Is Netflix Still Worth Buying After a 10% Stock Slump? Who Is the Better Investment Compared to Disney?

AI Podcast

Netflix shares dropped nearly 10% despite beating Q1 revenue and EPS expectations, largely due to a $2.8 billion one-time fee, not core business growth. Weak Q2 guidance and unchanged full-year outlook fueled the sell-off. Co-founder Reed Hastings' departure added symbolic weight. While some analysts view the decline as an overreaction, cost pressures, unproven price hike benefits, and subscriber growth concerns persist. Disney, conversely, shows streaming profitability and robust cash flow from its Experiences segment, presenting a more stable investment profile with a lower valuation.

TradingKey - After the market close on April 16, streaming giant Netflix delivered a seemingly stellar Q1 scorecard: revenue rose 16% year-over-year to $12.25 billion, beating market expectations of $12.17 billion; earnings per share reached $1.23, nearly doubling from $0.66 in the prior-year period.

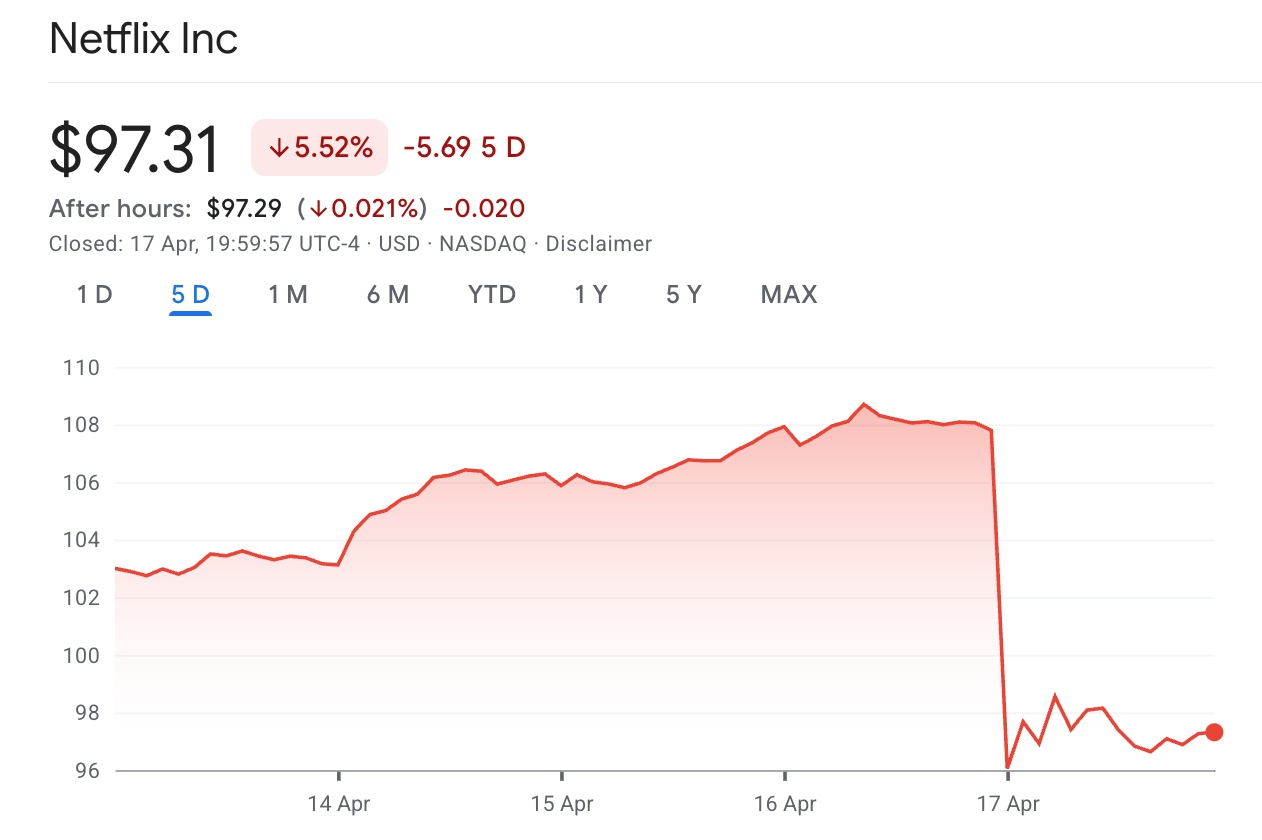

[Netflix shares plunged nearly 10%, Source: Google Finance]

However, the stock plummeted following the earnings release, with intraday losses exceeding 11% at one point on April 17 before closing down approximately 10% at $96.49, marking its largest single-day drop in nearly a year.

Why did a report that 'beat expectations' instead become the trigger for a sell-off?

Both Guidance Figures Missed Expectations

The primary reason Netflix's first-quarter earnings per share significantly exceeded expectations was not an improvement in its core streaming business, but rather a $2.8 billion one-time breakup fee.

This massive windfall stemmed from Netflix ending its bid for Warner Bros. Discovery assets, which were instead acquired by Paramount Skydance. Under the agreement, Netflix received approximately $2.8 billion in termination fees, recorded under "interest and other income," which alone accounted for the vast majority of the quarter's profit growth.

Market consensus on this was uniform: one-time non-recurring gains are essentially "paper profits." While they burnished past financial statements, they do nothing to help forecast the future. When analysts stripped away this windfall to re-examine performance, the underlying fundamentals of Q1 were far less glamorous than they appeared on the surface.

More disappointing for investors was that, after excluding this one-time income, Netflix failed to raise its full-year guidance for fiscal 2026; revenue guidance remained in the $50.7 billion to $51.7 billion range, with the operating margin target still at 31.5%. Against the backdrop of the Q1 beat, this failure to raise the outlook was interpreted by the market as a cautious signal from management regarding future costs and the competitive landscape.

Simultaneously, co-founder and Chairman Reed Hastings announced he will step down from the board after his term expires in June, concluding his 29-year leadership. As the central architect of Netflix's culture and strategy, the symbolic weight of Hastings' departure was amplified by the market at this sensitive juncture. Although Co-CEO Ted Sarandos denied the decision was related to the failed acquisition, concerns over strategic continuity continue to mount.

Weak Q2 guidance was the primary driver of the plunge; Netflix expects Q2 revenue of approximately $12.57 billion and earnings per share of just $0.78, both missing Wall Street estimates of $12.64 billion and $0.84, respectively. The company admitted that the second quarter will see the highest year-over-year increase in content amortization costs for the year—the spending peak has arrived while the benefits of price hikes have yet to materialize, leaving the shadow of rising costs to loom large.

Will Netflix Continue to Fall?

From a fundamental perspective, Netflix is facing three intensifying structural pressures.

Netflix plans to increase its 2026 content budget by approximately 10% to nearly $20 billion, while its acquisition of AI firm InterPositive and roughly $275 million in acquisition-related costs from the Warner transaction are further squeezing profit margins. Although the company maintained its full-year operating margin target of 31.5%, there is widespread skepticism in the market regarding its ability to achieve this figure.

Furthermore, the potential dampening effect of price hikes on subscriber growth has yet to be verified. In March, Netflix raised the price of its U.S. standard ad-free tier by $2 to $20 per month. While price increases benefit ARPU in the short term, the competitive landscape in streaming continues to intensify—with rivals like Disney+, Amazon Prime Video, and HBO Max closing in—and the risk of subscriber churn cannot be ignored. According to a Bank of America report, Q1 net subscriber additions were approximately 6 million, slightly below the market expectation of 6.5 million, bringing the total number of paid members to approximately 331 million.

Simultaneously, Netflix's stock had just experienced a rally prior to the earnings release, with expectations priced to perfection and an extremely narrow margin for error. The slowdown in second-quarter guidance, combined with the lack of an upward revision to full-year guidance, directly shattered the market's previous optimistic pricing.

However, Wall Street sell-side analysts generally believe this decline is an "overreaction" rather than a deterioration of fundamentals.

Morgan Stanley analyst Sean Diffley explained that the lower Q2 guidance is primarily due to the lag effect of domestic U.S. price hikes—such adjustments typically take two to three months to be fully reflected in financial data—and the full-year 31.5% margin target remains firm.

Needham analyst Laura Martin maintained a "Buy" rating and a $120 price target, noting that Netflix's internal core metrics for measuring user engagement recently hit record highs. JPMorgan also suggested capitalizing on the pullback, stating that Netflix's execution remains excellent and its growth potential is vast.

Overall, Netflix's mid-to-long-term investment thesis has not been derailed by this earnings report. A paid subscriber base exceeding 325 million, expectations for a doubling of its advertising business, and penetration potential within a global TV viewership share of only about 5% remain the core pillars supporting its long-term valuation.

In the short term, however, cost-side pressures have yet to be fully absorbed, the effects of price hikes require time to be validated, and the psychological impact of Hastings' departure will need to be gradually processed by the market.

Has Disney Replaced Netflix as the Better Investment?

On the streaming front, Disney (DIS) has made substantial progress. By the end of fiscal year 2025, Disney+ and Hulu had a combined subscriber base of approximately 196 million. The streaming business generated $1.3 billion in operating profit last year and further produced $450 million in Q1 of fiscal year 2026.

Disney is transitioning from a "cash-burning" phase to a "profitability" phase in streaming, and the market's assessment of its core drivers is undergoing a re-evaluation. The consensus earnings for fiscal year 2026 are $6.61 per share, an 11.5% year-over-year increase.

At the same time, Disney's Experiences segment continues to provide stable cash flow for the company. In Q1 of fiscal year 2026 alone, theme parks, cruises, and consumer products contributed $3.3 billion in operating profit, accounting for 72% of the company's total operating profit. This is a robust and predictable cash flow machine.

The valuation logic for the two companies is starkly different. Looking at their P/E ratios, Netflix's 38x P/E reveals its pure streaming pricing power, betting on its advertising monetization capabilities and room for continued price hikes with its 325 million members. This corresponds to higher elasticity, but market expectations have been driven quite high, leaving little room for error.

In contrast, Disney's valuation stems more from a combination of recovery and valuation re-rating. The inflection point for streaming profit has been established, and the Experiences business provides secure cash flow. The current level of just 15x projected 2026 earnings highlights its high margin of safety, though streaming profit margins are still far below those of Netflix.

Needham analyst Laura Martin previously noted when comparing the two companies that Netflix's dominance and pricing power in the streaming sector remain its core moat, while Disney relies more on its IP portfolio and bundling strategies to drive growth.

For investors seeking high upside potential, Netflix's risk-reward ratio has significantly improved after its plunge, with the price level around $92 providing an attractive margin of safety.

For investors who prefer valuation re-ratings and value robust cash flow support, Disney's current forward P/E of under 15x holds allocation value, though they must accept the potential for periodic volatility as its streaming business undergoes its catch-up process.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.