Fed May Raise Rates in September: Waller Says June CPI Will Determine Rate Policy Path, 5-Year Treasury Yield Surges to Break Recent Highs

AI Podcast

Federal Reserve Governor Christopher Waller recently signaled a hawkish shift, warning that persistent core inflation may necessitate further rate hikes. This stance challenges market expectations for near-term policy easing. While the labor market remains stable, policymakers fear repeating past delays in addressing price pressures. Internal FOMC support for rate increases is rising, with markets now pricing in potential hikes for September. As US inflation proves resilient due to broad-based economic factors, Treasury yields have surged, reflecting a "higher for longer" policy outlook. Investors remain focused on upcoming CPI data to calibrate market valuations and policy pivot timing.

TradingKey — The latest remarks from Federal Reserve Governor Christopher Waller sent a clear hawkish signal, stating that if core inflation remains elevated, the Fed does not rule out tightening monetary policy in the near term. This directly shattered the market's previous easing expectations of a policy shift toward rate cuts.

Waller noted that if subsequent economic data indicates inflation remains significantly above the 2% policy target, the Fed may need to raise interest rates further in the near term, adding that monetary policy is currently at a critical "crossroads." He pointed out that the direction of policy will be determined by incoming economic data, including Tuesday's CPI report.

While he does not advocate for premature rate hikes to avoid triggering a recession, he also emphasized that the current labor market is running smoothly. Therefore, the Fed must avoid repeating the mistake of a few years ago—being slow to react and delaying action when upward price pressures were building.

Waller admitted that the current labor market is far less hot than during the Fed's 2022–2023 rate-hiking cycle, and there is a "credible basis" to believe that inflation could continue to cool even without further policy tightening. However, he pointed out that relying solely on businesses' and investors' expectations of falling inflation is insufficient to justify the Fed remaining on the sidelines. If the Fed waits until market confidence gradually fades before taking action, it would be forced to play catch-up with more aggressive rate hikes.

According to the minutes of the Fed's June meeting released last week, although the Federal Open Market Committee (FOMC) unanimously voted to hold interest rates steady last month, a minority of officials already supported a rate hike. The latest economic projections show that half of the 18 policymakers expect at least a 25-basis-point rate hike this year, indicating that internal hawkish sentiment is rising.

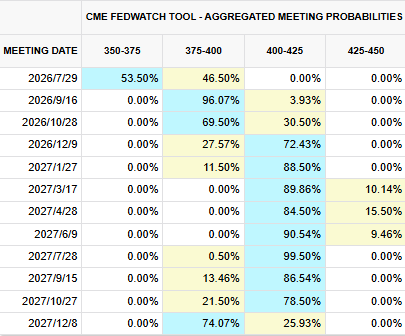

According to the CME FedWatch Tool, the market has now fully priced in a single rate hike by the Fed in September, while the probability of a rate hike at the end of this month is as high as 46.5%.

[Source: CME FedWatch]

For the secondary market, tomorrow's CPI data will directly calibrate market expectations for rate hikes. If core inflation once again exceeds expectations, Treasury yields and the US dollar are highly likely to strengthen, putting pressure on the valuations of growth-oriented risk assets and further delaying the timing of the Fed's policy pivot.

Currently, US inflation resilience has far exceeded expectations. The core PCE index, the Fed's preferred inflation gauge, rose to 3.4% year-over-year in May. This index has climbed steadily since January, with the upward trend beginning even before the outbreak of the US-Iraq war. This suggests that inflationary pressures are not driven solely by geopolitical and energy factors; rather, multiple forces, including tariffs and the expansion of AI infrastructure, are driving broad price pressures.

While the CPI data will be officially released tomorrow, US Treasury yields have already completed the market's expected pricing ahead of the data. The 2-year US Treasury yield, a bellwether reflecting short-term monetary policy, rose 55 basis points today to reach 4.273%. Meanwhile, the 5-year Treasury yield, which reflects market expectations for the monetary policy path and medium-term inflation over the next 3 to 5 years, rose 60 basis points today to a high of 4.374%, breaking its recent high set on May 19. The 10-year Treasury yield, the anchor of risk-free rates in financial markets, rose 52 basis points to a high of 4.618%.

This implies that the market is revising its short-term expectations for rate cuts, believing the Fed will maintain higher interest rates for longer, although expectations for long-term economic growth and inflation have not been revised upward significantly at the same time.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.