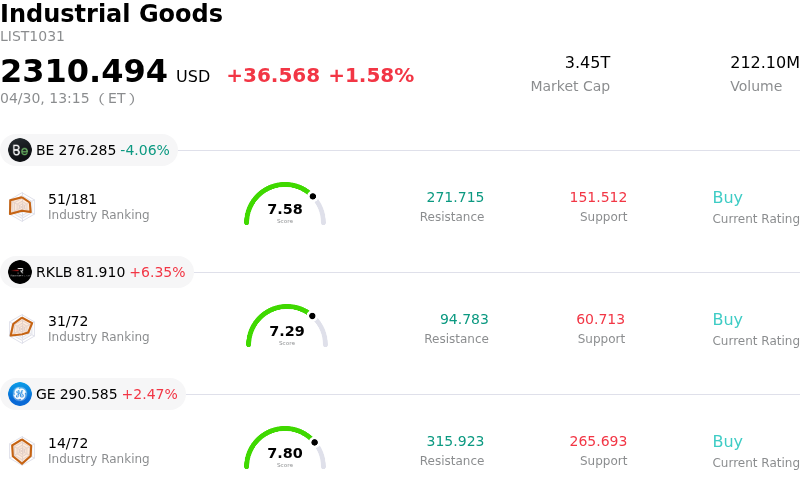

Vertiv Holdings Co Stock (VRT) Moved Up by 5.97% on Apr 30: Drivers Behind the Movement

Vertiv Holdings Co (VRT) moved up by 5.97%. The Industrial Goods sector is up by 1.58%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Bloom Energy Corp (BE) down 4.06%; Rocket Lab USA Inc (RKLB) up 6.35%; General Electric Co (GE) up 2.47%.

What is driving Vertiv Holdings Co (VRT)’s stock price up today?

Several key factors appear to be driving the positive movement in VRT's stock price. The company recently reported robust first-quarter 2026 financial results, with adjusted earnings per share significantly surpassing consensus estimates. This strong earnings beat, coupled with a slight revenue beat, signaled healthy operational performance and market demand for Vertiv's solutions.

Adding to the positive sentiment, management raised its full-year 2026 guidance across net sales, adjusted operating profit, and adjusted earnings per share. This upward revision suggests a confident outlook from the company's leadership regarding continued business momentum and an ability to capitalize on prevailing market trends. The improved guidance is a strong indicator of sustained growth expectations among investors.

A significant tailwind for Vertiv is the escalating demand from the data center industry, particularly driven by the rapid expansion of artificial intelligence infrastructure. Vertiv plays a critical role in providing essential power and cooling solutions for these high-density computing environments. The company's strategic acquisition of Strategic Thermal Labs LLC in late April, a specialist in advanced liquid-cooling technologies, further strengthens its position in serving the increasingly complex thermal management needs of AI workloads. This acquisition is seen as enhancing Vertiv's capabilities and competitive edge in a crucial growth area.

Furthermore, the strong financial performance and strategic moves have led to positive adjustments from the analyst community. Multiple equity research analysts have either reiterated favorable ratings or significantly increased their price targets for VRT shares in the days leading up to and on April 30, 2026. This positive analyst sentiment, including a recent Zacks Rank upgrade, often translates into increased investor confidence and buying interest.

While some insider selling and minor institutional stake trimming have been noted, these appear to be overshadowed by broader institutional buying activity, with several firms increasing their positions and a new significant stake being opened by a public employees retirement fund. The overall picture indicates that the market is reacting favorably to Vertiv's strong execution, strategic positioning within the booming AI infrastructure market, and optimistic future projections.

Technical Analysis of Vertiv Holdings Co (VRT)

Technically, Vertiv Holdings Co (VRT) shows a MACD (12,26,9) value of [14.91], indicating a neutral signal. The RSI at 57.40 suggests neutral condition and the Williams %R at -58.82 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Vertiv Holdings Co (VRT)

Vertiv Holdings Co (VRT) is in the Industrial Goods industry. Its latest annual revenue is $10.23B, ranking 17 in the industry. The net profit is $1.33B, ranking 13 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $315.51, a high of $380.00, and a low of $112.00.

More details about Vertiv Holdings Co (VRT)

Company Specific Risks:

- Vertiv Holdings Co experienced a 20% decline in revenue from overseas markets, particularly Europe, the Middle East, and Africa (EMEA), with organic sales down 29.4% in Q1 2026, contributing to post-earnings stock weakness and investor concerns.

- The company's Q2 EPS guidance, set between $1.370 and $1.430, marginally fell below some street expectations of approximately $1.44, leading to profit-taking and increased intraday volatility.

- Management's decision not to disclose the Q1 backlog figure has created uncertainty among investors regarding future demand visibility.

- The stock's high valuation, noted by some analysts, makes it particularly susceptible to market concerns and potential competitive risks, such as major customers developing in-house solutions, contributing to volatility.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.