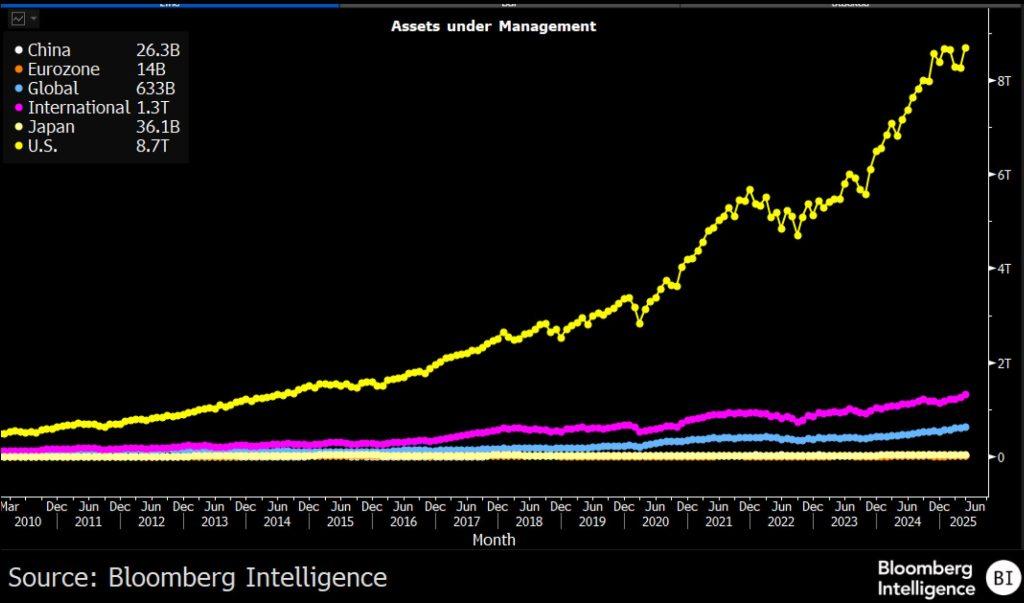

TradingKey - Global ETF assets have surpassed $16 trillion, with nearly $10 trillion flowing into U.S. markets—an allocation pattern reflecting the core role the U.S. market has played in driving ETF industry growth since 2010. The United States not only dominates ETF asset expansion but also delivers substantial long-term investment returns.

(Source: Bloomberg Intelligence)

ETFs have become the preferred tool for both institutional and individual investors thanks to their competitive fee structures, tax efficiency, transparency, and trading convenience. As one of the first ETFs to list in 1999, Invesco QQQ has witnessed the evolution of this investment vehicle from a professional niche to mainstream adoption.

However, ETF investing carries inherent risks. Many investors pursuing long-term wealth accumulation fall into common pitfalls due to insufficient knowledge or inadequate planning. Selecting the wrong products, misjudging risk profiles, or being misled by surface-level appearances can all lead to underwhelming results. For individuals aiming to achieve long-term financial goals, understanding these ETF investment traps is more crucial than merely focusing on opportunities.

This article systematically outlines seven common ETF investment misconceptions, enabling investors to identify potential risks and make more informed decisions in the market.

Misconception 1: Assuming All ETFs Are "Low-Volatility," "Low-Risk" Alternatives

A widespread market misconception equates ETFs with low-risk investments. While traditional index ETFs do offer relatively stable returns through diversification, the ETF universe spans vastly different risk profiles.

Today’s market features numerous complex, high-risk ETF products. For example, leveraged ETFs provide 2x or 3x index exposure—such as TQQQ (3x long Nasdaq-100) and SPXL (3x long S&P 500). Inverse ETFs like SQQQ (3x short Nasdaq-100) deliver returns opposite to their benchmark indices.

Though these products may amplify short-term gains, long-term holding often leads to severe losses due to two key factors.

First, the compounding effect of daily returns can produce negative outcomes in volatile markets: even if the underlying index ends flat, leveraged ETFs may incur losses from volatility decay. Second, the "volatility decay" caused by daily rebalancing makes it difficult for leveraged ETFs to maintain their stated multiples over time, causing long-term performance to diverge sharply from expectations.

When selecting ETFs, investors should carefully analyze their investment objectives, strategies, and potential risks—avoiding the trap of viewing ETFs as universally "safe" instruments. For high-leverage and inverse ETFs, it’s critical to recognize their role as short-term trading tools and avoid using them as core long-term holdings.

Misconception 2: Misunderstanding ETF Liquidity

Many investors mistakenly view an ETF’s average daily trading volume (ADV) as the sole metric for assessing liquidity. In reality, an ETF’s liquidity depends more heavily on the liquidity of its underlying assets.

Take QQQ as an example: as the second most actively traded ETF in the U.S. by daily volume, its liquidity advantage stems not only from high trading activity but also from the high liquidity of its underlying Nasdaq-100 index components, which are further supported by active futures and options markets.

When an ETF holds highly liquid underlying assets (such as U.S. large-cap stocks), it can absorb significant increases in trading demand without triggering major price swings—even if the ETF itself has low daily trading volume.

Conversely, if underlying assets are illiquid (e.g., certain small-cap stocks or high-yield bonds), even an actively traded ETF may exhibit wide bid-ask spreads and price volatility.

ETF liquidity is not determined solely by secondary market trading volume but arises from a unique dual-market structure. Investors trade ETF shares on exchanges in the secondary market, while authorized participants (APs) transact directly with ETF issuers in the "primary market" through creation/redemption mechanisms.

This structure enables ETFs to maintain strong liquidity even with low daily trading volumes. APs can instantly exchange baskets of underlying securities for ETF shares (or vice versa) based on demand, ensuring tight alignment between ETF prices and net asset value (NAV).

Liquidity-constrained ETFs may exhibit these risk characteristics:

- Premium/Discount Phenomena: ETF trading prices deviate significantly from NAV, potentially buying at a premium and selling at a discount

- Widening Bid-Ask Spreads: Increased gaps between buy and sell prices elevate transaction costs

- Heightened Price Volatility: Trades may trigger sharp price movements, degrading execution quality

(Source: Freepik)

Misconception 3: Passive ETFs Are Safer Than Active ETFs

The market widely believes passive ETFs are safer than actively managed ETFs—a view fraught with fundamental flaws. While it’s true that some actively managed ETFs are designed for short-term tactical trading (including leveraged and inverse products), an ETF’s risk profile ultimately depends on the characteristics of its underlying assets—not its management approach.

Whether an ETF uses passive replication or active strategies, its risk exposure is determined by asset class, sector allocation, and individual security selection.

The core value of actively managed ETFs lies in professional teams leveraging deep market analysis and research capabilities to dynamically evaluate opportunities and risks. This flexibility allows managers to adjust portfolios in response to changing markets, identify sectors and companies with relative advantages, and avoid areas with elevated downside risks. This active oversight enhances adaptability and risk control.

In contrast, passive ETFs rigidly track specific indices’ compositions and weights, lacking responsiveness to market shifts. When indices include overvalued or high-risk assets, passive ETF investors cannot mitigate these exposures through active decisions—a limitation that may amplify losses during systemic downturns.

Investors should look beyond the passive/active dichotomy to analyze underlying asset quality, sector allocation, and risk characteristics. An actively managed ETF invested in stable assets may provide superior risk control compared to a passive ETF blindly tracking its index—the key lies in the quality and adaptability of the underlying holdings.

Modern ETF markets offer diverse strategic options. Many actively managed ETFs are designed for long-term core holdings, emphasizing risk management and sustainable value creation. Professional institutions often combine these active ETFs with passive products to build more resilient portfolios.

Misconception 4: Historical Performance Accurately Predicts Future Returns

A pervasive misconception in ETF investing is overreliance on historical performance as the primary decision-making criterion. Financial advisors universally emphasize that ETF selection should align with an investor’s personal risk tolerance, financial goals, and time horizon—not past returns alone.

Many investors fall into the "chasing historical performance" trap, mistakenly treating past results as reliable predictors of future gains. This cognitive bias often leads to excessive concentration in market hotspots—such as the rapid inflows into Bitcoin or clean energy ETFs during their peak performance periods.

This behavior carries significant risks. ETFs in trending sectors often exhibit high volatility, with prices surging rapidly but also collapsing just as quickly. Investors frequently overlook the time horizon and consistency behind performance metrics, misinterpreting short-term market sentiment as sustainable opportunities. True value assessment requires evaluating performance sustainability and stability—not isolated high-return periods.

Historical data confirms that top-performing ETFs rarely maintain leadership. ETF price movements are driven by multiple factors: market sentiment, industry cycles, and macroeconomic conditions. Investors lacking a deep understanding of these dynamics risk substantial losses when attempting to time markets by chasing short-term performance.

Professional guidance should steer investors toward long-term strategies and comprehensive due diligence—not market fads. For those requiring short-term trading tools, advisors can recommend products explicitly designed for tactical use, rather than misapplying them as long-term holdings. Investment decisions must be grounded in thorough understanding of product mechanics—not dazzled by recent returns.

Misconception 5: Believing Frequent ETF Trading Doesn’t Impact Returns

ETFs function as highly liquid investment vehicles, allowing investors to trade assets throughout the day just like stocks. However, this convenience often leads to excessive trading, causing investors to overlook how frequent transactions materially erode investment returns.

The core advantage of ETFs lies in their low-cost structure and tax efficiency—not their suitability as short-term trading instruments. When investors treat ETFs as speculative chips rather than foundational long-term portfolio components, overtrading inevitably undermines overall performance. This behavior appears flexible but silently diminishes investment outcomes.

A Morningstar research report published in August 2024 exposed the severity of this issue: over the past decade, average annual returns for U.S. open-end fund and ETF investors stood at 7%, significantly trailing the 8.2% annual total return of the funds themselves. This 1.2 percentage point "investor return gap" stems primarily from poor market timing and excessive trading behavior.

Frequent ETF trading generates multiple layers of costs, including transaction commissions, capital gains taxes, and hidden trading expenses. These fees compound over time, gradually eating into investment gains.

Every portfolio adjustment incurs additional transaction costs that directly reduce net returns, creating a significant gap between expected and actual outcomes. In the long run, this "trading decay" effect can severely damage portfolios—contradicting the original purpose of ETFs as long-term investment vehicles.

(Source: Freepik)

Misconception 6: Assuming a Low Share Price Equates to Better Value

Investors often mistakenly believe that a low ETF share price (such as $10–$30) indicates superior investment value—a cognitive error mirroring value traps in stock investing.

This perspective ignores that investment decisions should center on yield and per-unit value creation efficiency—not surface-level price numbers. For example, an ETF with a $50 share price delivering an 8% annualized return holds far greater investment value than a $5 share price ETF losing 20% annually. These products exhibit fundamentally different investment outcomes.

An ETF’s share price inherently reflects the division ratio of its underlying assets—not the intrinsic value of those assets. The pricing mechanism is primarily determined by fund sponsors based on operational strategies, akin to slicing the same cake into different portions.

Regardless of per-share price, the proportional asset exposure and intrinsic value remain consistent. Thus, ETF price levels alone cannot serve as valuation metrics; the critical factors are the effectiveness of investment strategies and long-term performance.

Investors should focus on an ETF’s actual yield, fee structure, and risk-return profile rather than being misled by superficial pricing. The magnitude of net asset value per share merely represents the fractional allocation method of assets—it does not affect overall investment value.

Misconception 7: Buying Sector-Themed ETFs Simply Because You’re Bullish on an Industry

Sector-themed ETFs indeed offer convenient entry points for targeted exposure to specific fields like artificial intelligence, biotechnology, and renewable energy.

However, these ETFs often suffer from highly concentrated holdings—a single AI-themed ETF might allocate over 30% of assets to one technology giant, far exceeding basic diversification principles. When market conditions shift, such concentration exposes investors to risks vastly exceeding industry averages.

Moreover, while these ETFs target specific sectors, their performance is frequently swayed by broader macroeconomic factors. Even with strong fundamentals in a niche industry, interest rate policy changes, geopolitical tensions, or economic cycle shifts can pressure entire sectors, causing investors to miss expected returns.

Liquidity issues also plague many thematic ETFs. Due to low trading volumes, these products often exhibit wide bid-ask spreads that directly increase transaction costs—particularly during market volatility, where such costs can significantly erode returns.

Many thematic ETFs have short track records, lacking sufficient historical data for comprehensive long-term performance assessment. These products are frequently used for speculative market trends; when sentiment shifts, they often become the first targets for capital outflows, leaving late-entering investors vulnerable to "buying at peak prices."