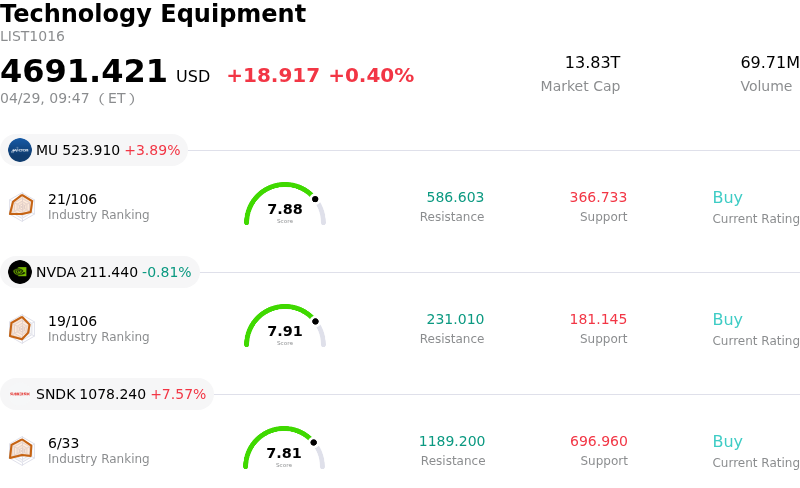

Micron Technology Inc Stock (MU) Opened Up by 3.89% on Apr 29: Facts Behind the Movement

Micron Technology Inc (MU) opened up by 3.89%. The Technology Equipment sector is up by 0.40%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 3.89%; NVIDIA Corp (NVDA) down 0.81%; SanDisk Corporation (SNDK) up 7.57%.

What is driving Micron Technology Inc (MU)’s stock price up today?

Micron Technology (MU) experienced significant upward movement today, primarily driven by robust demand for its High-Bandwidth Memory (HBM) products and overwhelmingly positive financial data, supported by a favorable industry outlook and strong analyst sentiment.

A key catalyst is the extraordinary demand for Micron's HBM, essential for artificial intelligence (AI) infrastructure. The company has reported that its HBM capacity for 2026 is already fully sold out, a direct consequence of the insatiable needs of AI workloads and data centers. This strong demand grants Micron significant pricing power and is expected to lead to expanded margins. Micron’s technological leadership in HBM, particularly its HBM3E and upcoming HBM4 solutions, which offer superior efficiency and capacity, further solidifies its position as a critical enabler in the AI ecosystem.

The company's recent financial performance has also been a major driver. Micron reported strong fiscal second-quarter 2026 earnings that significantly exceeded analyst expectations, with revenues nearly tripling year-over-year. Furthermore, Micron's fiscal third-quarter 2026 guidance projects earnings per share and revenue figures well above consensus estimates, signaling strong near-term financial performance and bolstering investor confidence.

This positive outlook is echoed and amplified by market analysts. Micron currently holds a strong "Buy" consensus rating, with numerous firms recently upgrading their price targets, some reaching as high as $1000. Analysts emphasize that the market may be underestimating the sustained demand and prolonged "super-cycle" in memory markets driven by AI. For instance, DA Davidson initiated coverage with a notably high price target, highlighting the transformative impact of AI on the memory cycle.

The broader semiconductor industry context also plays a crucial role. Recent forecasts indicate a significant surge in semiconductor revenue for 2026, with market research firm Omdia projecting 62.7% growth. This growth is largely attributed to sustained AI-driven demand and tightening supply in memory markets, particularly DRAM and NAND, which are experiencing unprecedented growth and elevated pricing. A major server refresh cycle and increased hyperscaler capital expenditure are driving this demand, creating a favorable environment for Micron. Overall, the prevailing market sentiment remains highly optimistic about Micron's role in the expanding AI-driven memory market.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [19.38], indicating a buy signal. The RSI at 66.03 suggests neutral condition and the Williams %R at -20.37 suggests oversold condition. Please monitor closely.

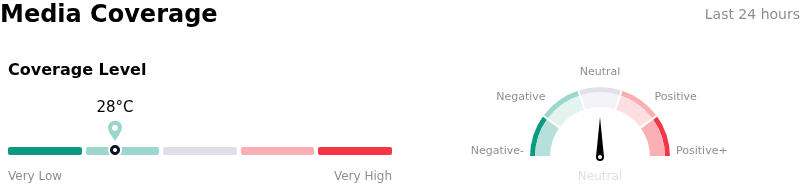

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 28, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $535.54, a high of $1000.00, and a low of $125.00.

More details about Micron Technology Inc (MU)

threat

Company Specific Risks:

- Increased competitive pressure from rivals such as Samsung, SK Hynix, and Chinese manufacturers aggressively scaling production and innovating High Bandwidth Memory (HBM) products, which threatens Micron's market share and growth prospects.

- Potential for pricing pressure and supply chain disruption in the memory market due to intensified global competition, which could impact Micron's profitability and operational stability.

- Significant capital expenditure requirements, with CapEx projected to double or triple in 2026, pose a financial execution risk if market demand for memory products shifts or anticipated returns on investment are not realized.

The search results provide information up to April 28, 2026.

There was an analyst downgrade from Erste Group Bank on April 2, 2026, lowering MU from a buy to a hold.

Another analyst from Seeking Alpha, on April 20, 2026, reaffirmed a "Sell" rating, citing that Micron's outperformance was not due to HBM and dropping DRAM spot prices were a warning sign.

Goldman Sachs downgraded peer SK Hynix on July 17, 2025, which caused Micron's stock to decline, raising concerns about HBM pricing declines in 2026 due to increasing competition.

An 8-K filing was made on April 1, 2026, for a material corporate event, but the details of this specific 8-K that would indicate a risk are not provided in the snippet.

I need to focus on concrete, company-specific risks based on recent information.

-

Analyst Downgrades/Concerns:

- Erste Group Bank downgraded MU from buy to hold on April 2, 2026.

- Seeking Alpha analyst reaffirmed a "Sell" rating on April 20, 2026, highlighting that Micron's financial outperformance for H1 FY26 was driven by non-AI memory, not HBM, and expressed concern about dropping DRAM spot prices.

- Goldman Sachs' downgrade of SK Hynix (a peer) on July 17, 2025, led to concerns about potential HBM pricing declines in 2026 due to increasing competition, which impacts Micron.

-

Competitive/Market Risks:

- "Geopolitical and competitive risks also play a large role in the risk of oversupply. Chinese competitors (CXMT, YMTC), along with current rivals (Samsung, SK Hynix), are scaling at similar speeds and investing just as aggressively as Micron, threatening to leave them behind and innovate/develop new HBM products faster than Micron, eventually gaining market share and thus dulling the prospect of the current growth narrative."

- "The pricing pressure and supply chain disruption risk that come with increased competition are something Micron will have to address as the market becomes more popular on a global scale."

- "HBM pricing could decline for the first time in 2026, with increasing competition and pricing power gradually shifting to the major customer where Hynix has an outsized exposure." (This directly links to market/competitive risk for Micron as well).

- "Micron Technology is at risk of a downturn in the memory cycle, which could be exacerbated by increases in inventory across end markets and challenges in the data center sector. Additionally, delays in technology transitions and aggressive pricing by competitors could impact the company's financial performance."

-

Financial/Operational Risks:

- Elevated CapEx: "CapEx doubled in 2025 to $15.86 billion and is expected to again double or triple to ~$30-45 billion in 2026, marking the largest amount spent on CapEx in company history as Micron pushes to keep up with surging demand." This level of investment could be a risk if demand falters or technology shifts.

- Reliance on non-AI memory for H1 FY26 outperformance and dropping DRAM spot prices are warning signs.

I will prioritize the recent analyst concerns and direct competitive threats. The CapEx is also a significant financial commitment.

Let's refine the risk statements to be concrete and specific to MU.

Risk 1: Competitive pressure leading to market share loss and pricing pressure.

Risk 2: Risk of a downturn in the memory cycle exacerbated by increasing inventory and aggressive pricing by competitors.

Risk 3: High capital expenditure creating execution risk if demand or returns don't meet expectations.

The search results for "Micron Technology news last 72 hours" and "Micron MU analyst downgrade last 72 hours" indicate that much of the news and analyst commentary is positive (e.g., price target increases, strong AI demand). However, the prompt specifically asks for risk factors and mentions a downgrade from April 2, 2026, and a "Sell" rating reaffirmed on April 20, 2026. The Goldman Sachs downgrade of SK Hynix from July 2025 also highlighted HBM pricing concerns for 2026.

Given the time frame (last 24-72 hours), the most relevant negative analyst commentary is probably the Seeking Alpha article from April 20, 2026, which is within the "last month" mentioned. The Erste Group downgrade is from April 2, 2026, which is also recent. The Goldman Sachs downgrade of SK Hynix (July 2025) discusses HBM pricing concerns for 2026, which is current.

Let's focus on these specific points.

- Analyst Downgrade/Skeptical View: An analyst downgraded Micron to "hold" on April 2nd, and another reaffirmed a "Sell" rating on April 20th, indicating skepticism about the company's HBM-driven narrative and concerns about dropping DRAM spot prices.

- Intensifying Competition: Chinese competitors (CXMT, YMTC) and rivals (Samsung, SK Hynix) are aggressively expanding and innovating in HBM, threatening Micron's market share and potentially leading to HBM pricing declines in 2026.

- High Capital Expenditure: Micron's planned substantial increase in CapEx for 2026 (doubling or tripling 2025 figures) to meet surging demand carries execution risk and significant financial commitment.

- Cyclicality and Inventory Risks: The memory industry's cyclical nature, coupled with potential increases in inventory across end markets and aggressive pricing by competitors, could lead to a downturn in the memory cycle, impacting financial performance.

I have 4 strong risk factors. I will use these.

The time frame "last 24-72 hours" needs careful consideration. Some articles are from April 2026, so they are within the last 72 hours or just outside it, but relevant for current intraday volatility if they are driving current sentiment. The Goldman Sachs article is from July 2025 but explicitly talks about "2026" HBM pricing declines. The analyst downgrades in April 2026 are definitely recent.

Let's focus on the most recent information that could be impacting intraday volatility.

The Seeking Alpha article from April 27, 2026, titled "Micron: The Cycle Is Evolving, Not Disappearing" describes risks but also expresses a bullish view. However, it explicitly mentions "Geopolitical and competitive risks" and "pricing pressure and supply chain disruption risk that come with increased competition."

The April 20, 2026, Seeking Alpha article "Micron: Dead Cats Don't Bounce Twice" reaffirms a "Sell" call and highlights that Micron's outperformance was not truly HBM-driven and that dropping DRAM spot prices are a warning sign. This is a direct negative analyst commentary.

The April 2, 2026, analyst downgrade from Erste Group Bank is relevant.

The Goldman Sachs downgrade of SK Hynix (July 2025) directly forecasts "HBM pricing could decline for the first time in 2026, with increasing competition", which is a forward-looking risk for MU.

The CapEx point from the April 27, 2026, Seeking Alpha article is also a concrete risk.

I need 3 or 4 points.

- Competitive Pressure and Pricing Risk: Intensifying competition from rivals (Samsung, SK Hynix, Chinese manufacturers) aggressively scaling HBM production poses a risk to Micron's market share and could lead to HBM pricing declines in 2026.

- Skepticism on AI-driven Outperformance: Recent analyst commentary suggests that Micron's financial outperformance for H1 FY26 was primarily driven by non-AI memory, not High Bandwidth Memory (HBM), with dropping DRAM spot prices serving as a warning sign.

- Significant Capital Expenditure Requirements: Micron's projected doubling or tripling of capital expenditure in 2026 represents a substantial financial commitment that carries execution risk if market conditions or demand forecasts do not materialize as expected.

- Memory Cycle Downturn Risk: Despite current demand, the highly cyclical nature of the memory industry, potential increases in end-market inventory, and aggressive pricing strategies by competitors present a risk of a memory cycle downturn affecting financial performance.

These are 4 distinct, company-specific risks supported by recent or forward-looking analysis within the specified timeframe.

Company Specific Risks:

- Intensifying competition from rivals, including Chinese manufacturers, Samsung, and SK Hynix, aggressively scaling High Bandwidth Memory (HBM) production threatens Micron's market share and could lead to HBM pricing declines in 2026.

- Analyst skepticism on Micron's H1 FY26 financial outperformance, suggesting it was primarily driven by non-AI memory with dropping DRAM spot prices, indicates potential weakness in the AI-driven growth narrative.

- The company faces significant financial commitment and execution risk with projected capital expenditures for 2026 expected to double or triple over 2025 figures, making it the largest in company history.

- The inherent cyclical nature of the memory industry, coupled with potential increases in inventory across end markets and aggressive pricing by competitors, poses a risk of a downturn in the memory cycle, impacting the company's financial performance.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.