Gold Prices Narrowly Hold $4,000 Mark; When Will the Precious Metals Sell-Off Stop?

Spot gold declined significantly, breaching $4,100 and nearing $4,000, driven by shifting Federal Reserve rate hike expectations following stronger-than-expected May jobs data and higher CPI inflation. Citigroup warned of extreme short-term risks, citing the need for substantial physical gold purchases to sustain current prices. Global gold ETFs experienced net outflows, though central bank demand, particularly from emerging markets and China, provides underlying support. Technically, gold has broken key moving averages, with potential downside targets at $4,000 and $3,888. The sell-off's end hinges on tempered rate hike expectations, exhausted short-term selling pressure, and sustained central bank buying.

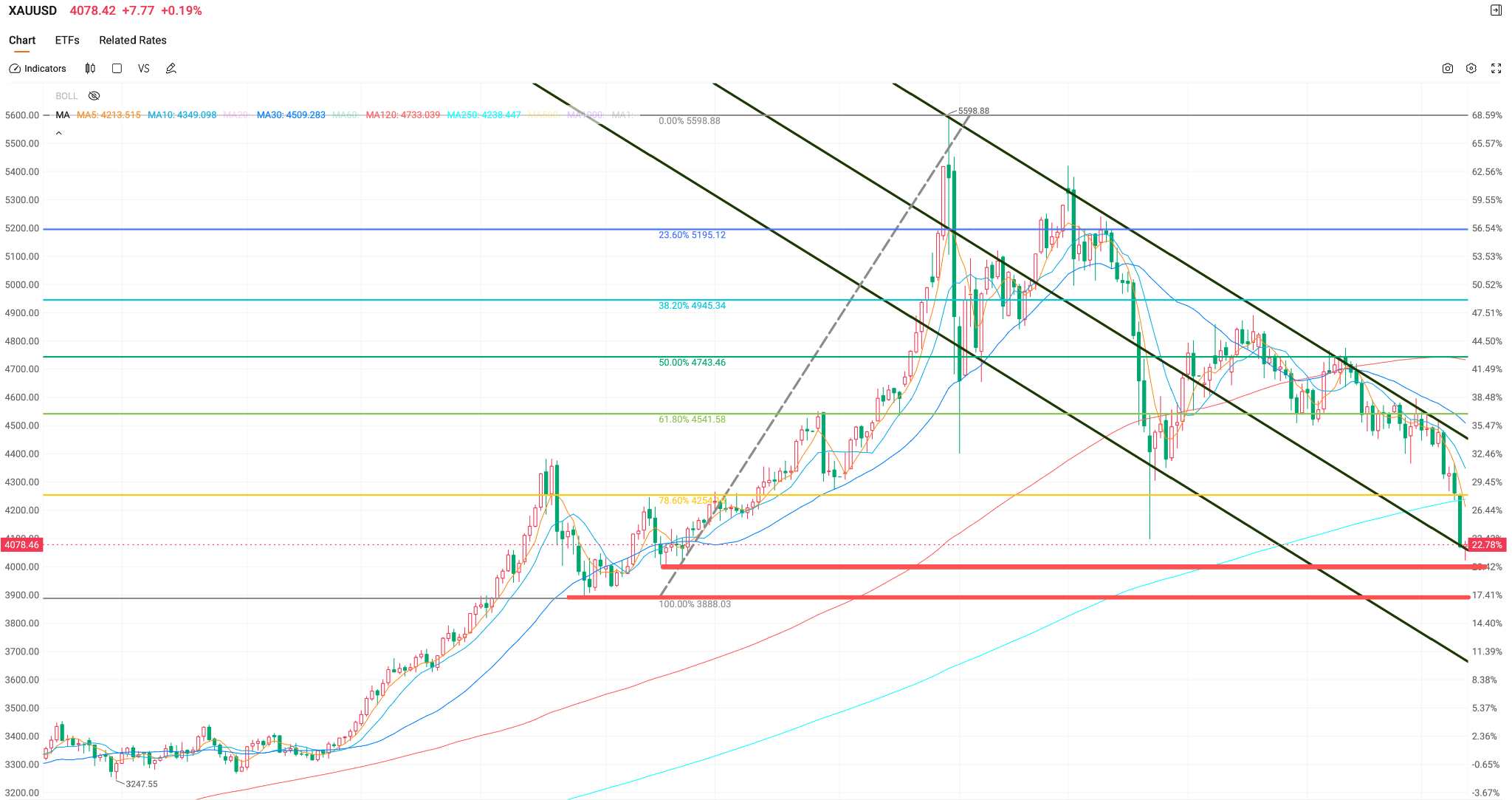

TradingKey - On June 10, Eastern Time, spot gold ( XAUUSD) breached the $4,100 level during intraday trading after four consecutive sessions of selling, nearing the $4,000 psychological support level. This downturn marks the most severe retracement since 2023.

Since late May, gold prices have fallen by nearly 10%, completely erasing year-to-date gains; the price has retraced more than 22% from its all-time high of $5,598.75.

Where the sell-off eventually stops depends on the balance of three factors: when the market scales back Fed rate hike expectations, when short-term selling pressure clears, and whether gold demand from global central banks can offset capital outflows.

Rate hike expectations are the primary drag.

The catalyst for the sell-off remains the shift in interest rate expectations.

May non-farm payrolls increased by 172,000, far exceeding market expectations and significantly weakening prospects for rate cuts this year. Meanwhile, data released Wednesday by the U.S. Bureau of Labor Statistics showed the Consumer Price Index (CPI) rose 4.2% year-on-year in May, its highest level since early 2023, marking the first time in three years that CPI inflation has breached the 4% threshold.

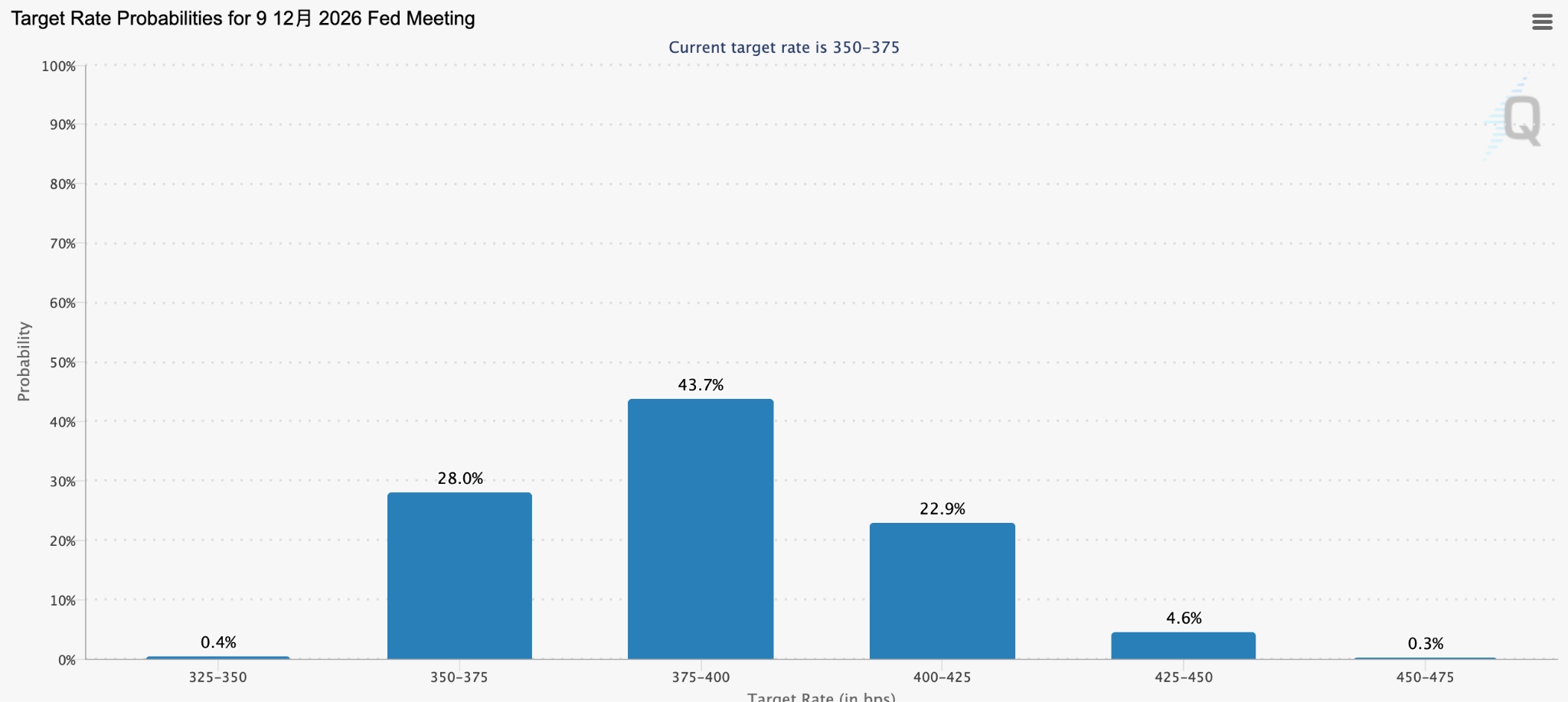

According to the CME FedWatch Tool, the probability of a Federal Reserve rate hike in October has risen to around 42%, while the probability of a hike in December has surpassed 70%.

[Probability of a Federal Reserve rate cut in December, Source: CME FedWatch]

The inverse pricing relationship between gold prices and real interest rates has been particularly significant since late April, with the calibration of liquidity expectations becoming the dominant driver of market pricing rather than the geopolitical risk premium.

Citigroup’s commodities team on June 9 sharply lowered its three-month gold price target from $4,300 per ounce to $4,000, explicitly warning short-term investors that the risks would be "extremely high" without wide stop-loss levels.

Citi's calculation logic is quite straightforward: to maintain current gold price levels, physical gold purchases would need to keep a pace of approximately $900 billion annually, whereas normal purchase volumes between 2010 and 2024 ranged only from $250 billion to $400 billion per year. In short, the current dependence of gold prices on physical demand has far exceeded historical norms.

Short-term Sell-off and Long-term Support

In terms of capital flows, global investors are accelerating their exit from gold ETFs.

Data from the World Gold Council shows that global physical gold ETFs saw a net outflow of $2 billion in May, with total assets under management (AUM) falling 2% month-on-month to approximately $600 billion and overall holdings retreating to 4,121 tonnes, slightly below the record high of 4,176 tonnes set at the end of February.

However, the massive retreat of short-term speculative capital has not shaken the floor support provided by long-term allocation funds.

As of the end of May 2026, China's gold reserves reached 74.96 million ounces, an increase of 320,000 ounces month-on-month, marking 19 consecutive months of accumulation and making the central bank the most steadfast contrarian buyer during the market downturn. In the first quarter of 2026, net gold purchases by global central banks reached 244 tonnes, a 17% increase quarter-on-quarter, as emerging market central banks continue to significantly increase their gold reserve allocations.

Key Support Following a Technical Break

From a technical perspective, spot gold broke below the $4,100 psychological level on June 10, hitting an intraday low of around $4,070. Gold prices have fallen below the 250-day moving average for the first time since September 2023.

Analysis indicates that gold's break below the key $4,100 support level has triggered stop-loss selling by programmatic trend traders. Analysts believe that, given the current market structure, a move toward the $4,000 psychological level cannot be ruled out. If the $4,000 threshold is breached, gold prices will face a test of the $3,888 level.

When will the sell-off end?

The three conditions for the sell-off to halt have not yet been fully satisfied. Regarding rate hike expectations, the probability of rates remaining unchanged in July and September is significantly higher than that of a hike; however, pricing for a rate hike within the year has not been fully digested, and the market continues its tug-of-war with the Fed over expectations.

Regarding short-term capital liquidation, the scale of net ETF outflows is still expanding. CFTC speculative net long positions have dropped nearly 40% from their peak at the start of the year, but it remains unclear whether the retreat is nearing its conclusion.

Technically, if gold prices stabilize within the $4,000 to $4,100 range and form an effective technical bottom divergence, the opportunity for a recovery in market sentiment will gradually emerge.

Taken together, until the Federal Reserve's policy meeting in mid-to-late June releases a clear signal, gold will likely repeatedly test its floor in the $4,000 to $4,300 range, pending a new equilibrium in the tug-of-war between market expectations and the Fed.

For long-term allocators, the decline in gold prices is gradually deflating the previous sentiment bubble. Repeated testing of the $4,000 threshold may eventually serve as a turning point where bulls and bears shift from liquidation to balance, at which time the market will address the core question of when the sell-off will end.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (3)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.