Lucid Group Inc Stock (LCID) Moved Down by 7.18% on Apr 7: A Full Analysis

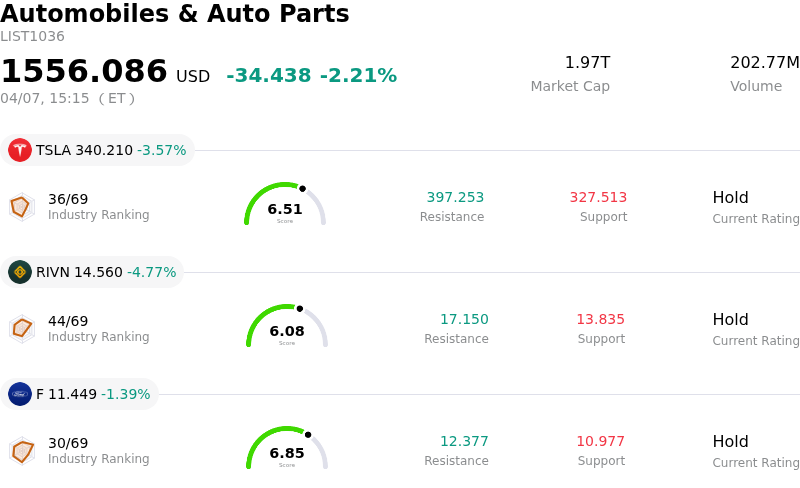

Lucid Group Inc (LCID) moved down by 7.18%. The Automobiles & Auto Parts sector is down by 2.21%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Tesla Inc (TSLA) down 3.57%; Rivian Automotive Inc (RIVN) down 4.77%; Ford Motor Co (F) down 1.39%.

What is driving Lucid Group Inc (LCID)’s stock price down today?

Lucid Group (LCID) experienced a notable decline in its share price, largely influenced by recent operational metrics and persistent concerns over its financial health. The company reported its first-quarter 2026 production and delivery figures, indicating 5,500 vehicles produced and 3,093 delivered, which fell short of analyst expectations of 5,967 vehicles produced and 5,237 delivered. This miss was primarily attributed to a 29-day disruption in Lucid Gravity deliveries due to a supplier quality issue concerning second-row seats, despite the company stating the issue has been resolved and reaffirming its full-year production guidance of 25,000-27,000 vehicles.

The reported delivery numbers represent a significant drop from the prior quarter, highlighting vulnerabilities in Lucid's supply chain management and its ability to meet customer demand, even for its highly anticipated Gravity model. This operational setback comes alongside ongoing investor apprehension regarding Lucid's financial performance. The company has demonstrated a consistent pattern of losing money on each vehicle sold, with a negative gross profit margin reported at -93%. Furthermore, Lucid recorded negative free cash flow of $3.8 billion in 2025, and its liquidity has decreased. Although the Public Investment Fund of Saudi Arabia continues to provide financial support, concerns about the company's long-term viability persist among some market observers.

Analyst sentiment remains mixed, with a consensus "Hold" rating as of April 6, 2026, and an average price target that suggests potential upside, yet a notable portion of analysts advise holding or selling. Some analysts have recently lowered price targets or downgraded the stock, reflecting caution. The stock also hit a 52-week low recently, underscoring the challenges it faces within the highly competitive electric vehicle market and broader economic pressures. Despite positive news like the Lucid Gravity receiving the 2026 World Luxury Car of the Year award and plans for a new, more affordable platform, these factors have not been sufficient to offset the immediate concerns stemming from production hiccups and financial results.

Technical Analysis of Lucid Group Inc (LCID)

Technically, Lucid Group Inc (LCID) shows a MACD (12,26,9) value of [-0.14], indicating a sell signal. The RSI at 42.95 suggests neutral condition and the Williams %R at -85.79 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lucid Group Inc (LCID)

Lucid Group Inc (LCID) is in the Automobiles & Auto Parts industry. Its latest annual revenue is $1.35B, ranking 43 in the industry. The net profit is $-3.79B, ranking 85 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $15.32, a high of $30.00, and a low of $7.50.

More details about Lucid Group Inc (LCID)

Company Specific Risks:

- Lucid Group missed Q1 2026 delivery estimates, delivering only 3,093 vehicles against expectations of over 5,200, due to a supplier quality issue with second-row seats for the Gravity SUV that halted deliveries for 29 days.

- The company issued a recall for 4,476 Gravity SUVs manufactured between December 2024 and February 2026 due to improperly welded seatbelt anchors, indicating potential quality control and safety concerns.

- Analyst sentiment reflects concerns about Lucid's extended path to profitability, with Morgan Stanley projecting gross profitability not before 2028 and ongoing EBIT losses through 2031, coupled with a significant dilution risk as the company may need to raise approximately $2 billion in equity by the second half of 2026.

- A substantial gap exists between Q1 2026 production of 5,500 vehicles and actual deliveries of 3,093, highlighting critical operational bottlenecks and inefficiencies in getting vehicles to market, which contributes to financial strain for the company.