US June CPI Preview: Can Cooling Inflation Open Up Fed Rate Cut Expectations? How Will US Stocks, the Dollar, and Gold React?

AI Podcast

The upcoming June US CPI data is a critical catalyst for global markets. Investors expect headline CPI to cool to approximately 3.8% due to lower energy costs, yet core CPI remains the primary focus for gauging underlying inflation persistence. Goldman Sachs projects a modest decline, signaling potential caution. Sticky core inflation would likely reinforce hawkish Federal Reserve expectations, supporting the US dollar and pressuring gold and growth stocks. Conversely, a significant core CPI surprise could lower Treasury yields, boosting risk assets and gold. Long-term forecasts suggest inflation may stay above the Fed’s 2% target, complicating the policy outlook.

TradingKey - The United States will release June Consumer Price Index (CPI) data this Tuesday, which is one of the most critical macroeconomic events in global financial markets this week. As US inflation heated up significantly in May, and with recent Middle East tensions, oil price volatility, Federal Reserve meeting minutes, and non-farm payroll data collectively altering market expectations, the June CPI will significantly impact the Fed's next policy judgment, while also directly determining the short-term direction of US stocks, the US dollar ( USD) and gold ( XAUUSD ).

Markets Focus on June Core CPI

From the perspective of market expectations, investors generally expect June headline CPI to cool down significantly from May. Previously, May CPI rose 4.2% year-on-year, a relatively high level over the past nearly three years, driven primarily by a sharp rise in gasoline and energy prices. Core CPI rose 2.9% year-on-year and 0.2% month-on-month, showing that although price pressures excluding food and energy are lower than headline inflation, they remain some distance away from the Federal Reserve's 2% target. Entering June, as oil prices pulled back at one point and energy price pressures eased, the market expects headline CPI could retreat from May's 4.2% to around 3.8%, and could even register a slight decline month-on-month.

However, what truly determines the market response is not headline CPI, but core CPI. This is because energy prices are highly volatile and easily influenced by the situation in the Middle East and short-term fluctuations in oil prices, whereas the Fed is more focused on the persistence of inflation. If June core CPI remains around 2.9%, it would indicate that services inflation, housing costs, insurance, medical care, and other core items remain sticky, meaning the Fed may not quickly pivot to a dovish stance just because headline CPI declines. Conversely, only if core CPI month-on-month is significantly below expectations will the market truly believe that inflationary pressures are easing.

Regarding institutional views, Goldman Sachs expects June core CPI to rise by about 0.17% month-on-month, slightly below the market consensus, and projects that core CPI year-on-year may decrease from 2.9% to 2.8%. On headline CPI, Goldman Sachs expects that, driven by falling energy prices, June headline CPI may decrease by about 0.11% month-on-month and fall back to around 3.87% year-on-year. This implies that if the data aligns with Goldman Sachs' expectations, inflation will appear to cool on the surface, but the decline in core inflation will not be significant, and the market may still remain cautious.

Over a longer horizon, the Philadelphia Fed's second-quarter Survey of Professional Forecasters shows that economists have significantly raised their 2026 inflation expectations, projecting fourth-quarter-over-fourth-quarter headline CPI and core CPI for 2026 at 3.5% and 2.9%, respectively. This indicates that the market currently does not expect inflation to quickly return to 2%, but rather tends to believe that U.S. inflation will remain above the Federal Reserve's target for some time.

How US Stocks, US Dollar and Gold React in Short Term After CPI Data?

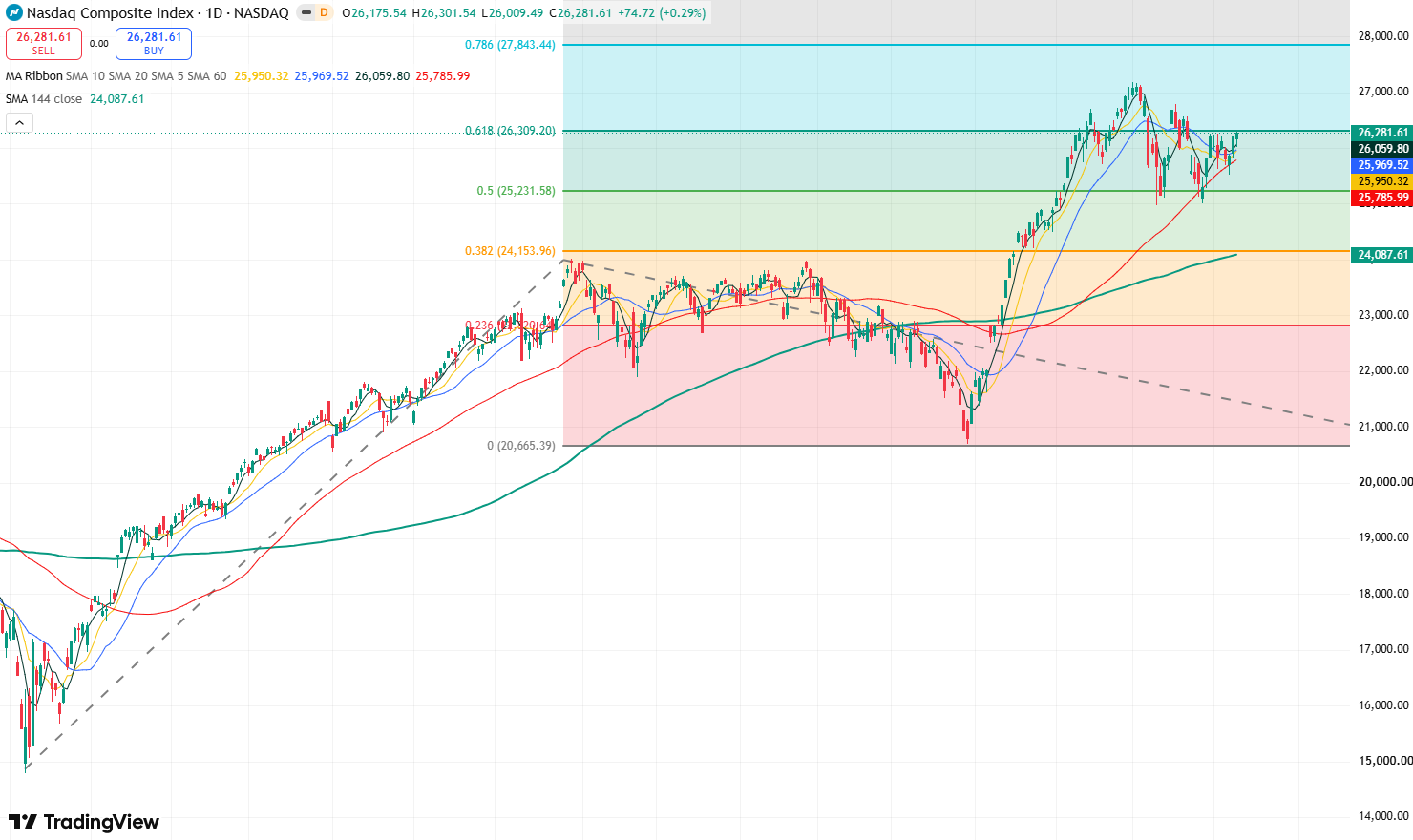

For US equities, the impact of June's CPI will be primarily reflected in interest rate expectations and valuation levels. If CPI is lower than expected, especially if core CPI cools significantly, US Treasury yields could fall, easing market concerns about Fed rate hikes, which would benefit tech stocks, AI concept stocks, and growth stocks. The Nasdaq and S&P 500 could regain momentum for valuation expansion, and investor risk appetite could also improve, potentially supporting the Nasdaq to hit new historic highs. Conversely, if core CPI is higher than expected, the market may again bet on the Fed raising rates within the year or keeping interest rates higher for longer, which would weigh on growth stock valuations, and US equities could experience a pullback. Financial stocks may show mixed performance; while high interest rates benefit net interest margins, the banking and consumer sectors could also come under pressure if inflation reinforces fears of an economic slowdown.

Nasdaq Index Daily Chart, Source: TradingView

For the US dollar, a CPI higher than expected is usually a direct positive. If both headline and core CPI are stronger than expected, the US Dollar Index could rebound quickly as the market prices back in a hawkish Fed policy path. MUFG also noted that unless US inflation slows down enough to alter Fed expectations, the rebound in Asian currencies may be unsustainable; if US inflation beats expectations again, it will reinforce the market's bullish bias toward the US dollar. Conversely, if CPI is significantly lower than expected, especially if core CPI declines in tandem, the US dollar could face downward pressure.

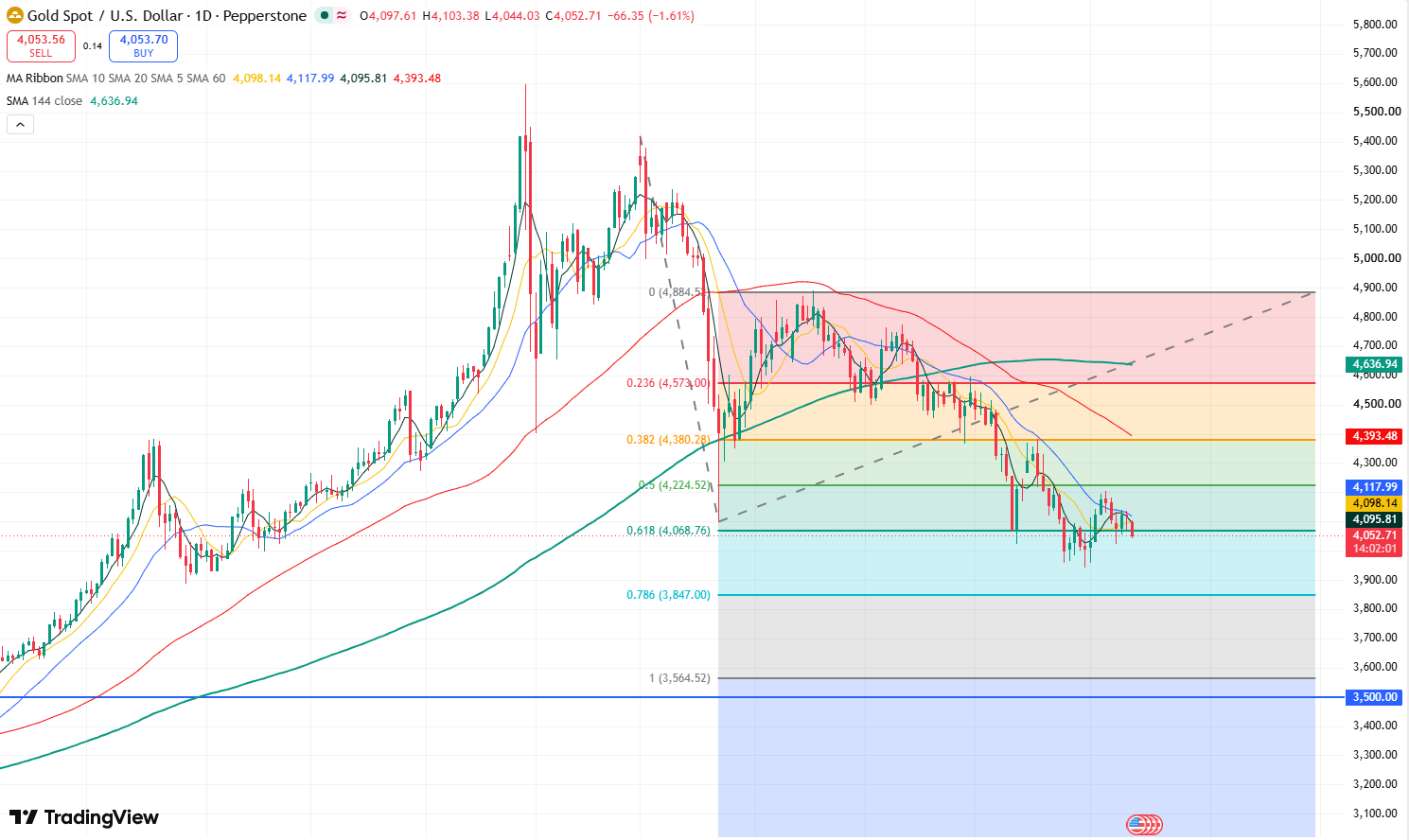

Gold Price Daily Chart, Source: TradingView

For gold, as a non-yielding asset, it is highly sensitive to real interest rates. If June CPI is lower than expected, cooling market expectations of Fed rate hikes, and sending US Treasury yields and the USD lower, gold is expected to find support and rally again, potentially continuing to test the $4,200 resistance level. Conversely, if core CPI is stronger than expected, upward pressure on real interest rates will weigh on gold, and gold prices may extend their recent downward trend to further test the $4,000 mark, or even fall below $4,000 to slide further toward $3,900.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.