Hold or Diversify? Why This Forgotten Industry Deserves a Look

AI Podcast

The S&P 500's April 2026 performance of 10.42%, driven by tech, was the best since 2020. Investors face holding tech-heavy portfolios, selling, or diversifying. While tech momentum persists, risks like geopolitical uncertainty and inflation loom. Market timing is discouraged. Diversification into less correlated sectors like healthcare offers a hedge. Healthcare, historically underperforming, presents value and is insulated from economic downturns. The GLP-1 drug trend shows significant growth potential despite regulatory and pricing concerns. The State Street Health Care Select Sector SPDR ETF (XLV) and individual stocks like Eli Lilly and Novo Nordisk are investment avenues.

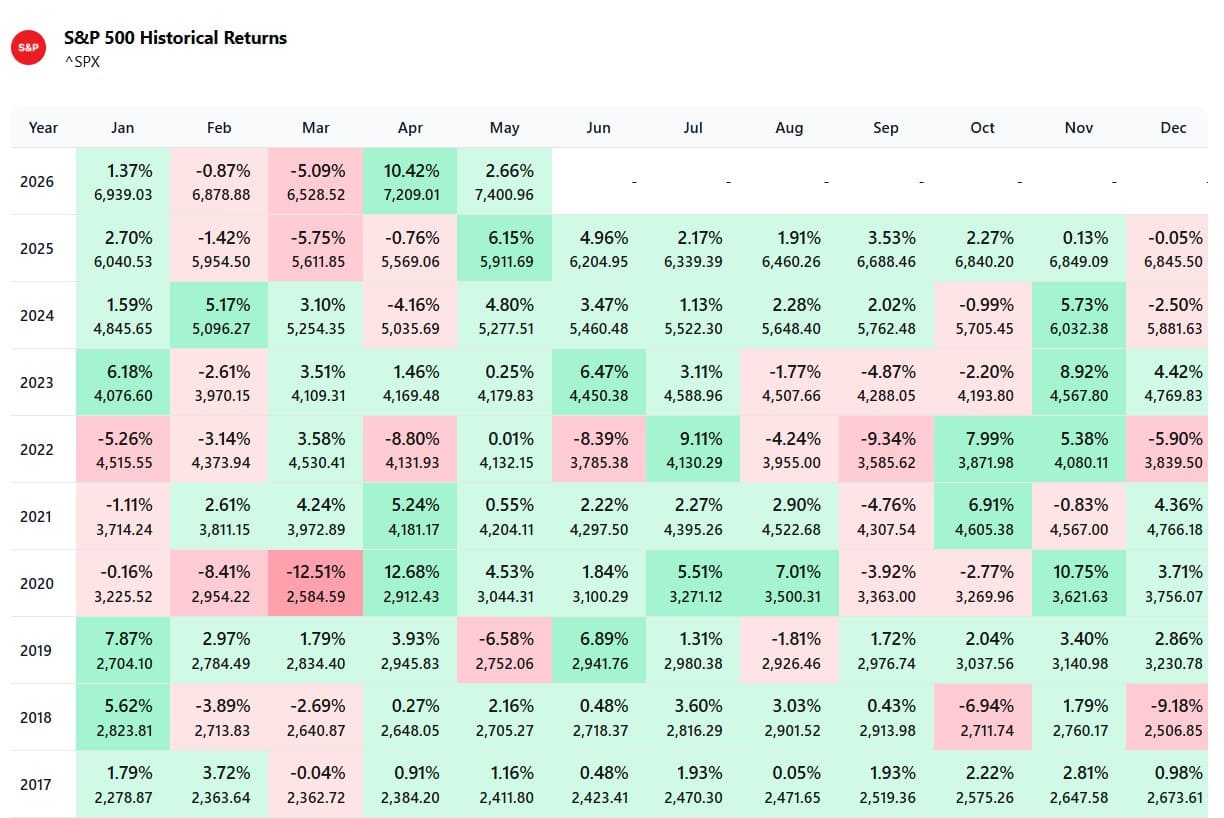

Recent market performance has been more than just strong. In April 2026, the S&P 500 returned 10.42% - this is a great performance. In fact, this is the fifth-best month for the S&P 500 in the past 40 years, and the best one since 2020.

Period | Performance | Reason |

April 2020 | 12.68% | COVID Rebound, stimulus |

December 1991 | 11.16% | Post-recession recovery |

October 2011 | 10.77% | Eurozone debt crisis resolution optimism |

November 2020 | 10.75% | COVID Vaccine Breakthroughs |

April 2026 | 10.42% | Iran peace talks |

Source: Amsflow

The rally was driven primarily by the tech sector. The State Street Technology Select Sector SPDR Fund (XLK), tracking the tech stocks within the S&P500, returned 20% in April, and since the S&P500 is a market-cap-weighted index, the tech sector, having over 30% weight, is the single most important contributor to this magnificent performance of the broad equity market.

After such a rally, many investors start to face the dilemma of what to do next, and honestly, there are three possible options: 1) Hold; 2) Sell and time the market; and 3) Hedge or diversify.

Option 1: Keep on Holding a Tech-Heavy Portfolio

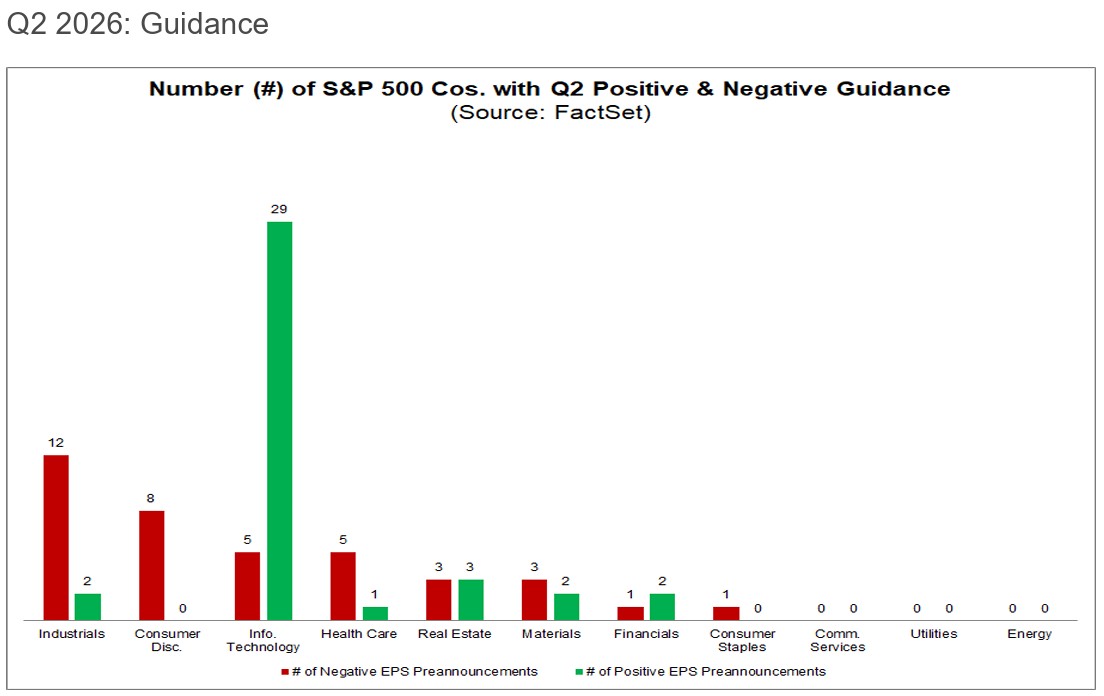

Most of the tech earnings have been positive so far, with the momentum to continue in Q2. It is not just Q1 results being good, but the guidance for Q2 has also been upbeat. A large majority of the tech companies (as of May 8th) have reported positive EPS guidance for Q2.

Source: FactSet

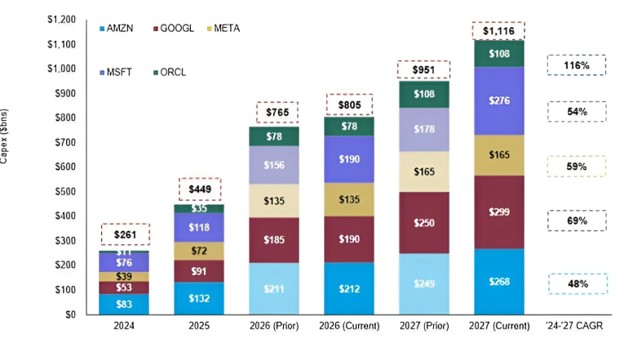

One of the core reasons behind the overall optimism is the capex from the hyperscalers is going up, providing liquidity for the AI rally. Furthermore, the demand for CPUs, GPUs, memory chips and optics outstrip the supply by a large margin, and immediate solution for this will not simply appear overnight. All this data supports the thesis that the rally actually has legs, at least in the months to come.

Source: Morgan Stanley

However, it appears that all positive aspects have largely been priced in. Expecting this level of exponential growth to continue is unrealistic. At some point there will be a plateau or just correction, or simply rotating funds to non-tech stocks. Not to mention there are still a lot of uncertainties and risks like geopolitics, inflation, mid-term elections.

Option 2: Selling and Trying to Enter at a Better Time

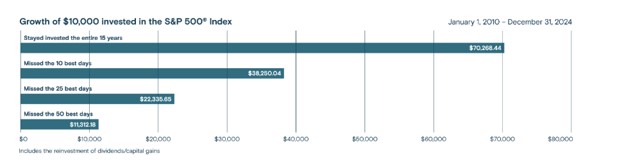

At this point, many would consider taking away some profits avoiding future turbulence and try to enter at a more favorable price. However, timing the market is always tricky, and it’s more about luck than skill, and it can be too much stress, guessing the short-term price movements. Even professional investors have spoken against timing the market. Peter Lynch has said far more money has been lost by Investors preparing for corrections than has been lost in corrections themselves. And according to Ray Dalio, trying to time the market is a fool's errand.

Historical data shows that being temporarily out of the market and missing the best days can greatly harm returns:

Source: S&P

Option 3: Diversifying Towards Less Correlated Sectors

Hedging and diversification can provide a good balance – stay invested in tech but without the big exposure to the risks. In the era of AI investing, a lot of different sectors remain overlooked, and healthcare is one of them.

Relatively Low Correlation with Tech

Apart from the macro effects (interest rates, inflation), these two sectors are driven by very different factors. Tech is driven by AI trends, data center capex, while healthcare is driven by demographics, regulations and biotech/pharma pipelines when it comes to launching products.

Drugmakers like LLY and NVO need to pass very strict FDA procedures to be able to sell a drug, and the FDA approval process and outcome have little to do with the overall market and the state of the economy. A lot of industries within the healthcare sector are insulated from economic downturns – pharmaceuticals, managed care providers, and medical equipment.

Low Valuations

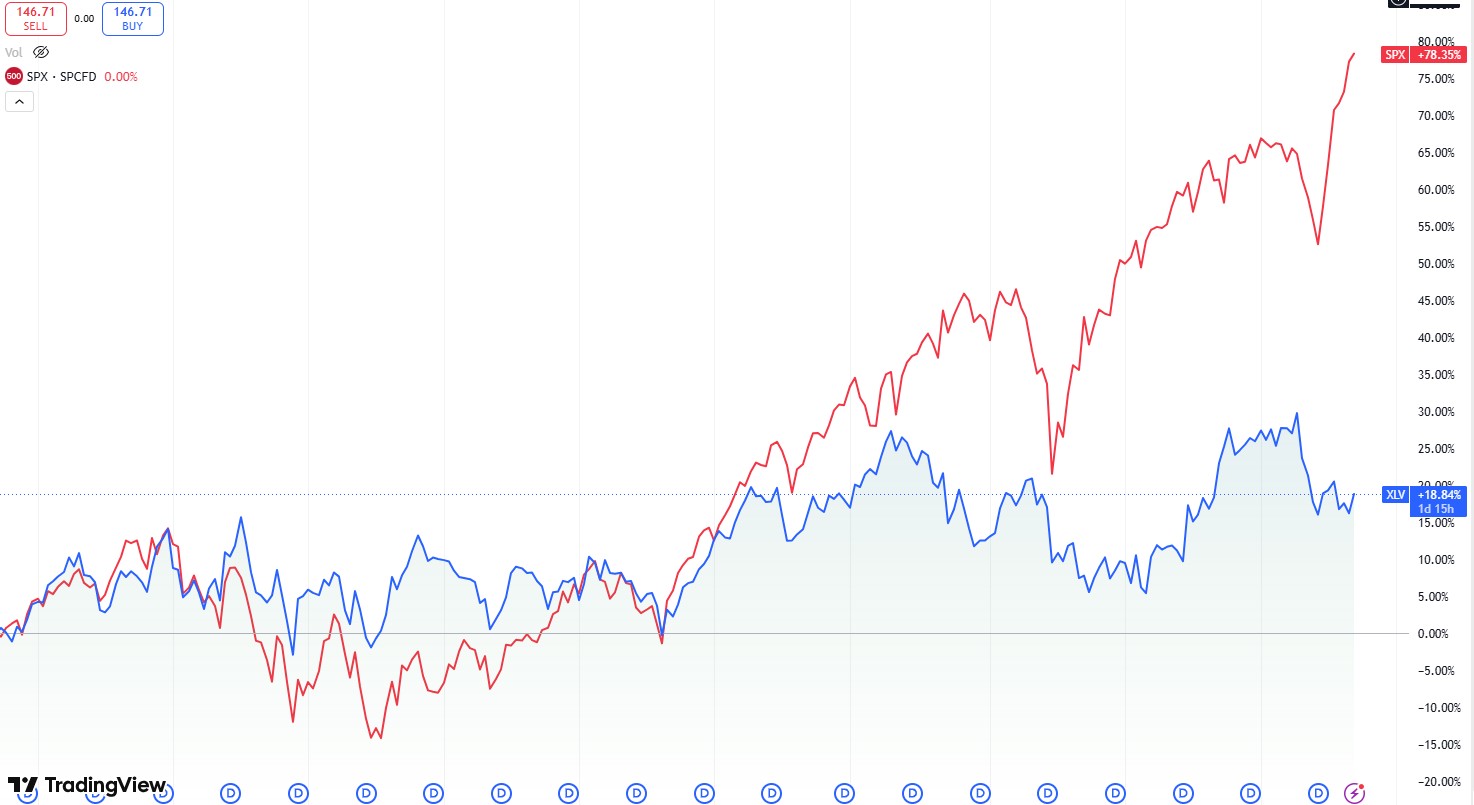

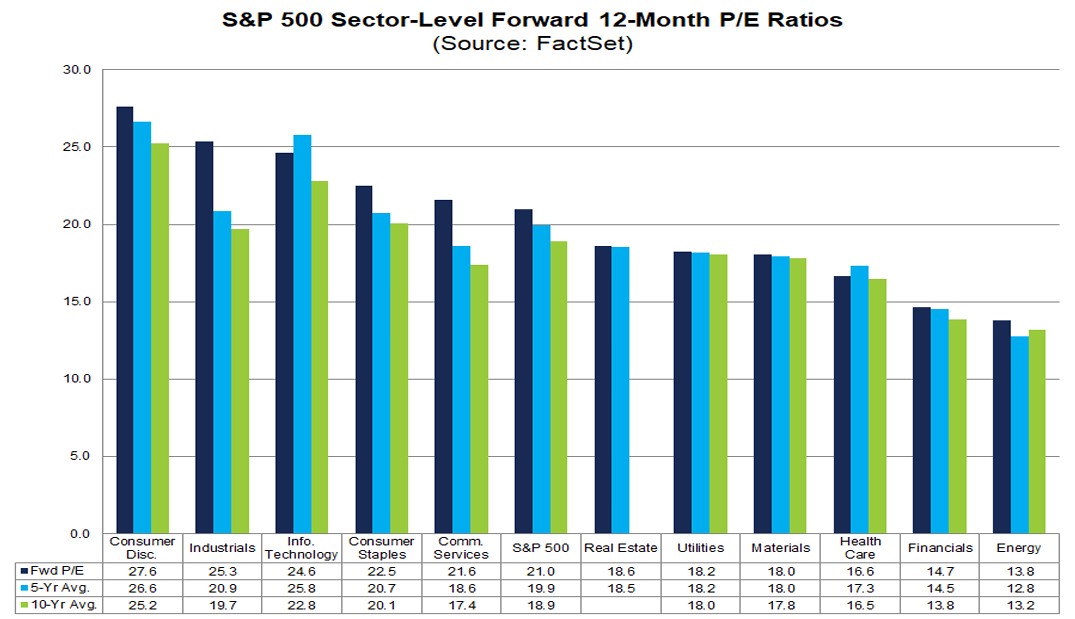

Years of underperformance make the healthcare sector a good value play. Healthcare is among the worst-performing sectors since 2021, significantly trailing behind the SPX index. Even among other sectors, the P/E ratio is on the lower side.

Source: TradingView

Source: FactSet

Just like how tech now is all about AI, GLP-1 is the hottest trend within healthcare. To explain it simply, unlike the traditional drugs, which can be considered as chemicals forcing the body to do something, GLP-1 drugs act like a bio-identical hormone engineered to achieve the desired goal. GLP-1 drugs so far are related to weight loss and diabetes, but their applicability can extend to many other pathologies.

GLP-1 drugs generally produce an average weight loss of 15–20% or more of body weight over 12–16 months, whereas older, traditional medications often result in more modest reductions, generally in the range of 5-10%, showing how effective and revolutionary GLP-1 could be.

Source: JP Morgan

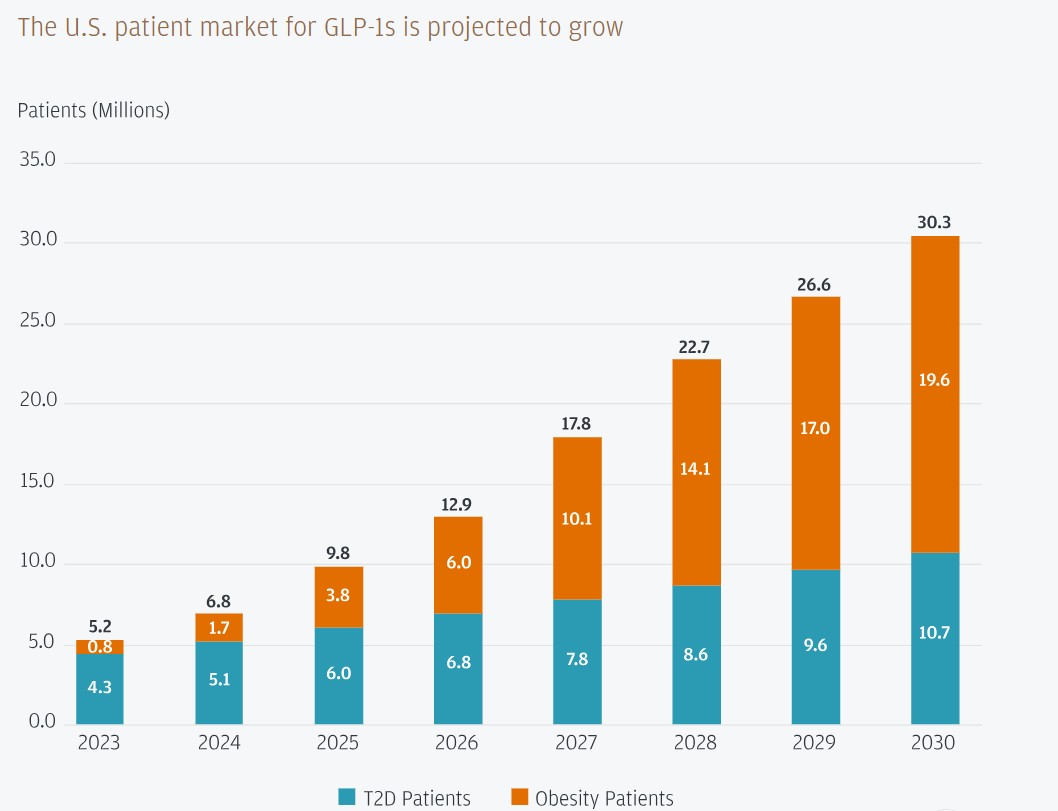

Currently there are 10mn patients in the US using GLP-1 for both Type2 diabetes and Obesity, this number is expected to reach 30mn within five years, according to IQVIA and JP Morgan, predisposing the whole market for a hypergrowth; The main drivers will be more accessible insurance coverage, as well as expansion of products towards oral forms (from injections), overseas market expansion and expansion of products beyond obesity and diabetes.

But many people may ask, why is the time to look at healthcare after years of underperformance, and why give up the AI winners for healthcare stocks? The healthcare industry is at a crossroads, and there are two main obstacles that have prevented the industry from progressing until now.

Obstacle 1 was Covid-19. The pandemic gave a boost to the sector a few years ago, but it also inflicted significant damage to the supply chains in the industry, especially when it comes to raw materials and logistics. In other words, COVID accelerated vaccine/biotech investment but diverted capacity from non‑COVID drugs; However, now this headwind is slowly fading away, and more resources are freed for non-COVID drugs.

Obstacle 2 is the regulatory uncertainty. GLP-1 is relatively new, and they are not very widely covered by the national and private healthcare plans, which makes GLP-1 quite expensive. There are plans for the U.S. Health and Human Services (HHS) (basically, the US ministry of health) to enforce a price cap for GLP-1 drugs so they can become more affordable for the public. The subsidy will be borne by the drugmakers, the private insurers and the government.

What investors are worried about is that this can dramatically cut the margins of drugmakers. Some sources say that drugmakers may need to cut the price of their products by up to 20%. What the market is missing is that the drugmaker's business model will evolve from low-volume, high-margin towards high-volume, low-margin, unlocking a much larger addressable market and bringing a much stronger predictability of the revenues, once patients are onboarded on the subsidized health programs. Also, GLP-1 drugs have very high gross margins, with Mounjaro being nearly 80%, and a price cut may still leave a solid margin. With more affordable drugs, the high drop rates of GLP-1 usage will go down, and drugmakers will enjoy much more predictable revenue streams.

How to Play This

Broad exposure to the sector can be achieved with the State Street Health Care Select Sector SPDR ETF (XLV). The other way is through individual stocks.

This is not an industry primer, so we cannot go that deep, but we can map some significant healthcare stocks. Firstly, we have the main GLP-1 players Eli Lilly and Company (LLY), a GLP-1 leader with blockbuster products like Mounjaro and Zepbound, as well as Novo Nordisk (NVO), the other major GLP-1 producer with products like Ozempic and Wegovy.

There are smaller contenders like Pfizer Inc. (PFE) and Amgen (AMGN), currently developing GLP-1 products, and willing to challenge the above two.

Other major healthcare players, not directly related to GLP-1, include, but are not limited to, UnitedHealth Group (UNH) - the largest managed healthcare and insurance provider; Johnson & Johnson (JNJ), a conglomerate with business spreading from pharma to devices; and AbbVie (biotech/immunology).

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.