Alibaba Group Holding Ltd Stock (BABA) Moved Down by 3.22% on Apr 23: Drivers Behind the Movement

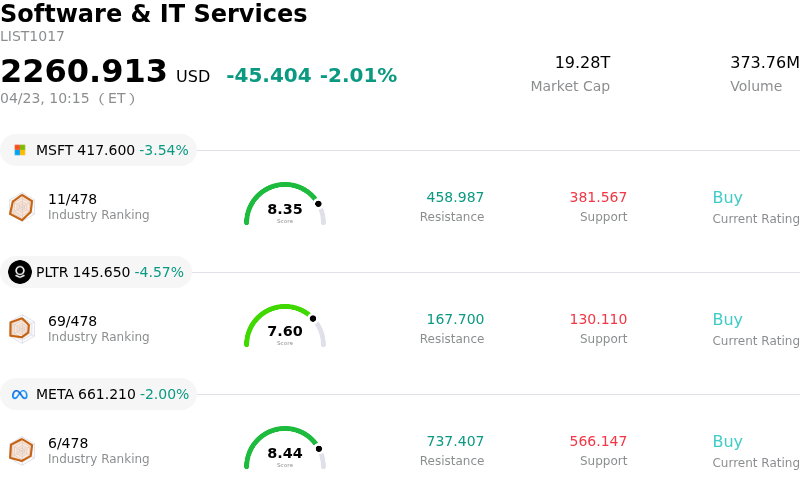

Alibaba Group Holding Ltd (BABA) moved down by 3.22%. The Software & IT Services sector is down by 2.01%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 3.54%; Palantir Technologies Inc (PLTR) down 4.57%; Meta Platforms Inc (META) down 2.00%.

What is driving Alibaba Group Holding Ltd (BABA)’s stock price down today?

Alibaba (BABA) stock is experiencing a downward movement with significant intraday volatility today, April 23, 2026, primarily driven by a confluence of company-specific financial challenges, ongoing regulatory scrutiny in China, and competitive pressures.

Recent reports indicate that Alibaba is facing considerable pressure on its profitability due to rising costs and aggressive investments in new growth areas. The company's fiscal third-quarter 2026 results showed a significant decline in net income and free cash flow, despite some revenue growth. This is attributed to substantial investments in AI infrastructure and quick-commerce initiatives. Management has also indicated that adjusted EBITA will continue to fluctuate due to this investment intensity, suggesting that profitability normalization is not expected in the immediate future. Analysts have also revised down their earnings per share (EPS) estimates for fiscal 2026, signaling deteriorating near-term business trends.

Furthermore, regulatory actions in China continue to impact investor sentiment. Chinese authorities recently imposed significant fines on major delivery platforms, including Alibaba, for issues related to merchant oversight and "ghost deliveries." This action, reported on April 17, reinforces a perception of heightened regulatory scrutiny on Chinese technology companies. While some market participants might view such fines as a closure of regulatory overhang, for Alibaba, it contributes to increased compliance costs and potential operational uncertainties.

The intensely competitive landscape within China's quick commerce and delivery sectors is also a significant factor. Aggressive investment and price wars among major players are impacting profitability, adding to the company's financial strain. This competitive pressure, combined with increased regulatory costs, is dampening investor enthusiasm.

Although there have been positive developments, such as Alibaba's rollout of an enterprise AI-native agent platform "Wukong" and the launch of a 10,000-card intelligent computing cluster with China Telecom, these long-term strategic investments are currently compressing near-term operating margins and free cash flow. Profitability for these new segments is not expected until fiscal 2028-2029, meaning they are not providing immediate relief to the financial pressures.

Geopolitical developments, specifically the US-China relationship and tensions in regions like the Strait of Hormuz, also create an overarching layer of uncertainty for Chinese stocks like BABA. While a recent ceasefire between the U.S. and Iran had previously boosted tech stocks due to easing geopolitical tensions, any renewed concerns or shifts in these dynamics can quickly impact investor risk appetite for Chinese assets.

Technical Analysis of Alibaba Group Holding Ltd (BABA)

Technically, Alibaba Group Holding Ltd (BABA) shows a MACD (12,26,9) value of [-1.30], indicating a neutral signal. The RSI at 55.44 suggests neutral condition and the Williams %R at -28.47 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Alibaba Group Holding Ltd (BABA)

Alibaba Group Holding Ltd (BABA) is in the Software & IT Services industry. Its latest annual revenue is $138.07B, ranking 5 in the industry. The net profit is $17.94B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $184.69, a high of $256.87, and a low of $112.00.

More details about Alibaba Group Holding Ltd (BABA)

Company Specific Risks:

- Alibaba faces significant pressure on profitability and operating margins due to surging sales and marketing costs (25.3% of revenues) and increased cost of revenues (59.5% of total revenues) in Q3 FY26, alongside a 71% decline in free cash flow, as reported by Zacks.

- Analyst sentiment has turned more cautious, with Freedom Capital downgrading BABA to a "Hold" rating, Erste Group downgrading to "Hold" due to declining operating margins and rising long-term liabilities, and TipRanks' AI Analyst issuing a Neutral rating citing weak cash flow and heavy AI/cloud spending.

- The company's substantial investments in AI, cloud, and quick commerce have led to a reported 67% decline in non-GAAP profit and a 204% fall in free cash flow over the past year, raising concerns about near-term earnings erosion and an uncertain payback period for these capital expenditures.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.