Vertiv Holdings Co Stock (VRT) Moved Up by 7.52% on Jun 30: What Investors Need To Know

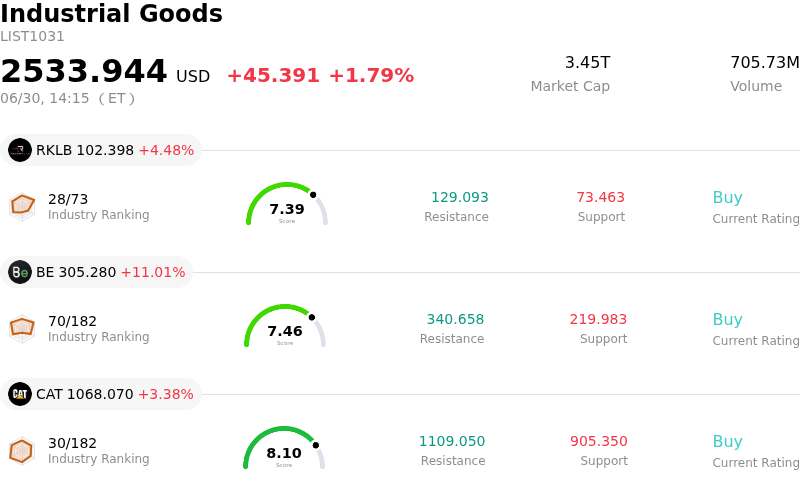

Vertiv Holdings Co (VRT) moved up by 7.52%. The Industrial Goods sector is up by 1.79%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Rocket Lab USA Inc (RKLB) up 4.48%; Bloom Energy Corp (BE) up 10.76%; Caterpillar Inc (CAT) up 3.37%.

What is driving Vertiv Holdings Co (VRT)’s stock price up today?

Vertiv Holdings Co (VRT) experienced strong upward momentum on the back of monumental international capital expenditure commitments and positive fundamental catalysts. The key driver for the surge was the South Korean government's announcement of a massive, multi-year state and corporate investment plan exceeding one trillion dollars to build advanced semiconductor fabrication plants and artificial intelligence data centers. Out of this total, corporate giants including SK Group, Naver, and GS Group are projected to invest hundreds of billions of dollars specifically into AI data centers. Because Vertiv maintains a strong market presence in Asia and its high-performance power and thermal infrastructure is deeply integrated into NVIDIA's computing architecture, investors anticipate a substantial increase in bookings for the company as these regional buildouts materialize.

Market optimism was further reinforced by Vertiv's continuous expansion of its liquid cooling capabilities to support high-density AI hardware. The integration of ThermoKey, a specialized manufacturer of heat-rejection systems acquired earlier in June, is highly valued by investors. Traditional air cooling systems are increasingly inadequate for handling the extreme heat densities of next-generation AI processors. Consequently, the market is actively rewarding Vertiv's rapid consolidation of the liquid cooling supply chain as hyperscalers scale their infrastructure.

Additionally, macro data center demand remains robust as the market approaches the second-quarter earnings season. Vertiv has already demonstrated rapid growth and high visibility, carrying a backlog of over fifteen billion dollars. In tandem with raised full-year 2026 revenue guidance and strong expected organic net sales growth, the company's positioning as a structural beneficiary of the AI cycle outweighed recent industry rotation pressures and valuation concerns. Despite persistent risks such as supply-chain disruptions and potential margin pressures from rising component costs, the combination of massive international infrastructure investments and Vertiv's technological leadership fueled strong demand for the stock.

Technical Analysis of Vertiv Holdings Co (VRT)

Technically, Vertiv Holdings Co (VRT) shows a MACD (12,26,9) value of 0.006, indicating a neutral signal. The RSI at 46.827 suggests neutral condition and the Williams %R at 61.864 suggests sell condition. Please monitor closely.

Media Coverage of Vertiv Holdings Co (VRT)

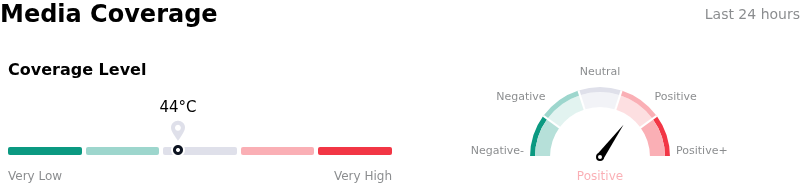

In terms of media coverage, Vertiv Holdings Co (VRT) shows a coverage score of 44, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Vertiv Holdings Co (VRT)

Vertiv Holdings Co (VRT) is in the Industrial Goods industry. Its latest annual revenue is $10.23B, ranking 17 in the industry. The net profit is $1.33B, ranking 13 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $368.34, a high of $500.00, and a low of $188.00.

More details about Vertiv Holdings Co (VRT)

Company Specific Risks:

- Vulnerability to Broader AI and Semiconductor Liquidations: Vertiv's stock remains highly sensitive to systemic shocks in the AI supply chain, as evidenced by a sharp 11.1% single-session decline triggered by regulatory interventions in South Korea's leveraged chip exchange-traded funds (ETFs). Since Vertiv's physical infrastructure business model is highly correlated with hyperscaler capital expenditures, any external de-risking or margin calls in the semiconductor market directly precipitates heavy institutional profit-taking on VRT.

- Extreme Valuation Multiples and Minimal Margin of Safety: Trading at a trailing P/E of approximately 70x and a forward P/E of over 45x, Vertiv’s valuation sits significantly above historical averages for industrial infrastructure companies. Financial analysis platforms indicate the stock is severely overvalued relative to its estimated intrinsic value of $152.90, exposing investors to severe downside volatility if current multi-billion dollar AI backlogs fail to convert into immediate, high-margin revenue.

- Regional Growth Weakness in EMEA: Despite robust global order momentum, Vertiv’s organic and regional performance remains uneven. In particular, EMEA regional operations are under pressure, with the segment suffering a sharp 20.3% year-over-year revenue drop and a 29.4% decline in organic sales during the first quarter, representing a localized operational bottleneck that could drag down consolidated full-year performance.

- Substantial C-Suite and Insider Divestments: Internal confidence faces scrutiny following a wave of executive profit-taking during the stock's run-up. Multiple C-suite executives and directors have completed substantial stock sales near the company's peak trading ranges, signaling that insiders may view the near-term equity valuation as fully priced.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.