Arm Holdings PLC Stock (ARM) Moved Up by 3.03% on Apr 30: Key Drivers Unveiled

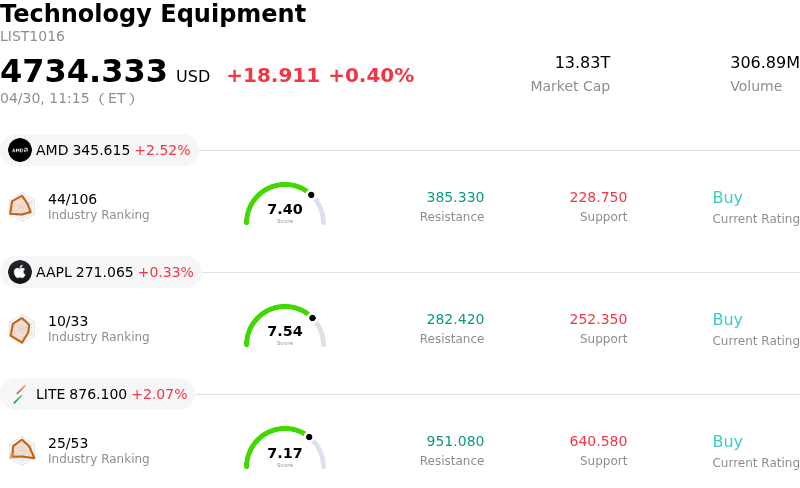

Arm Holdings PLC (ARM) moved up by 3.03%. The Technology Equipment sector is up by 0.40%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Advanced Micro Devices Inc (AMD) up 2.52%; Apple Inc (AAPL) up 0.33%; Lumentum Holdings Inc (LITE) up 2.07%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

ARM Holdings experienced upward movement today, suggesting investor confidence in the company's long-term prospects, particularly within the burgeoning artificial intelligence sector. This positive sentiment appears to have outweighed recent concerns and broader market jitters. The strong underlying demand for AI-driven chip technology continues to be a primary catalyst, with the semiconductor industry seeing accelerated capital spending on advanced manufacturing tools to meet this need.

A significant factor contributing to today's positive performance includes recent optimistic revisions from equity analysts. Several firms, such as Wells Fargo and Mizuho, upgraded their price targets and reiterated favorable ratings for ARM in late April, citing the company's strategic positioning to benefit from emerging AI opportunities and growth in data centers. Needham also recently upgraded ARM's rating to "Buy." These positive adjustments in analyst forecasts likely provided a boost to market sentiment, encouraging buying activity.

Despite a reported decline in the stock's value on April 28, which was linked to concerns about hyperscaler capital expenditure following a report regarding OpenAI's growth targets and Taiwan Semiconductor Manufacturing Company's complete divestment of its ARM shares, the overall bullish thesis for ARM's role in AI appears resilient. ARM's plans to design its own AI chips, in addition to its core licensing business, are seen by some as sharpening its upside potential in the AI data center market, even while acknowledging associated execution risks. The broader semiconductor market continues to exhibit strong performance, with weekly sales increasing year-over-year. This favorable industry backdrop supports ARM's growth narrative as a critical enabler of AI innovation.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [15.45], indicating a buy signal. The RSI at 63.86 suggests neutral condition and the Williams %R at -39.91 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.01B, ranking 26 in the industry. The net profit is $792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $166.63, a high of $240.00, and a low of $81.78.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Rumors of a potential collaboration between Qualcomm and OpenAI to develop a custom chip not based on ARM's architecture introduce a significant competitive threat and risk of losing key design wins.

- ARM's strategic pivot into designing and selling its own production silicon for AI data centers risks margin compression, as hardware sales typically carry substantially lower gross margins compared to its historically high-margin licensing model.

- The company's elevated valuation, with price-to-earnings ratios exceeding 130 and price-to-sales ratios significantly above industry averages, leaves the stock highly vulnerable to profit-taking and sharp pullbacks amid any broader cooling of sentiment for AI-levered equities.

- Uncertainty regarding hyperscaler AI capital expenditure is heightened by reports of OpenAI missing internal revenue targets and tempering infrastructure ambitions, which directly impacts ARM's revenue growth outlook given its exposure to custom silicon in the data center market.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.