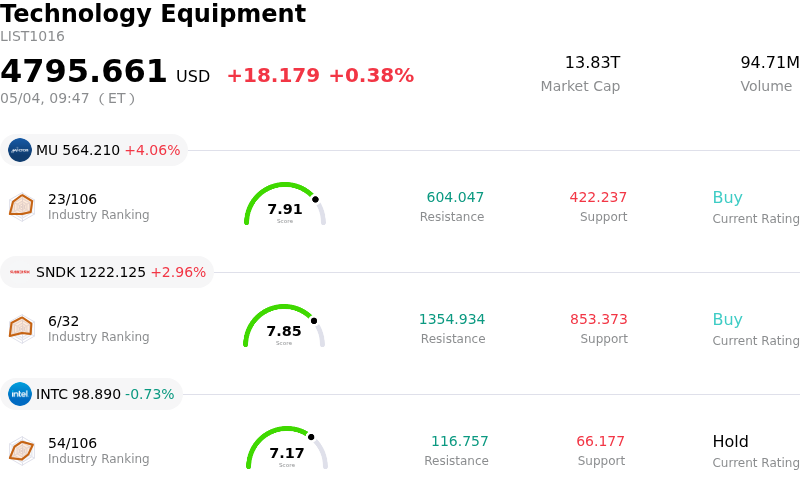

Micron Technology Inc Stock (MU) Opened Up by 4.06% on May 4: Facts Behind the Movement

Micron Technology Inc (MU) opened up by 4.06%. The Technology Equipment sector is up by 0.38%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 4.06%; SanDisk Corporation (SNDK) up 2.96%; Intel Corp (INTC) down 0.73%.

What is driving Micron Technology Inc (MU)’s stock price up today?

Micron Technology's stock experienced an upward movement due to a confluence of robust financial performance, strong demand in key markets, and highly positive analyst sentiment. The company issued overwhelmingly strong earnings guidance for the third quarter of 2026 in April, significantly exceeding consensus estimates for both EPS and revenue. This guidance followed impressive financial results for fiscal Q2 2026, which also substantially surpassed expectations, marking a fourth consecutive quarter of record revenue driven by strong demand in the DRAM and NAND segments.

A primary catalyst for the stock's performance is the surging demand for High Bandwidth Memory (HBM), a critical component in artificial intelligence (AI) applications. Micron is a leading global supplier of HBM and has indicated that its HBM products are sold out for the next several quarters. The company is progressing with its HBM4 development, with mass production expected to begin in 2026, and is aggressively expanding its manufacturing capacity for these advanced memory chips. The overall HBM market is projected to see significant growth, expanding from approximately $35 billion in 2025 to around $100 billion by 2028, a forecast that has been accelerated. The industry is currently experiencing a supply crunch for HBM, leading to increased pricing.

Analyst sentiment remains exceptionally bullish, contributing to the positive share price movement. Numerous analysts have recently raised their price targets for Micron. For instance, UBS reiterated a Buy rating and increased its price target, citing an ongoing memory "super-cycle" and improved pricing. Furthermore, a D.A. Davidson analyst initiated coverage with a $1,000 price target in May 2026, the highest on Wall Street, attributing this optimism to AI-driven demand creating a longer-than-usual memory cycle. The company holds a strong "Buy" consensus rating from a large number of analysts. This strong analyst confidence, combined with increasing institutional investment, further supports the upward trajectory of the stock. Market research also points to significant sequential increases in contract prices for both DRAM and NAND flash memory, serving as a substantial tailwind for Micron.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [25.12], indicating a buy signal. The RSI at 71.84 suggests buy condition and the Williams %R at -3.06 suggests oversold condition. Please monitor closely.

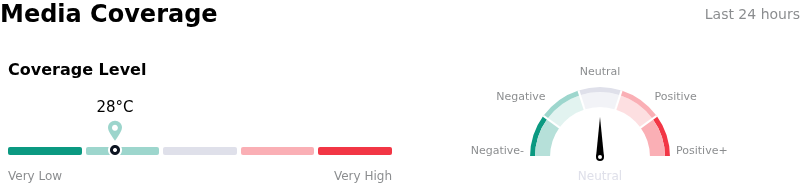

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 28, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $535.54, a high of $1000.00, and a low of $125.00.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Micron's aggressive capital spending plans for new fabrication plants, exceeding $25 billion for FY2026 and increasing for FY2027, raise investor concerns about potential future overcapacity in the memory market, particularly if AI demand growth moderates or synchronized competitor plant openings lead to supply-demand imbalances, which could impact gross margins.

- Intensifying competition from rivals like Samsung and SK Hynix, who are aggressively scaling and innovating in High Bandwidth Memory (HBM), poses a risk of price wars and erosion of Micron's HBM margins, with some analysts highlighting concerns about potential HBM pricing declines in 2026 not yet fully priced into the market.

- The inherent cyclicality of the memory chip market, where pricing is not based on performance advantages, combined with recent analyst downgrades and reiterated "Sell" ratings, indicates fundamental valuation risks due to skepticism about the HBM-driven narrative, dropping DRAM spot prices, and the stock potentially nearing a cyclical peak.

- The advanced and complex manufacturing processes required for High Bandwidth Memory (HBM), including 3D stacking with no redundancy, make large-scale production exponentially challenging, introducing significant execution risks and supply chain complexities that could limit Micron's ability to consistently meet booming demand.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.