KLA Corp Stock (KLAC) Closed Up by 8.71% on Jun 18: A Full Analysis

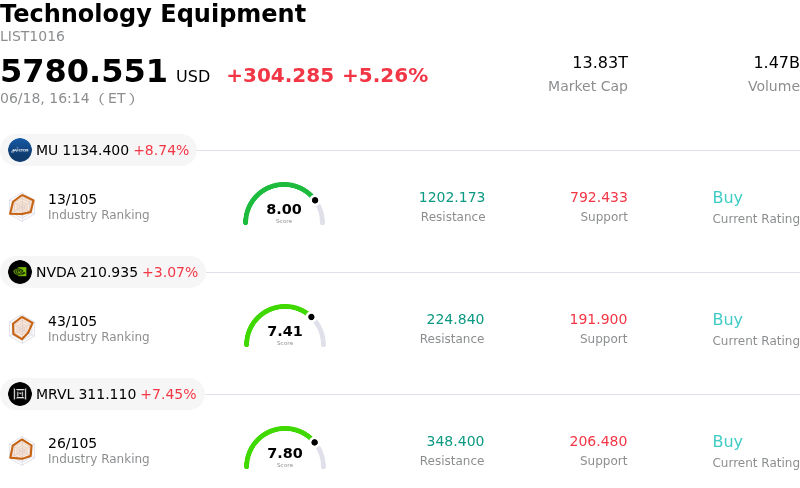

KLA Corp (KLAC) closed up by 8.71%. The Technology Equipment sector is up by 5.26%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 8.74%; NVIDIA Corp (NVDA) up 3.09%; Marvell Technology Inc (MRVL) up 7.44%.

What is driving KLA Corp (KLAC)’s stock price up today?

KLA Corporation's stock experienced a sharp upward surge, reversing recent downward momentum and demonstrating strong intraday volatility. This significant rally is primarily attributed to a combination of highly favorable analyst updates, a robust technical rebound from oversold conditions, and sustained optimism surrounding artificial intelligence-driven demand for semiconductor equipment.

A key catalyst for the gains was a major post-split price target hike from Citigroup. The bank raised its valuation outlook significantly, pointing to upward revisions in global wafer fabrication equipment spending. This adjustment is underpinned by projections of massive capital expenditure increases from hyperscalers through 2028, largely driven by the accelerating deployment of agentic artificial intelligence. This technological transition shifts memory and logic requirements, placing KLA’s specialized inspection and metrology tools in a highly favorable position. Additionally, other prominent Wall Street firms, including Cantor Fitzgerald and Barclays, recently bolstered their price targets, citing early-stage, multi-year supply cycles and strong booking visibility extending several years out.

From a technical standpoint, the stock was primed for a rebound. KLA recently executed a ten-for-one forward stock split, which initially spurred brief profit-taking and a technical pullback. The subsequent slide pushed key momentum indicators, such as the Relative Strength Index, deep into oversold territory. This technical oversold condition, coupled with the lower nominal share price post-split, triggered a wave of opportunistic buying as institutional and retail investors capitalized on the cheaper entry point, driving massive trading volume.

Broad sector momentum also supported the gains. In the semiconductor equipment space, process control intensity is increasing as advanced chips grow more complex and defects become costlier to manage. KLA remains a dominant player in this niche, benefiting from secular tailwinds in advanced packaging and artificial intelligence accelerators. While the company continues to navigate headwinds like stringent export controls on shipments to China and recent free cash flow contraction, the overwhelming long-term demand for artificial intelligence infrastructure has currently overshadowed these risks. The combination of structural industry growth, highly bullish analyst sentiment, and oversold technical signals successfully drove KLA's powerful intraday recovery.

Technical Analysis of KLA Corp (KLAC)

Technically, KLA Corp (KLAC) shows a MACD (12,26,9) value of -438.208, indicating a sell signal. The RSI at 18.727 suggests oversold condition and the Williams %R at 99.131 suggests oversold condition. Please monitor closely.

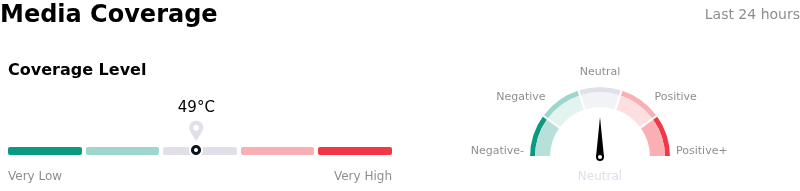

Media Coverage of KLA Corp (KLAC)

In terms of media coverage, KLA Corp (KLAC) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of KLA Corp (KLAC)

KLA Corp (KLAC) is in the Technology Equipment industry. Its latest annual revenue is $12.16B, ranking 15 in the industry. The net profit is $4.06B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $195.45, a high of $290.00, and a low of $138.80.

More details about KLA Corp (KLAC)

Company Specific Risks:

- **Severe Free Cash Flow Contraction:** KLA’s Q3 FY2026 operating cash flow plummeted 34.02% year-over-year, leading to a 37% year-over-year contraction in free cash flow. This sharp working capital deterioration represents a fundamental divergence from headline GAAP earnings and threatens short-term financial flexibility.

- **Margin Compression and Input Cost Pressures:** Management has projected an approximate 100-basis-point negative impact on near-term gross margins. This compression is driven by soaring memory component costs that the company is currently unable to pass down to its customer base.

- **China Export Restrictions:** Stringent and tightening government export controls targeting advanced semiconductor technologies continue to act as a direct drag on top-line growth, with management projecting a negative revenue impact of $300 million to $350 million in forfeited sales for the current fiscal year.

- **Elevated Valuation and Insider Divestments:** Following its 10-for-1 forward stock split, KLAC’s trailing P/E multiple expanded to over 67x, significantly above its historical five-year median of 26x. This premium is exacerbated by recent SEC filings showing $19.7 million in quarterly insider selling—including a $10 million stock liquidation by CEO Richard Wallace—raising institutional concerns about overvaluation.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.