Arm Earnings Meet Targets Again, Why Is Capital Unimpressed? Post-Market Shares Fall Over 6% After Initial Rise

AI Podcast

Arm's Q4 FY2026 results exceeded expectations, with revenue up 20.2% YoY, driven by strong licensing growth. While AI data center demand is robust, with over $2 billion in customer demand for its AGI CPUs, market concerns persist regarding supply chain execution. Royalty revenue faced headwinds from the weak smartphone market. Despite a slight decrease in operating margin due to increased R&D, Arm's pivot to AI data centers positions it for future growth, though near-term stock volatility reflects these supply chain uncertainties.

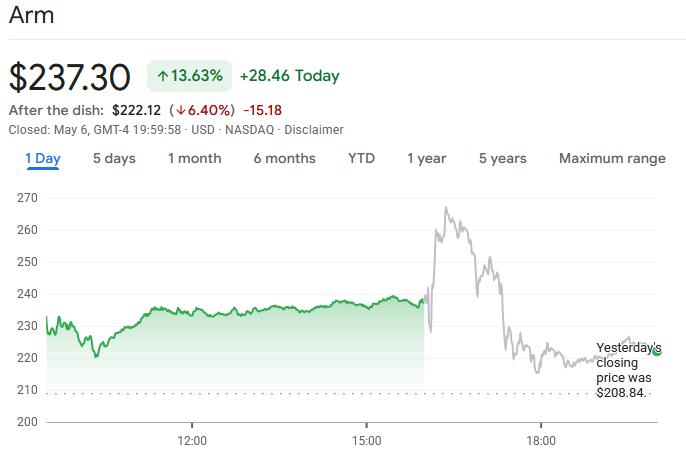

TradingKey - After the U.S. market close on May 6, Arm ( ARM) announced its fourth-quarter results for fiscal 2026, with both revenue and profit exceeding market expectations. Its AI data center business demonstrated strong growth momentum, but the sharp volatility in the stock price—rising initially and then falling after the release—underscored market concerns about the company.

Financial reports show that Arm's fourth-quarter revenue reached $1.49 billion, up 20.2% year-on-year, while full-year revenue hit a record high of $4.92 billion. This marks the third consecutive fiscal year since the company's IPO that revenue growth has exceeded 20%.

Profit performance was equally strong, with adjusted earnings per share of $0.60, beating the analyst consensus of $0.58. Full-year adjusted EPS reached $1.77, and the fourth-quarter adjusted operating margin was approximately 49%. However, compared to the 53% margin in the same period last year, profitability has come under some pressure, primarily due to increased investment in R&D and in-house chip development.

Meanwhile, despite short-term headwinds in the global smartphone market, licensing revenue also set a record of $819 million.

Notably, Arm's long-term growth narrative is pivoting from the mobile market to AI data centers. The company revealed that customer demand for its first data center CPU has exceeded $2 billion and is expected to persist through fiscal 2028, with the segment poised to become its largest business unit soon.

However, the market remains skeptical of Arm's supply chain capabilities. Michael Ashley Schulman, a partner at wealth management firm Cerity Partners, noted that investors are concerned about whether Arm can meet customer demand in a timely fashion. Although supply may eventually be secured, uncertainty persists regarding the speed of delivery and the company's ability to respond to further growth in future demand.

This cautious outlook, combined with short-term pressure on the mobile segment—where fourth-quarter royalty revenue of $671 million missed market expectations—triggered a reversal in market sentiment.

Following the earnings announcement, Arm's shares initially jumped 12% in after-hours trading before quickly diving to end the session 6.4% lower.

Arm’s Licensing Revenue Beats Expectations; Weak Smartphone Market Drags on Royalties

Arm's revenue primarily relies on two models: licensing chip technology to companies such as Apple and NVIDIA, and collecting royalties based on the shipment volume of products using its architecture. Its chip architecture has gained market recognition for its low power consumption, a feature that perfectly meets the current core demand for data centers to control energy costs.

Arm's licensing revenue delivered a stellar performance this fiscal quarter, recording $819 million in the fourth quarter—a 29% year-over-year increase that far exceeded market analysts' prior estimates of $781 million.

CFO Jason Child stated that this growth was mainly driven by robust market demand for next-generation chip architecture and the results of deepening strategic cooperation with customers, including a long-term partnership with the Indonesian government and two new licensing agreements for next-generation Computing Subsystems (CSS). Notably, a technology licensing and design services agreement under SoftBank contributed $200 million in licensing revenue to the quarter.

As a highly forward-looking indicator in Arm's business model, changes in licensing revenue often signal the industry's future direction—customers purchasing Arm architecture and IP licenses typically intend to launch Arm-based chip products within the next few years, which will provide Arm with consistent and stable royalty revenue. Therefore, the significant growth in the licensing business directly reflects that leading customers are continuing to ramp up their investment in the Arm ecosystem.

However, Arm also cautioned that licensing revenue is subject to quarterly volatility, as its performance is directly linked to the timing of large deal signings; the company instead focuses more on Annualized Contract Value (ACV). Data shows that Arm's ACV grew 22% year-over-year in the fourth fiscal quarter, remaining above the company's long-term growth targets.

In contrast to the strong performance of the licensing business, Arm's royalty revenue for the fourth fiscal quarter was $671 million, up 11% year-over-year but below the market expectation of $690 million to $693 million.

Royalty revenue is directly linked to the actual shipment volume of end-user devices; therefore, this lower-than-expected figure typically implies a slowdown in shipment momentum in certain end markets.

Currently, the primary drag comes from the smartphone market. Arm revealed that smartphone shipments turned to negative year-over-year growth last quarter, with weakness concentrated in the low-end market, while memory chip shortages drove up consumer electronics prices and dampened sales, further intensifying this pressure.

As the dominant leader in global smartphone chip architecture, Arm's designs power nearly all of the world's smartphones; consequently, cyclical fluctuations in the mobile market continue to have a direct impact on the company's short-term revenue, following similar warnings previously issued by downstream chipmakers like Qualcomm.

Against the backdrop of short-term pressure in the global smartphone market, it is particularly noteworthy that Arm's licensing and other revenue achieved a 29% counter-trend growth. Although mobile royalty revenue growth slowed due to supply chain fluctuations, many customers opted to prepay licensing fees to secure rights to advanced chip designs. This "licensing-first, royalties-later" business model has established a robust performance buffer for Arm, effectively offsetting the impact of the consumer electronics market's weakness.

AI Agents Reshaping the CPU Market

With the explosive growth of AI agents, demand for general-purpose computing power has surged, and Arm has entered the burgeoning central processing unit (CPU) market.

Previously, Arm dominated the mobile device market, including smartphones and tablets, with its low-power architecture; however, in the server and PC sectors, Intel and AMD's x86 architecture has consistently maintained dominance.

With the advent of the AI era, the importance of energy efficiency, core scale, data throughput, and customization capabilities has risen sharply, and the advantages of the Arm architecture have begun to stand out in the data center sector—particularly the increasing power consumption and heat dissipation pressures in AI scenarios, which have become the core competitive edge of Arm's high-efficiency CPUs.

The Arm AGI CPU, released this March, was specifically designed for AI agents (AI software capable of executing tasks autonomously) and received high market recognition immediately upon its launch.

Currently, major global cloud providers have fully deployed Arm-architecture products; Amazon ( AMZN) AWS continues to expand its Graviton series and is deeply integrating it with infrastructure such as Trainium and Nitro; Google ( GOOGL) launched the Axion CPU to build a complete AI computing ecosystem alongside its TPUs; Microsoft ( MSFT) Azure is advancing its self-developed Arm-architecture CPU, Cobalt; NVIDIA ( NVDA )'s Grace/Vera and other AI server products also extensively utilize Arm-architecture CPUs.

According to Arm's disclosures, total customer demand for AGI CPUs in fiscal years 2027 to 2028 has exceeded $2 billion; the product is expected to deliver more than twice the performance of x86 platforms at the rack level and could help AI data centers reduce capital expenditure by up to $10 billion per gigawatt.

CEO Rene Haas expressed even greater confidence, stating that Arm has the capacity to capture the largest share of the CPU market by the end of this decade.

However, he also admitted that while Arm has secured enough capacity to meet the first $1 billion in order demand, it has yet to fully lock in capacity for the second $1 billion. Revenue from the first batch of AGI CPUs is expected to be recognized in the fourth quarter of fiscal 2027, totaling approximately $90 million, with the company planning to provide more specific shipping estimates in the third quarter.

The popularization of AI agents is redefining the value of CPUs in the AI industry chain; while GPUs were previously the absolute core of AI computing, the role of CPUs in task scheduling, memory access, and network coordination is now becoming increasingly critical.

UBS ( UBS) analyst Tim Arcuri estimates that the total addressable market for server CPUs will reach approximately $170 billion by 2030, with the share of CPUs in AI chips potentially growing fivefold; the ratio of CPUs to GPUs in inference scenarios is gradually balancing out, and new demand for standalone pure-CPU server racks may even emerge, which is expected to be split equally between x86 and Arm architectures.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.