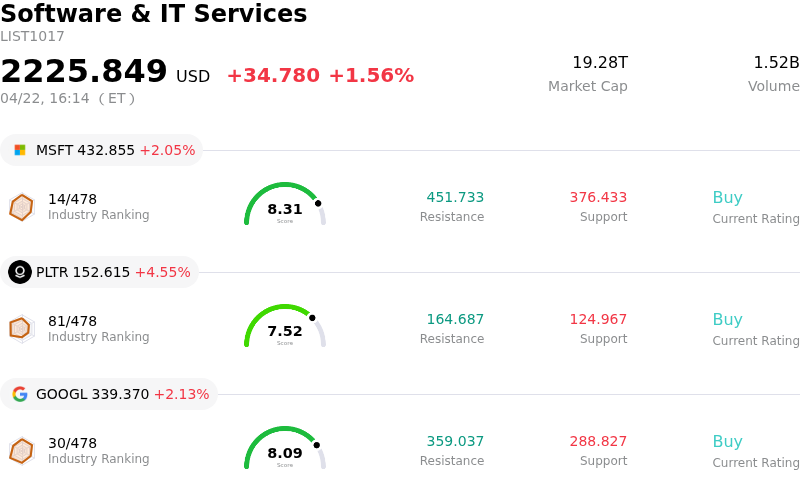

ServiceNow Inc Stock (NOW) Closed Up by 3.03% on Apr 22: Drivers Behind the Movement

ServiceNow Inc (NOW) closed up by 3.03%. The Software & IT Services sector is up by 1.56%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 2.05%; Palantir Technologies Inc (PLTR) up 4.55%; Alphabet Inc Class A (GOOGL) up 2.13%.

What is driving ServiceNow Inc (NOW)’s stock price up today?

ServiceNow experienced a positive stock movement today, primarily driven by strong financial results for its first quarter of 2026 and continued advancements in its artificial intelligence strategy. The company announced its Q1 2026 financial results after market close, reporting revenues that surpassed consensus estimates and beating the high end of its own guidance across key growth and profitability metrics. This robust performance, coupled with an increased full-year subscription revenues outlook, appears to have instilled investor confidence.

Ahead of the earnings release, several analysts maintained positive ratings on ServiceNow, with some expecting the company to exceed financial expectations. Benchmark, for instance, reiterated a "Buy" rating, anticipating strong performance in revenue, operating income, operating margin, and free cash flow for the first quarter. This pre-earnings optimism, combined with the confirmed beat, likely contributed to the upward trend.

Furthermore, strategic initiatives related to AI continue to bolster the company's outlook. ServiceNow recently completed its acquisition of Armis, a move that expands its security offerings and supports its overarching AI Control Tower strategy. The company also launched new AI-native solutions for the manufacturing sector and introduced a Dispute Management AI Agent in partnership with Xactly, designed to automate revenue workflows. These developments highlight ServiceNow's commitment to integrating AI across its product portfolio, with reports indicating that its Now Assist AI products are showing significant growth in net new annual contract value. The recognition as a Leader in the 2026 IDC MarketScape for worldwide AIOps further validates its strong position in the AI domain.

While the stock has experienced notable declines in previous periods, partly due to concerns regarding AI's potential impact on traditional software business models, the current positive developments and strong financial execution suggest that ServiceNow is effectively navigating these industry shifts. Institutional investors are also showing renewed interest, with some highlighting ServiceNow as a compelling opportunity amidst the AI disruption.

Technical Analysis of ServiceNow Inc (NOW)

Technically, ServiceNow Inc (NOW) shows a MACD (12,26,9) value of [-4.66], indicating a neutral signal. The RSI at 48.94 suggests neutral condition and the Williams %R at -23.36 suggests oversold condition. Please monitor closely.

Fundamental Analysis of ServiceNow Inc (NOW)

ServiceNow Inc (NOW) is in the Software & IT Services industry. Its latest annual revenue is $13.28B, ranking 30 in the industry. The net profit is $1.75B, ranking 31 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $167.42, a high of $260.00, and a low of $100.00.

More details about ServiceNow Inc (NOW)

Company Specific Risks:

- UBS recently downgraded ServiceNow to Neutral from Buy and significantly reduced its price target from $170 to $100, citing a material shift in enterprise spending priorities and growing interest in lighter workflow tools, contributing to a 7.6% intraday stock decline.

- Analyst commentary highlights the risk of disruption to ServiceNow's core software business model from autonomous AI agents and alternative solutions, which could reduce demand for traditional human-operated tools and lead to "seat compression."

- Concerns persist regarding ServiceNow's valuation, as some analysts believe the stock still trades at a rich premium compared to peers, even after a substantial year-to-date decline, with questions about slowing organic growth and expense discipline.

- The recently completed $7.75 billion Armis acquisition introduces potential integration risks and raises questions about expense management, particularly if organic growth continues to slow, requiring careful distinction between organic and inorganic revenue contributions.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.