Intel Corp Stock (INTC) Moved Down by 3.24% on Jun 26: A Full Analysis

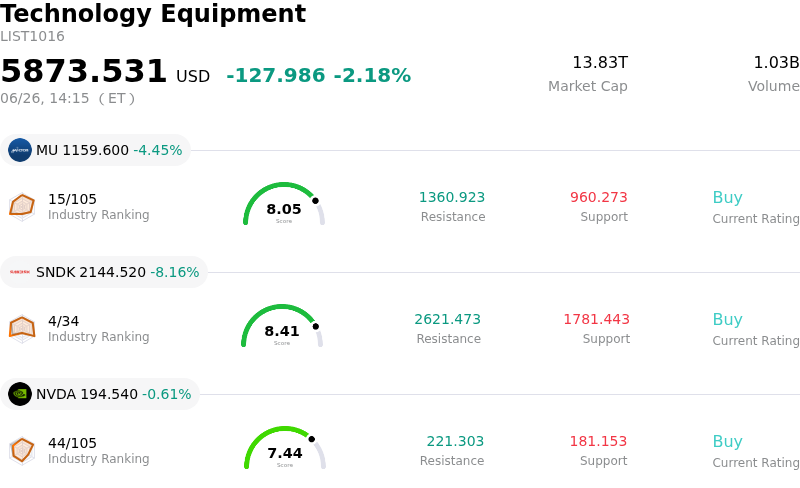

Intel Corp (INTC) moved down by 3.24%. The Technology Equipment sector is down by 2.18%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 4.45%; SanDisk Corporation (SNDK) down 8.16%; NVIDIA Corp (NVDA) down 0.61%.

What is driving Intel Corp (INTC)’s stock price down today?

Goldman Sachs initiated coverage of Intel with a Neutral rating and a 12-month price target of $150. While the firm acknowledged Intel’s long-term opportunities in AI-driven server CPU demand, domestic foundry leadership, and advanced packaging growth, it cautioned that the stock's massive year-to-date rally has already priced in a significant portion of this optimism. By suggesting that peers like Nvidia, Broadcom, and AMD present superior near-term revenue visibility, the brokerage's balanced risk-reward assessment prompted a cooling effect among investors.

Further compounding the pressure is growing scrutiny over Intel's stretched valuation. Following its meteoric rise over the past year, the company’s forward price-to-earnings multiple has ballooned significantly above the semiconductor industry average. This high valuation has raised concerns about the margin of safety, especially as the company continues to navigate near-term financial strains, substantial capital expenditure depreciation pressures, and ongoing foundry division losses. Profit-taking became a natural course for market participants looking to secure gains near multi-month highs.

The downward pressure was also amplified by a broader, risk-off tone across the macroeconomic landscape. Broad weakness in equity futures, particularly in technology-heavy indices, dragged down high-beta semiconductor equities. As market participants reduced exposure to large-cap technology names amid rising interest rate concerns, Intel experienced heightened intraday volatility.

Lastly, execution risks surrounding the company's ambitious turnaround remain a focal point. Although there is high optimism surrounding future foundry agreements—such as preliminary advanced packaging deals and future chip-making contracts—substantial revenue from these projects is not expected to materialize for another two to three years. Until these long-term commitments translate into realized external foundry revenues, investors remain highly sensitive to near-term operational and yield milestones, contributing to the stock's pullback.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of 2.017, indicating a buy signal. The RSI at 60.523 suggests neutral condition and the Williams %R at 19.898 suggests overbought condition. Please monitor closely.

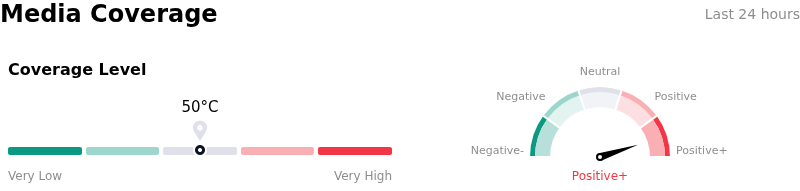

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 50, indicating a moderate level of media attention. The overall market sentiment index is currently in extremely bullish zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $94.77, a high of $160.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Overextended Valuation and Weak Relative Visibility: Following Goldman Sachs' coverage initiation on June 25, 2026, with a "Neutral" rating, institutional analysts flagged that Intel's massive rally has stretched its forward P/E to over 113x–133x. This leaves no margin of safety, particularly as peers like NVIDIA, Broadcom, and AMD present significantly stronger revenue visibility at comparable valuations.

- Speculative Run-Up Fueled by Unconfirmed Apple Partnership: Much of the stock's recent surge toward its 52-week high of $141.45 was driven by unconfirmed social media and political rumors of a domestic chip-manufacturing contract with Apple. Because neither company has officially verified the partnership, the stock remains highly vulnerable to a sharp pullback if actual order volumes fail to materialize.

- Margin Dilution and Sub-Profitable Yields on Next-Gen Nodes: Although Intel's advanced 18A-P process node entered the risk production phase on June 16, 2026, research indicates that current yields remain below the 50% profitable commercial threshold. Reaching commercial-scale profitability is delayed until late 2026 or 2027, posing near-term margin dilution and execution risks.

- Severe Capital Strain from Unprofitable Foundry Operations: Intel's foundry business remains deeply unprofitable, posting a $2.4 billion operating loss alongside a negative free cash flow of $3.87 billion in Q1 2026. This continuous cash burn restricts the company's financial flexibility to sustain its multi-billion-dollar domestic fab expansion projects.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (1)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.