May Fed Meeting Preview: Diminishing odds of rate cuts to defy Trump’s rate cut dream

TradingKey – This Wednesday afternoon, May 7, the Federal Reserve will announce its latest monetary policy decision. Despite repeated pressure from U.S. President Donald Trump and some “soft data” pointing toward the case for rate cuts, solid inflation and employment figures—the so-called “hard data”—may actually raise the bar for any potential easing.

Market participants widely expect that the Federal Reserve will keep interest rates unchanged at its upcoming May meeting, holding the federal funds rate steady within a range of 4.25% to 4.50%. This would mark the third consecutive policy meeting in 2025 where the Fed maintains the status quo on interest rates.

In April, Trump's persistent calls urging Federal Reserve Chair Jerome Powell to cut rates triggered a debate over the central bank’s independence. Broadly speaking, Trump's push for looser monetary policy appears driven by his desire to lower borrowing costs, potentially offsetting the economic drag from tariffs and reducing the burden of refinancing U.S. government debt.

However, based on the current state of the Fed’s dual mandate—price stability and maximum employment—there appears to be little urgency for the Fed to ease policy anytime soon.

On the inflation front, the core PCE price index in March declined to 2.6% year-over-year from the prior reading of 2.8%, broadly in line with expectations. However, as noted by Wall Street Journal’s Nick Timiraos, while the 12-month PCE figure of 2.3% is approaching the Fed’s 2% target, three- and six-month annualized inflation remains around 3%.

In terms of labor market conditions, the U.S. economy added 177,000 jobs in April, surpassing expectations, while the unemployment rate held steady at 4.2%, as forecasted. According to Timiraos, this report shows no broad signs of job losses, and Fed officials are expected to remain cautious in their approach.

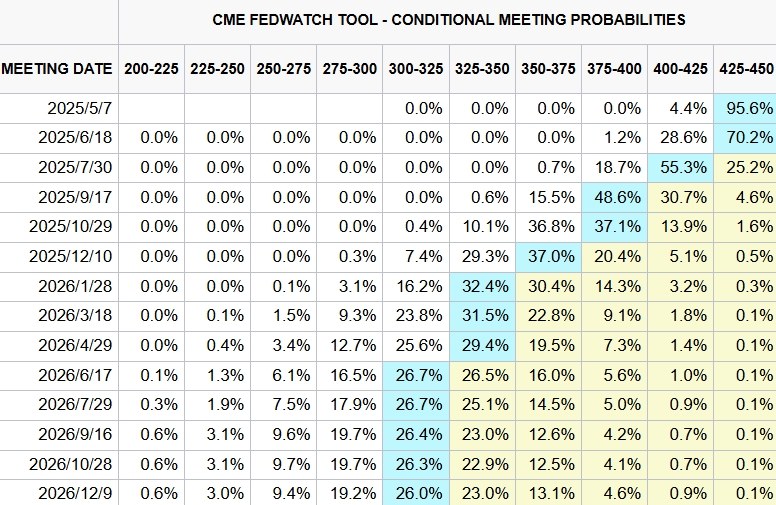

Following the release of the April nonfarm payrolls report, Goldman Sachs and Barclays both pushed back their forecasts for the first Fed rate cut of the year—from June to July.

Goldman Sachs noted that the current Federal Open Market Committee (FOMC) seems to have set a higher threshold for rate cuts than during the 2019 trade war. With both current inflation levels and survey-based inflation expectations running hotter than they were then, policymakers likely want to see more compelling evidence of an economic slowdown before shifting course.

JPMorgan Chase highlighted that Trump’s tariff policies could put the Fed in a dilemma—should inflation surge again before hard economic data clearly softens.

Currently, traders anticipate three rate cuts from the Fed this year, down from the four previously expected at the beginning of the month.

[Traders' bets on Fed policy path, Source: CME FedWatch Tool ]

Analysts at WisdomTree said that unless something negative happens between now and June, there would be no need for the Fed to take action.

A Hope for Four Rate Cuts This Year?

TradingKey Senior economist Jason Tang maintains that given the current backdrop of slowing economic growth, resilient labour markets, and ambiguous signs of reflation, we concur with this "hold" expectation. The focus will be on Chair Jerome Powell’s press conference remarks.

Beyond reiterating the Fed’s current stance, we anticipate Powell may adopt a mildly hawkish tone to counter President Trump’s attempts to influence monetary policy, reinforcing the Fed’s independence.

Looking ahead, economists widely anticipate that Trump’s high-tariff policies will create a “low growth, high inflation” environment, posing a policy dilemma for the Fed. Consensus expects the Fed to re-initiate a rate-cutting cycle in July 2025, with three cuts projected for this year. While we agree that high tariffs will exacerbate economic slowdown, we diverge on inflation expectations.

Although tariffs may drive price increases from the supply side, deteriorating economic prospects and weakening domestic demand are likely to cap inflationary pressures. Short-term inflation may fluctuate, but the broader trend toward the Fed’s 2% target remains intact. In a “low growth, low inflation” scenario, we project a more aggressive rate-cutting path than current market expectations—potentially four or more cuts in 2025. If this view gains traction, the U.S. dollar index could face sustained downward pressure.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.