AstraZeneca PLC Stock (AZN) Moved Up by 3.43% on Apr 1: Facts Behind the Movement

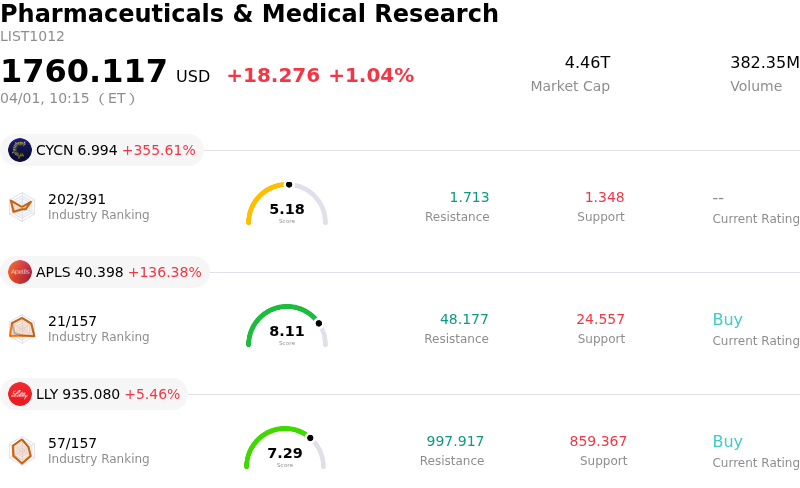

AstraZeneca PLC (AZN) moved up by 3.43%. The Pharmaceuticals & Medical Research sector is up by 1.04%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Cyclerion Therapeutics Inc (CYCN) up 355.61%; Apellis Pharmaceuticals Inc (APLS) up 136.38%; Eli Lilly and Co (LLY) up 5.46%.

What is driving AstraZeneca PLC (AZN)’s stock price up today?

The stock's upward movement today is primarily attributable to significant positive developments in the company's clinical pipeline and subsequent optimistic adjustments from market analysts. AstraZeneca recently announced favorable Phase 3 clinical trial results for its respiratory drug, tozorakimab, targeting Chronic Obstructive Pulmonary Disease (COPD). The OBERON and TITANIA trials demonstrated clinically meaningful reductions in COPD exacerbations and improvements in lung function, meeting their primary endpoints. This success is particularly noteworthy as other similar treatments from competitors have faced challenges in late-stage development, positioning tozorakimab as a potential leader in a therapeutic area with considerable unmet need. Market analysts have responded positively to these results, projecting that tozorakimab could generate substantial annual revenues, with some estimates ranging between $3 billion and $5 billion. This has led to an increase in investor confidence regarding a significant new revenue stream for the pharmaceutical giant.

In light of these encouraging trial outcomes, several Wall Street analysts have reiterated or adjusted their positive outlooks for AstraZeneca. On April 1, 2026, major firms maintained "buy" ratings for the stock and revised their price targets upwards, indicating continued confidence in the company's growth trajectory and pipeline strength. For instance, Leerink Partners raised its price target for AZN and increased its probability of success for tozorakimab in COPD. This aligns with the broader consensus among analysts who hold a "Moderate Buy" rating for the company.

While other news, such as mixed Phase 3 results for efzimfotase alfa in hypophosphatasia and the strategic delay of some European drug launches due to U.S. pricing pressures, were also noted around this period, the robust data from the tozorakimab trials appears to be the dominant driver for today's positive share price performance. The market seems to be weighing the potential of a major new drug approval more heavily than other less impactful or slightly mixed news. Additionally, institutional investors have shown increased interest in the company, with some firms raising their holdings during the previous quarter, reflecting a positive long-term sentiment.

Technical Analysis of AstraZeneca PLC (AZN)

Technically, AstraZeneca PLC (AZN) shows a MACD (12,26,9) value of [3.23], indicating a neutral signal. The RSI at 62.24 suggests neutral condition and the Williams %R at -0.34 suggests oversold condition. Please monitor closely.

Fundamental Analysis of AstraZeneca PLC (AZN)

AstraZeneca PLC (AZN) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $58.74B, ranking 8 in the industry. The net profit is $10.22B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $208.60, a high of $240.00, and a low of $120.00.

More details about AstraZeneca PLC (AZN)

Company Specific Risks:

- Ongoing legal challenges against the U.S. government's drug price negotiation program could impact future revenue streams in a key market.

- Discontinuation of the late-stage CAPItello-280 trial for Truqap in metastatic castration-resistant prostate cancer due to an unlikelihood of meeting primary endpoints signals a setback in the oncology pipeline.

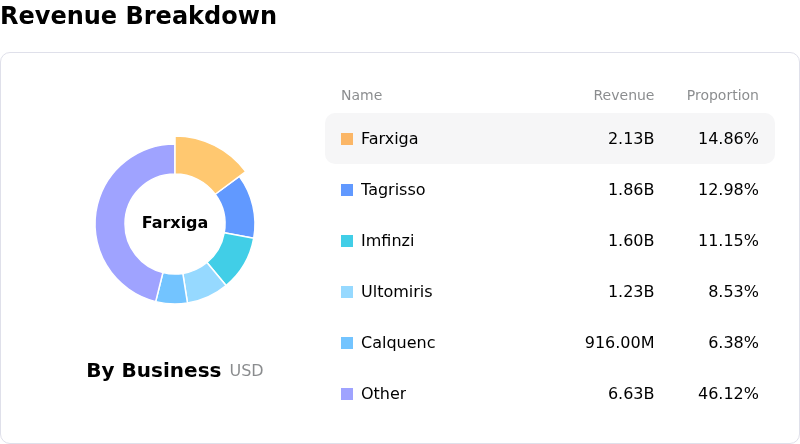

- The company faces material patent pressures beginning in the first half of 2026 with the expiration of Farxiga, a significant revenue-generating drug.

- Persistent concerns regarding an ongoing investigation into operations and alleged insurance fraud in the China market continue to pose legal and commercial risks.