U.S. CPI Rises Slightly, Yet Markets Double Down on Rate Cut Bets: Decoding the Logic

TradingKey - On Thursday morning (U.S. Eastern Time), the U.S. Bureau of Labor Statistics released the July CPI report:

- Core CPI rose 3.1% year-over-year, the highest level in five months and above the 3.0% forecast.

- On a monthly basis, core CPI increased 0.3%, the largest gain since January and above the prior 0.2%.

- Headline CPI rose 2.7% annually, slightly below the 2.8% estimate but unchanged from the previous reading.

- Month-over-month, it rose 0.2%, in line with expectations but below the prior 0.3%.

Despite the hotter-than-expected core inflation, markets reacted in the opposite direction of traditional logic:

- Spot gold briefly spiked to $3,354 per ounce.

- The Dollar Index dropped more than 30 basis points.

- GBP/USD broke above 1.35, and USD/JPY fell below 148.

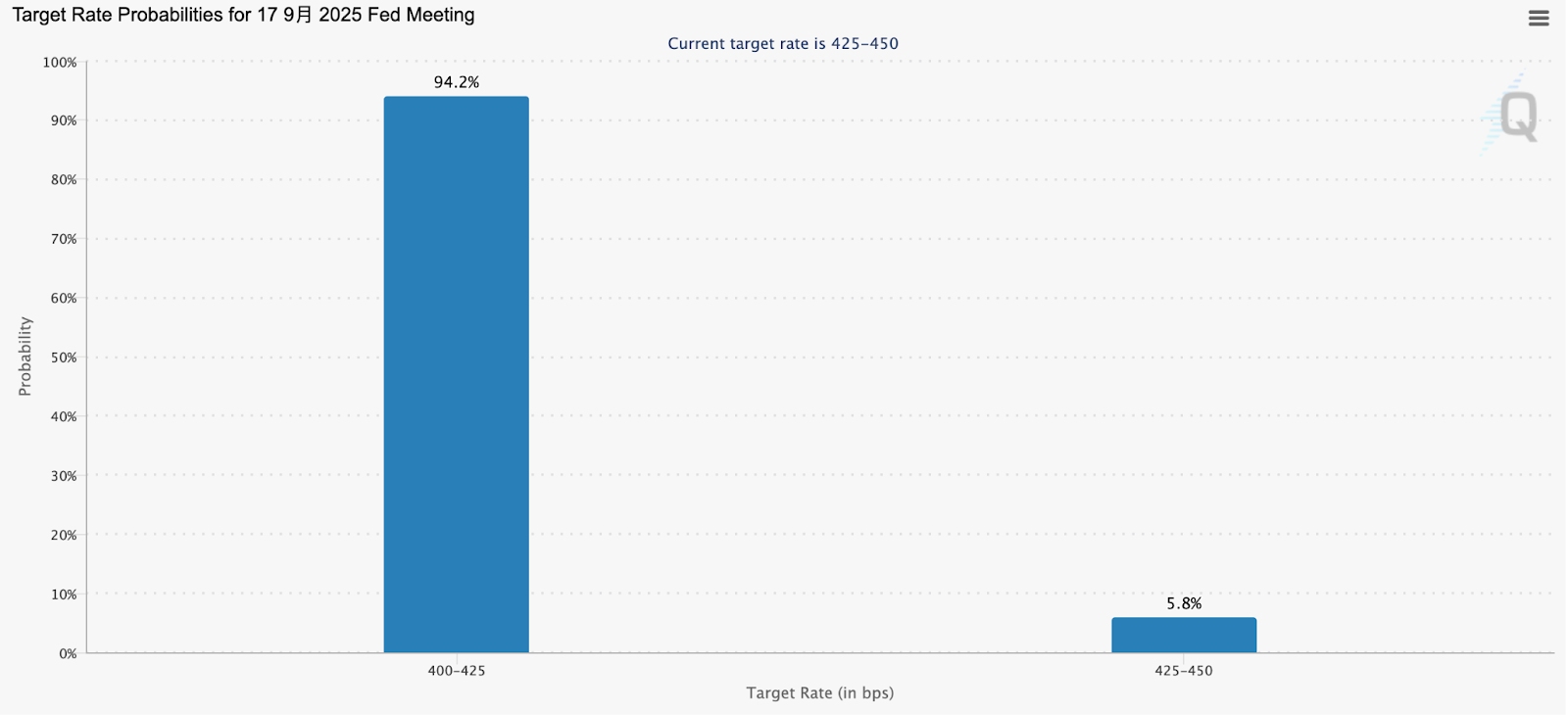

- Short-term Treasury futures declined, as traders significantly increased their bets on a September Fed rate cut, while maintaining expectations for another cut before year-end.

[Source: CME Group]

At first glance, the rise in core inflation signals persistent price pressures, especially in services and select goods, where price stickiness remains evident. Analyst Chris Anstey noted this was the first time in six months that monthly core CPI did not come in below expectations — suggesting inflation could re-accelerate, a development that would typically discourage the Fed from easing policy. He highlighted that prices for video and audio equipment surged sharply due to tariff impacts, posting the largest year-on-year gain since 2021. Traditionally, such signals would prompt the Fed to maintain higher rates for longer to guard against inflationary resurgence.

Yet the market’s reaction was the opposite. Analyst Jersey explained that the moderate headline CPI reflects continued declines in energy and certain food prices. More importantly, the Fed’s preferred inflation gauge — the PCE price index — is expected to approach the 2% target in the coming months. Combined with weakening labor and manufacturing data, the broader economic momentum is clearly slowing, shifting the Fed’s policy focus toward downside growth risks.

In reality, markets are not reacting to a single inflation print, but to the convergence of disinflation and economic deceleration. Recently, multiple Fed officials have signaled that a rate cut this year is possible, emphasizing the need to balance inflation control with growth preservation — a message the market has interpreted as a green light for earlier easing.

In this context, even though core CPI flashed a “yellow warning,” the broader trend remains one of easing inflation pressure, while the risk of economic slowdown is becoming more urgent. The Fed may now be more willing to act early to avoid a hard landing.

As a result, while the July CPI data showed a slightly “hotter” core reading, it did not shake confidence in a September rate cut. Instead, it reinforced expectations for a series of cuts before year-end.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.