Western Digital Corp Stock (WDC) Moved Up by 5.76% on Mar 17: What Investors Need To Know

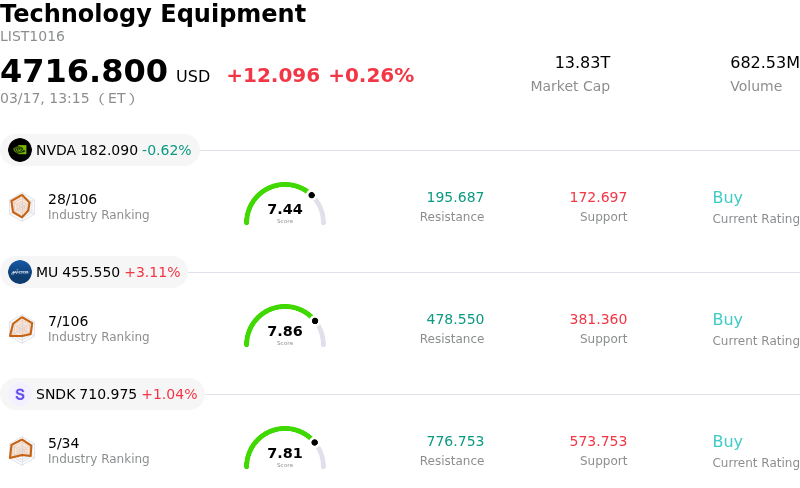

Western Digital Corp (WDC) moved up by 5.76%. The Technology Equipment sector is up by 0.26%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.62%; Micron Technology Inc (MU) up 3.11%; SanDisk Corporation (SNDK) up 1.04%.

What is driving Western Digital Corp (WDC)’s stock price up today?

The upward movement in Western Digital Corporation's stock today reflects a combination of robust industry tailwinds, strong company-specific performance, and optimistic market sentiment surrounding its strategic positioning. The overarching theme driving this positive momentum is the escalating demand for high-capacity storage solutions, primarily hard disk drives (HDDs) and NAND Flash, fueled by the explosive growth in artificial intelligence (AI), cloud computing, and hyperscale data centers.

Western Digital has reportedly achieved a significant milestone, with its HDD production capacity entirely sold out through the end of 2026. This "sold out" status is largely attributed to multi-year supply agreements with AI data centers and hyperscale customers, some extending into 2027 and 2028. This high demand and constrained supply environment is contributing to increased pricing power for the company and provides strong revenue visibility for the foreseeable future.

Recent financial reports have further bolstered investor confidence. The company has surpassed revenue and earnings per share estimates for both its first and second fiscal quarters of 2026, demonstrating strong year-over-year growth and improved gross margins. Management has also provided an encouraging outlook for the upcoming quarter, projecting continued strong revenue growth and healthy profitability. This consistent overperformance and positive guidance indicate effective operational execution in meeting the demands of the AI-driven data economy.

Analysts maintain a predominantly bullish stance on Western Digital, with a consensus "Moderate Buy" rating. Several firms have recently raised their price targets, acknowledging the company's strategic transformation and its critical role in the expanding AI infrastructure. This positive re-evaluation by the analyst community reinforces the optimistic market perception.

Furthermore, the company's strategic pivot to become a pure-play hard disk drive leader, following the separation of its Flash business in early 2025, is being viewed favorably. This focus allows Western Digital to concentrate on high-margin enterprise solutions for the AI era. Concurrently, Western Digital's commitment to shareholder returns, evidenced by its quarterly cash dividend program and share repurchases, also contributes to investor appeal.

Technical Analysis of Western Digital Corp (WDC)

Technically, Western Digital Corp (WDC) shows a MACD (12,26,9) value of [4.00], indicating a neutral signal. The RSI at 57.84 suggests neutral condition and the Williams %R at -19.06 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Western Digital Corp (WDC)

Western Digital Corp (WDC) is in the Technology Equipment industry. Its latest annual revenue is $9.52B, ranking 8 in the industry. The net profit is $1.84B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $316.01, a high of $440.00, and a low of $92.00.

More details about Western Digital Corp (WDC)

Company Specific Risks:

- Ongoing competitive and pricing pressures within the storage market, potentially leading to average selling price (ASP) declines and compression of future gross margins, despite recent expansion, due to the cyclical nature of the hardware business.

- Cautious capital expenditure plans, projected at only 4%-6% of sales, could restrict the company's ability to scale production to meet increasing demand, especially amidst an anticipated acceleration in technology roadmap development.

- The potential for industry oversupply poses a significant risk to the continuation of currently favorable market dynamics, despite strong demand for high-capacity drives, given the cyclical nature of the storage hardware sector.

- Heavy insider selling activity, with over 92,000 shares valued at approximately $24.3 million sold in the last 90 days, including recent significant transactions, may signal a lack of confidence from company executives and could weigh negatively on investor sentiment.