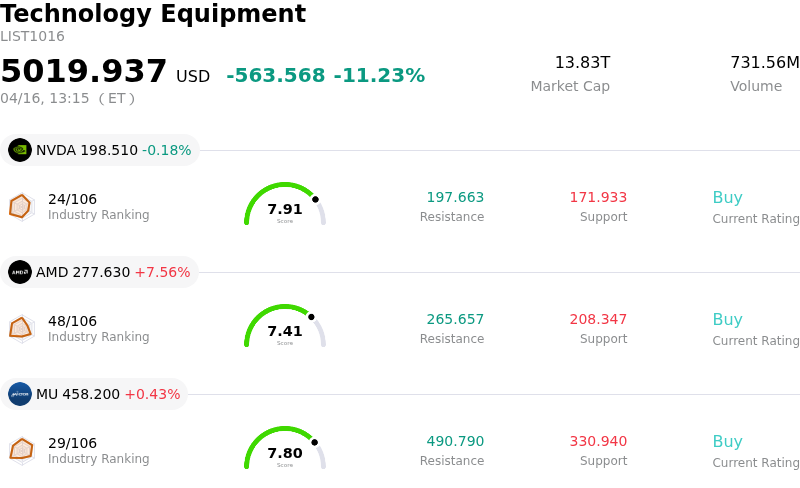

Taiwan Semiconductor Manufacturing Co Ltd Stock (TSM) Moved Down by 3.04% on Apr 16: Key Drivers Unveiled

Taiwan Semiconductor Manufacturing Co Ltd (TSM) moved down by 3.04%. The Technology Equipment sector is down by 11.23%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.18%; Advanced Micro Devices Inc (AMD) up 7.56%; Micron Technology Inc (MU) up 0.43%.

What is driving Taiwan Semiconductor Manufacturing Co Ltd (TSM)’s stock price down today?

Taiwan Semiconductor Manufacturing Co. (TSM) experienced notable intraday volatility today, concluding with a decline in its share price, despite reporting robust first-quarter 2026 financial results and providing an upbeat outlook. The company announced a record net profit that surged by 58% year-over-year, alongside a significant increase in revenue, which also surpassed both its own guidance and analyst expectations. Strong demand for advanced process technologies, particularly those driven by artificial intelligence (AI) applications, was highlighted as a primary catalyst for this strong performance. TSMC also raised its revenue growth forecast for the full year 2026 to more than 30% in U.S. dollar terms and indicated that capital expenditures would be at the higher end of its previously announced range, underscoring its confidence in the sustained AI megatrend.

However, the negative stock movement on a day marked by such positive earnings suggests that other factors may be influencing investor sentiment. One contributing element could be a "buy the rumor, sell the news" dynamic, where the strong financial performance was largely anticipated and potentially already priced into the stock after its substantial gains over the past year. Additionally, while TSMC expressed confidence in its near-term supply chain resilience, executives acknowledged that the ongoing Middle East conflict could eventually impact profitability through pressures on global shipping routes and energy costs. Concerns over rising costs for critical materials like helium, which has seen its spot price double, and tungsten, which has tripled, are also noted, even if TSMC has secured safety stock for the near term. These broader geopolitical risks and potential supply chain vulnerabilities, along with the disclosed expectation of a 2% to 3% gross margin dilution for the full year 2026 due to the ramp-up of new 2-nanometer technology and overseas fab expansions, might be tempering investor enthusiasm and leading to profit-taking. The March 2026 Consumer Price Index report, released on April 10, showed an increase in overall inflation and significant rises in energy prices, contributing to a broader macroeconomic backdrop of uncertainty.

Technical Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Technically, Taiwan Semiconductor Manufacturing Co Ltd (TSM) shows a MACD (12,26,9) value of [2.35], indicating a buy signal. The RSI at 62.63 suggests neutral condition and the Williams %R at -10.33 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Taiwan Semiconductor Manufacturing Co Ltd (TSM) is in the Technology Equipment industry. Its latest annual revenue is $122.22B, ranking 2 in the industry. The net profit is $55.12B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $415.64, a high of $550.00, and a low of $205.00.

More details about Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Company Specific Risks:

- Ongoing geopolitical tensions in the Middle East, including the closure of the Strait of Hormuz, pose an immediate threat to TSMC's supply chain, potentially leading to increased energy and critical material costs (such as helium and naphtha) and production disruptions.

- Projected margin compression stemming from substantial capital expenditures for new fabs and the ramp-up of advanced technologies like the 2-nanometer process, which is expected to dilute 2026 gross margins by 2-3%, as well as overseas fab expansions.

- Despite strong Q1 earnings, analysts and valuation models indicate that TSM shares are significantly overvalued (ranging from 33% to 43% above intrinsic value), suggesting a risk of market correction or limited upside if growth expectations are not continually exceeded.

- Approaching capacity limits for advanced-node production amidst surging AI chip demand raises concerns about potential operational bottlenecks and supply chain constraints, which could hinder future delivery capabilities and growth.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.