Alibaba Group Holding Ltd Stock (BABA) Moved Down by 5.24% on Mar 27: A Full Analysis

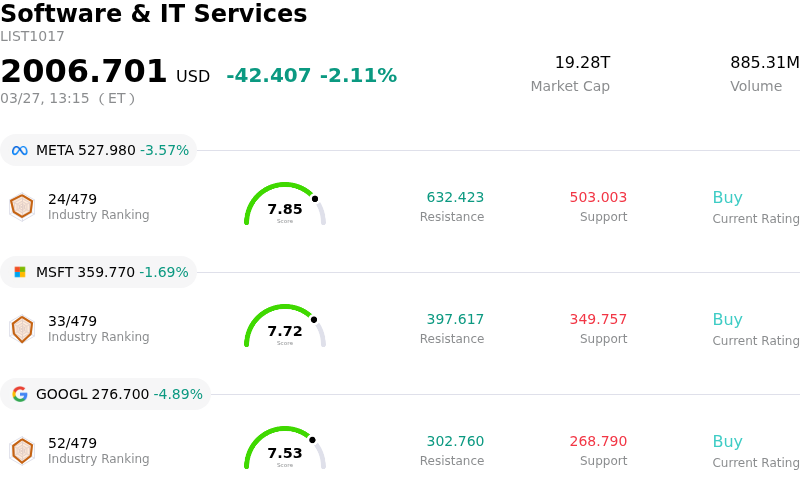

Alibaba Group Holding Ltd (BABA) moved down by 5.24%. The Software & IT Services sector is down by 2.11%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Meta Platforms Inc (META) down 3.57%; Microsoft Corp (MSFT) down 1.69%; Alphabet Inc Class A (GOOGL) down 4.89%.

What is driving Alibaba Group Holding Ltd (BABA)’s stock price down today?

Alibaba’s stock experienced a notable decline primarily driven by its recent third-quarter fiscal 2026 earnings report, which revealed significant profitability challenges despite revenue growth. The company reported results that fell short of analyst expectations for both revenue and earnings per share. While revenues saw a modest increase, non-GAAP net income and adjusted EBITA registered substantial year-over-year decreases. Free cash flow also declined significantly during the quarter.

The pronounced contraction in profitability is largely attributed to Alibaba’s aggressive investment strategy, particularly in its artificial intelligence initiatives and the rapid expansion of its quick commerce business. These heavy investments have led to a considerable surge in sales and marketing expenses, which consequently compressed near-term operating margins and free cash flow. Although the Cloud Intelligence Group demonstrated strong performance with accelerated revenue growth, especially from AI-related products, this strength was not sufficient to offset the broader deterioration in overall company profitability.

Following the disappointing financial disclosure, several investment analysts reacted by revising down their earnings per share estimates and lowering their price targets for Alibaba. For instance, Erste Group Bank decreased its FY2026 EPS forecast, and Zacks Investment Research placed Alibaba on its "Strong Sell" list. Susquehanna also adjusted its price target downward, specifically citing the impact of substantial AI spending on profits.

Adding to investor concerns is the intensifying competitive landscape within the e-commerce sector. Increased rivalry from other major players is contributing to higher costs for Alibaba to maintain its market position, further impacting its profitability. The market is also exhibiting apprehension regarding the timeline for these aggressive investments to translate into recovered profitability, creating uncertainty that fuels volatility.

Technical Analysis of Alibaba Group Holding Ltd (BABA)

Technically, Alibaba Group Holding Ltd (BABA) shows a MACD (12,26,9) value of [-6.76], indicating a neutral signal. The RSI at 34.04 suggests neutral condition and the Williams %R at -76.47 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Alibaba Group Holding Ltd (BABA)

Alibaba Group Holding Ltd (BABA) is in the Software & IT Services industry. Its latest annual revenue is $138.07B, ranking 5 in the industry. The net profit is $17.94B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $186.11, a high of $256.87, and a low of $112.00.

More details about Alibaba Group Holding Ltd (BABA)

Company Specific Risks:

- Alibaba's latest quarterly net income significantly declined by 66-67%, and analysts have subsequently decreased FY2026 earnings per share estimates, attributed to substantial investments in AI and quick commerce initiatives that are compressing near-term margins and free cash flow.

- The company faces intensified regulatory scrutiny, including ongoing U.S. probes into alleged data and AI ties with the Chinese military and EU scrutiny over its AliExpress platform for selling dangerous and counterfeit products, potentially leading to sanctions or increased compliance costs.

- Persistent margin compression is a concern due to aggressive spending in the "food delivery war" and significant capital allocation to AI and cloud, while core e-commerce revenue growth has slowed to a modest 2%, indicating market saturation and intense competition.

- Aggressive capital investments in AI and cloud segments introduce execution risk, with analysts expressing concern over the prolonged timeline to profitability and reports of executive departures within the Qwen AI division raising potential talent retention issues.