South Korean Stock Plunge Drags Down US Stocks: SanDisk Slumps 12%, SK Hynix Drops Over 10%, Memory Sector Suffers Irrational Sell-Off

AI Podcast

On July 13, Eastern Time, the memory sector experienced a broad sell-off, driven by a decline in South Korean markets and SK Hynix’s earnings forecast downgrade by Korea Investment & Securities (KIS). Despite the 8% profit miss, fundamentals remain robust; the shortfall reflects long-term supply agreement pricing structures rather than weakening demand. The industry is transitioning toward high-value, long-term contracts, smoothing earnings cycles. Simultaneously, Goldman Sachs reiterated a "Buy" rating for SanDisk, citing persistent NAND shortages and strong demand. The current market volatility is viewed as an earnings rhythm adjustment rather than a fundamental shift in memory demand.

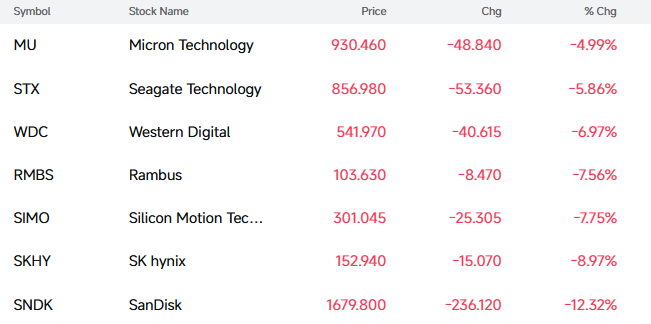

TradingKey - On July 13, Eastern Time, the memory stock sector suffered an overall setback today. As of press time, SanDisk ( SNDK) fell 12.32%, SK Hynix ( SKHY) fell 8.97%, Western Digital ( WDC) fell 6.97%, Seagate Technology ( STX) fell 5.86%, Micron Technology ( MU) fell 4.99%.

Notably, the decline in the memory sector is inextricably linked to the sell-off in the South Korean stock market—South Korea's KOSPI plunged over 8% to trigger a circuit breaker, SK Hynix plummeted 15%, and Samsung fell over 10%.

[Source: FutuBull]

Market analysis indicates that this round of sell-off was mainly due to profit-taking following SK Hynix's listing on the US stock market, as well as the downgrade of its earnings forecast by Korea Investment & Securities (KIS).

Specifically, KIS's latest forecast shows that SK Hynix's revenue for the second quarter of 2026 will reach 80.9 trillion Korean won, up 54% quarter-on-quarter and surging 264% year-on-year; operating profit is expected to reach 60.4 trillion Korean won, up 61% quarter-on-quarter and skyrocketing 556% year-on-year.

However, this performance is below the market consensus: operating profit was revised down by about 8% from the previous consensus of 65 trillion Korean won. Following the announcement, the market's core focus quickly shifted to "earnings missing expectations," which triggered today's sell-off of South Korean stocks.

Nic Puckrin, founder of Coin Bureau and a cross-asset analyst, wrote in a report: "Today's near-record decline of SK Hynix during Asian trading hours is no longer just a South Korean issue; it is now injecting this volatility into Nasdaq."

He stated: "In fact, the two markets are becoming more intertwined than ever, influenced by each other's concentration of technology stocks. This is a vicious cycle that should worry equity investors."

However, digging deeper into KIS's research report, it is clear that the forecast adjustment does not stem from a slowdown in HBM demand, but rather from temporary disruptions caused by changes in product structure and pricing models. In the second quarter, the proportion of SK Hynix's HBM shipments continued to rise, but the prices of such products had been locked in advance through long-term supply agreements (LTAs), resulting in an average selling price (ASP) below the market spot price level during the same period.

Simply put, the current memory market is in a rapid upward price channel, with spot prices for traditional DRAM and NAND rebounding sharply. Meanwhile, SK Hynix, having locked in prices for HBM orders in advance, cannot fully benefit from the marginal revenue gains brought by the short-term price surge.

However, this impact is only a short-term difference in earnings rhythm. As HBM4 officially enters the mass shipment phase in the third quarter, the volume expansion of the next-generation high-value products will optimize the product mix and push the overall ASP further upward. KIS calculations show that the average selling prices of DRAM and NAND flash memory in the second quarter rose by approximately 30% and 50% respectively compared to the first quarter, indicating that the tight supply-demand dynamics in the memory industry have not fundamentally changed.

The firm downgraded its operating profit forecasts for 2026 and 2027 by 9% and 11%, respectively. The core reason is not deteriorating fundamentals, but rather that institutions have begun to revise their earnings calculation models based on the framework of long-term supply agreements. Unlike past memory cycles that heavily relied on spot prices, the memory industry in the AI era is transitioning to a new model of "long-term agreement lock-ins + high-value products." Long-term contracts enhance demand certainty and earnings visibility, but they also smooth out the earnings peaks during periods of skyrocketing prices.

Notably, Goldman Sachs raised its price target for SanDisk from $1,200 to $2,200 and reiterated its "Buy" rating. The bank forecasts that SanDisk is about to report very strong quarterly results.

Goldman Sachs believes that the global shortage of NAND flash memory chips will persist into 2026, with a simultaneous recovery in demand from mobile, PC, and data center segments. Meanwhile, production capacity is being squeezed by the high-end AI memory sector, leaving conventional products undersupplied and market prices on an upward trajectory. SanDisk's management revealed at the Mizuho Technology Conference in early June that even at the low end of the price range for New Business Model (NBM) agreements, "we like these margins" and they "will be consistent with the margins guided for the fourth quarter."

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.