Palantir Technologies Inc Stock (PLTR) Moved Up by 3.08% on May 7: A Full Analysis

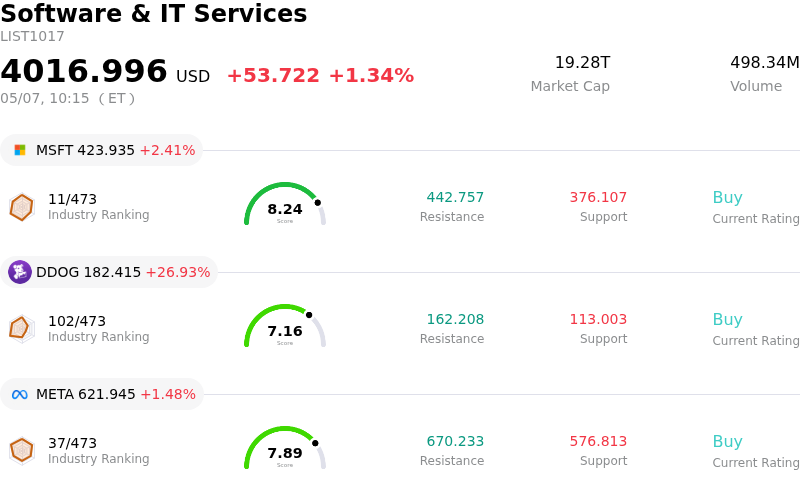

Palantir Technologies Inc (PLTR) moved up by 3.08%. The Software & IT Services sector is up by 1.34%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 2.41%; Datadog Inc (DDOG) up 26.93%; Meta Platforms Inc (META) up 1.48%.

What is driving Palantir Technologies Inc (PLTR)’s stock price up today?

Palantir Technologies (PLTR) experienced an upward movement today, primarily driven by the positive reception of its robust first-quarter fiscal year 2026 earnings report. The company announced impressive financial results on May 4, 2026, significantly surpassing analyst expectations for both revenue and earnings per share.

The reported revenue reached $1.6 billion, representing an 85% year-over-year increase, outperforming the consensus estimate. Adjusted earnings per share also exceeded projections, demonstrating strong operational performance. A key highlight from the earnings call was the substantial growth in Palantir's U.S. business, with overall U.S. revenue increasing by 104% year-over-year. The U.S. commercial segment saw a particularly strong surge, growing by 133% year-over-year, while the U.S. government segment also posted significant growth.

Furthermore, the company provided an optimistic outlook by raising its full-year 2026 revenue guidance to a range implying 71% growth, along with increased guidance for U.S. commercial revenue, adjusted operating income, and adjusted free cash flow. Management underscored the success of its Artificial Intelligence Platform (AIP) in driving U.S. adoption for critical operational use cases across both commercial and government sectors. Palantir also highlighted an exceptional "Rule of 40" score of 145%, indicative of its accelerated growth and high profitability.

Following the strong earnings announcement, several analysts reacted positively, contributing to today's upward price action. Argus upgraded Palantir to a "Buy" rating from "Hold" today, May 7, 2026, citing the better-than-expected results and revised outlook, and raised its price target. Similarly, Rosenblatt increased its price target to $225 from $200 on May 5, maintaining a "Buy" rating, while Wedbush also held an "Outperform" rating with a $230 price target. These positive adjustments from research firms appear to have counteracted earlier profit-taking, which saw the stock decline on May 5, 2026, despite the strong fundamentals. The continued confidence from analysts, coupled with Palantir's strategic partnerships, such as with Nvidia for a turnkey AI operating system, reinforces investor sentiment.

Technical Analysis of Palantir Technologies Inc (PLTR)

Technically, Palantir Technologies Inc (PLTR) shows a MACD (12,26,9) value of [-1.30], indicating a sell signal. The RSI at 41.22 suggests neutral condition and the Williams %R at -87.74 suggests oversold condition. Please monitor closely.

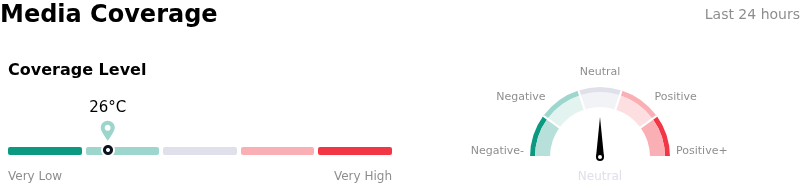

Media Coverage of Palantir Technologies Inc (PLTR)

In terms of media coverage, Palantir Technologies Inc (PLTR) shows a coverage score of 26, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Palantir Technologies Inc (PLTR)

Palantir Technologies Inc (PLTR) is in the Software & IT Services industry. Its latest annual revenue is $4.48B, ranking 73 in the industry. The net profit is $1.63B, ranking 32 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $182.43, a high of $255.00, and a low of $70.00.

More details about Palantir Technologies Inc (PLTR)

Company Specific Risks:

- Palantir's extremely high valuation multiples (e.g., 150-217 P/E, 42x implied 2026 sales) leave minimal room for error and render the stock highly sensitive to any perceived moderation in growth or shifts in AI market sentiment, despite strong Q1 2026 earnings.

- Multiple analysts have downgraded Palantir or lowered price targets post-earnings, with concerns ranging from the company's ability to sustain growth off a larger base (Jefferies, price target $70) to erosion of its competitive moat by rivals like OpenAI and Anthropic (HSBC, DA Davidson).

- Significant insider selling activity, totaling $435.1 million in the last three months and showing a net selling trend across 72 recent transactions, may signal diminished confidence from company insiders.

- While overall revenue grew, Palantir's U.S. commercial sales (Q1 2026: $595M) fell short of analyst expectations ($605M consensus), indicating uneven commercial momentum and continued heavy reliance on government contracts, which constituted 78% of its total U.S. revenue.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.