Fed’s 2025 PCE Forecast Surpasses 3% – Peter Schiff: Rate Cuts Are the Cause, Not the Cure

TradingKey - Despite U.S. President Donald Trump's claims that high inflation does not exist, and his continued pressure on Federal Reserve Chair Jerome Powell to cut interest rates, the June FOMC meeting's Summary of Economic Projections (SEP) continues to signal rising stagflation risks, with the PCE price index expected to exceed 3% in 2025. Economists argue that further rate cuts will not help the U.S. economy.

On June 18, the Federal Reserve announced its decision to hold the federal funds rate steady for the fourth consecutive meeting, in line with expectations. In its latest statement, the Fed revised its assessment of economic uncertainty from “increased further” to “diminished but remains elevated,” removing language previously used to describe increasing risks of higher unemployment and inflation.

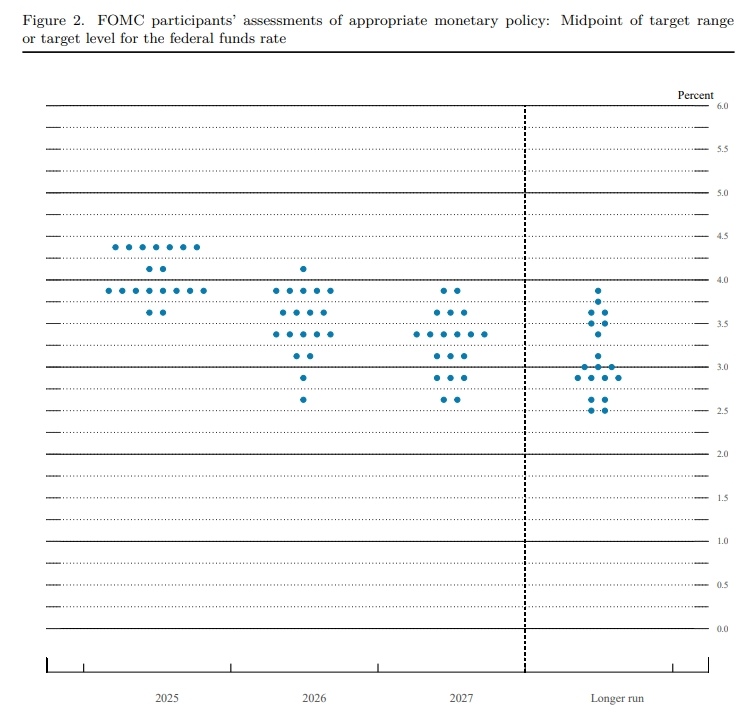

Nonetheless, the Federal Reserve’s economic projections and dot plot still reflect a hawkish tone. Although policymakers broadly maintain the baseline forecast of two rate cuts in 2025, the number of officials who expect no rate cuts at all increased from 4 to 7, while those forecasting only one rate cut rose from 2 to 4.

FOMC June Meeting Dot Plot, Source: Fed

In addition, FOMC members have become more concerned about stagflation. They have revised their 2025 GDP growth forecast downward from 1.7% to 1.4%, raised the unemployment rate forecast from 4.4% to 4.5%, and increased both the PCE inflation forecast and core PCE forecast from 2.7% to 3.0%.

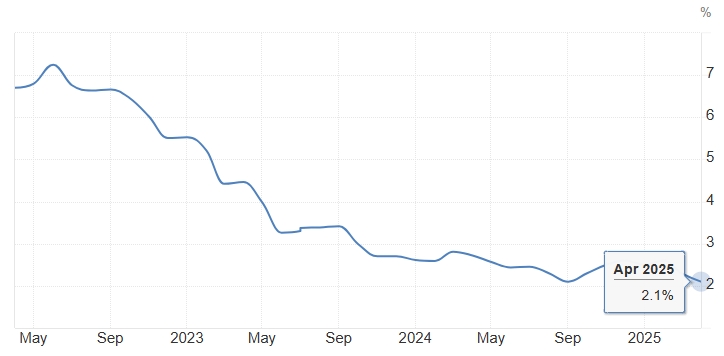

The last time the U.S. PCE inflation YoY reached 3% was in October 2023; as of April 2025, the PCE inflation rate stood at only 2.1%.

U.S. PCE YoY, Source: Trading Economics

The Fed’s upward revision of inflation expectations highlights the inflationary impact of Trump tariffs. After the meeting, Chair Powell stated that some tariff-driven inflationary effects are already visible and more are expected in the coming months.

U.S. Economic Outlook: Rate Cuts or Rate Hikes?

Before the FOMC meeting results were released, U.S. President Donald Trump once again criticized Powell, calling him a "fool" and accusing him of hurting the U.S. economy by refusing to cut interest rates. Trump said he wants U.S. borrowing costs to drop by at least two percentage points, and would be happy with a cut of 2.5 percentage points.

Trump’s calls for rate cuts have escalated over time — from initially demanding 100 basis points, then 200 basis points, now even 250 basis points. Some analysts believe this is more of a negotiation tactic than a genuine policy demand, similar to his approach on tariffs.

However, renowned economist Peter Schiff does not believe that the U.S. economy urgently needs rate cuts. During a TV program on June 18, he said actual inflation will likely far exceed the Fed’s forecasts, and the U.S. economy will perform far worse than expected.

Schiff pointed out that the root cause of current inflation is not just the recent imposition of high tariffs by Trump, but rather the accumulated inflationary pressures from more than a decade of loose monetary policy.

Due to years of low interest rates and quantitative easing, large amounts of U.S. dollars have been circulating globally. As foreign investors begin to withdraw capital from U.S. financial assets, more money is returning to the U.S., pushing up prices.

The economist warned that the U.S. may face a stagflation scenario — where both inflation and economic weakness coexist, making it extremely difficult to respond effectively.

Lower interest rates will not help the U.S. economy, he said, labeling them as the "cause."

He suggested that the real solution is to raise interest rates, even though it will bring significant pain — because the current U.S. economic system has been built on cheap money.

Schiff added that this would lead to a prolonged recession — including falling stock prices, declining real estate values, and widespread corporate bankruptcies — but it is inevitable, as the alternative could be even worse.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.