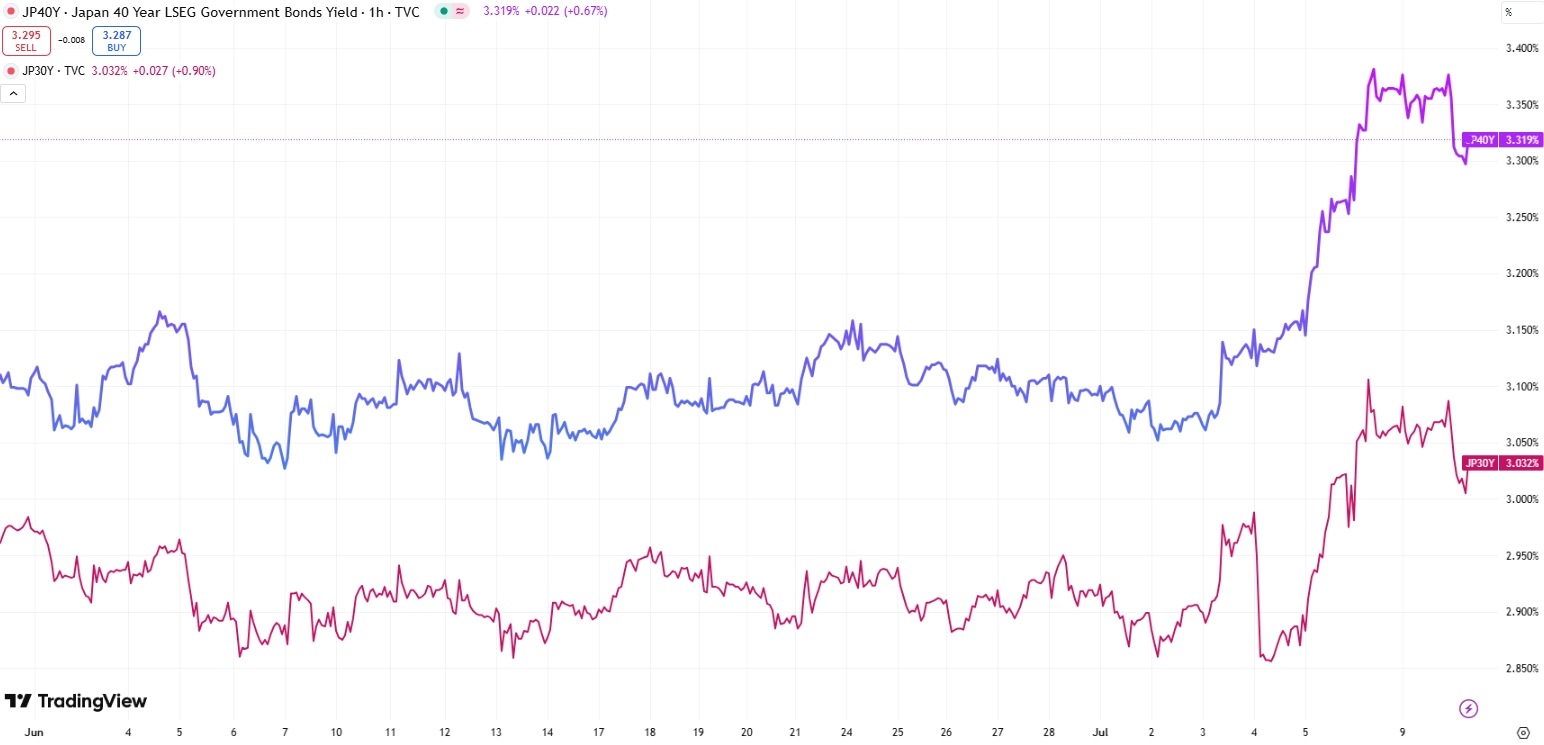

They noted that the results, along with signs of stabilization in bond prices the day before, may help calm markets — at least temporarily. Long-end yields remain attractive, while 30-year and 40-year JGB yields have also stabilized after prior spikes.

30-Year and 40-Year JGB Yields, Source: TradingView

Following the auction, the yield on the 20-year JGB fell 1.7 bps to 2.491%, the 30-year yield dropped 3 bps to 3.033%, and the 40-year yield declined 3.4 bps to 3.322%.

Despite the rebound in bond prices, yields remain near record highs. Bloomberg analysts noted that while the auction appeared stable on the surface, investor caution toward long-dated Japanese debt will persist as the Upper House election approaches — and as fiscal expansion risks loom.

Institutional Investors Remain Cautious Amid Fiscal Concerns

According to NHK News, Japan’s ruling coalition — formed by the Liberal Democratic Party (LDP) and Komeito — lost its majority in the House of Representatives earlier this year. Its performance in the upcoming House of Councillors election will be crucial.

Given the potential negative impact of Trump’s tariffs on the economy, market speculation is growing that the government may adopt more aggressive fiscal stimulus — with opposition parties proposing even deeper tax cuts.

Data showed that real wages in May fell 2.9% YoY, worse than the expected 1.7% decline — putting further pressure on future consumption and growth outlook.

Japan and the U.S. are still in active negotiations over key tariff issues — especially in the automotive sector — in an effort to avoid a full-blown technical recession, after Japan’s real GDP declined 0.7% YoY in Q1 2025.

AXA Investment said that major institutional investors like banks and life insurers are unlikely to actively participate in long-term JGB auctions for now — as they await clarity from the July 20 election and its policy implications.

Meiji Yasuda Life Insurance also revealed that due to rising yields and increased issuance pressure, the firm plans to avoid aggressive investments in ultra-long JGBs over the next one to two years.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.