Lam Research Corp Stock (LRCX) Closed Up by 3.24% on Mar 17: Drivers Behind the Movement

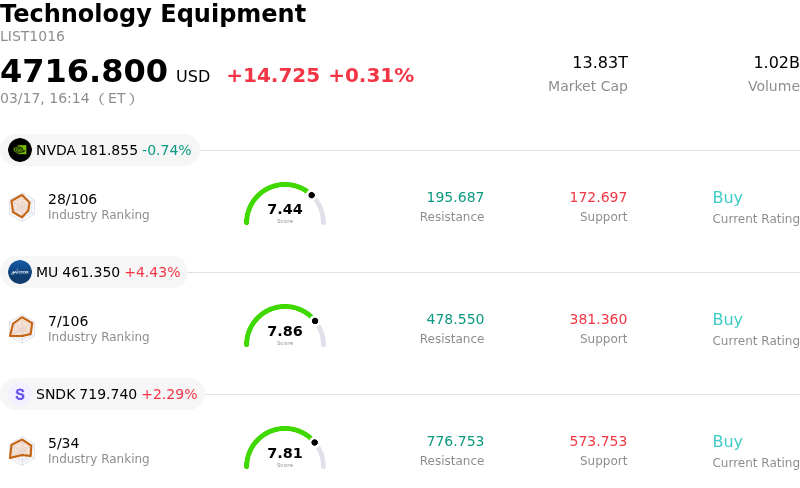

Lam Research Corp (LRCX) closed up by 3.24%. The Technology Equipment sector is up by 0.31%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.74%; Micron Technology Inc (MU) up 4.43%; SanDisk Corporation (SNDK) up 2.29%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

The significant upward movement in Lam Research (LRCX) shares today, reflecting an increase in its price, is largely attributable to a confluence of positive financial data, strong analyst sentiment, and favorable industry dynamics, particularly within the artificial intelligence (AI) sector.

The company's recent fiscal second-quarter 2026 results surpassed both revenue and earnings expectations, demonstrating robust operational execution. Lam Research reported revenues that exceeded consensus estimates and an increase in earnings per share. This strong financial performance was further bolstered by optimistic guidance provided for the third quarter of 2026, which projected healthy revenue and earnings per share.

Analyst forecasts have significantly contributed to the positive sentiment surrounding LRCX. Numerous analysts maintain a strong positive outlook, issuing "Buy" or "Strong Buy" ratings and revising earnings per share and price targets upwards. The consensus among analysts suggests significant potential for appreciation, with the average 12-month price target indicating a notable upside from current levels. This sustained confidence from the analytical community is a key driver for investor interest.

Moreover, the broader industry dynamics, particularly the surging demand for artificial intelligence (AI) infrastructure, are creating a highly favorable environment for Lam Research. The global Wafer Fab Equipment (WFE) market is anticipated to experience substantial growth in 2026, largely fueled by the AI boom, with projections reaching $135 billion. Lam Research is strategically positioned to capitalize on this expansion due to its leadership in critical areas such as advanced packaging, deposition, and etch capabilities, which are essential for AI-related technology transitions. The company's focus on scaling operational capacity and advancing its product roadmap is central to meeting this heightened semiconductor demand. Growth in advanced packaging is projected to exceed 40% in 2026, further emphasizing the company's strong position in key high-growth segments.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [-1.21], indicating a sell signal. The RSI at 48.66 suggests neutral condition and the Williams %R at -59.55 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $270.39, a high of $325.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Significant insider selling pressure has been observed in recent regulatory filings, with directors and the CFO reducing their stakes, potentially signaling cautious internal sentiment regarding future performance.

- Valuation models suggest the stock may be significantly overvalued, trading at peak cycle valuations (31X-40X forward P/E) compared to its historical mean, raising concerns about potential re-rating or consolidation if market momentum or operational execution falters.

- The company faces ongoing geopolitical and regulatory risks associated with its revenue concentration in China, where government-imposed export controls and a potential decline in revenue from the region could negatively impact gross margins and market share.

- Intensified competition within the semiconductor equipment industry, combined with U.S. government export controls, presents an external vulnerability as international competitors not subject to these restrictions could gain an advantage.