Nasdaq Index Rises for 10 Straight Days, Why Has Tesla Barely Risen?

AI Podcast

Tesla's stock has declined year-to-date, significantly underperforming the Nasdaq's rally, due to disappointing Q1 delivery volumes and production-delivery mismatches. The energy storage business also saw a year-over-year decline. Sell-side firms have issued more cautious stances, lowering ratings and price targets. Additionally, political endorsement shifts and Musk’s controversial statements have negatively impacted valuation and European sales. The market's focus on AI infrastructure excludes Tesla, with investors prioritizing fundamentals over sentiment and narratives. Significant progress on Robotaxi and Optimus, along with better-than-expected earnings guidance, will be crucial for investor interest.

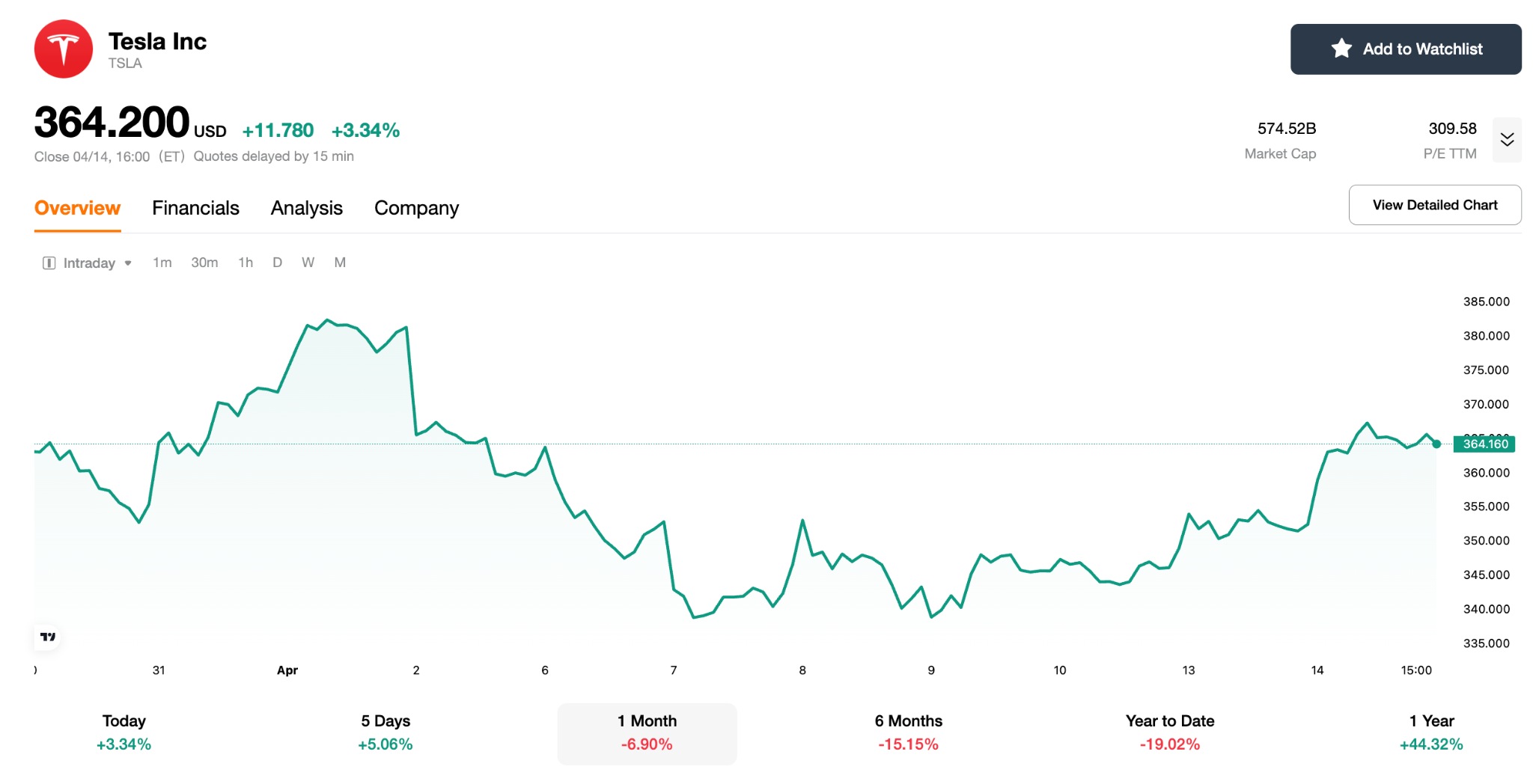

TradingKey - On April 14, the Nasdaq notched its tenth consecutive session of gains, marking its longest winning streak since 2023. It has risen nearly 14% from its recent lows, as the 'Magnificent Seven' tech giants generally outperformed the broader market.

However, Tesla shares rose by only nearly 2.5% over the ten-session period. Year-to-date, Tesla (TSLA) the stock has fallen approximately 21.5% cumulatively, retreating more than 30% from its December peak. As AI chip stocks stage a collective rally, why is Tesla being 'forgotten' by the market?

Delivery volumes across multiple business lines suffered a major setback.

Previously, Tesla's first-quarter results left Wall Street collectively disappointed.

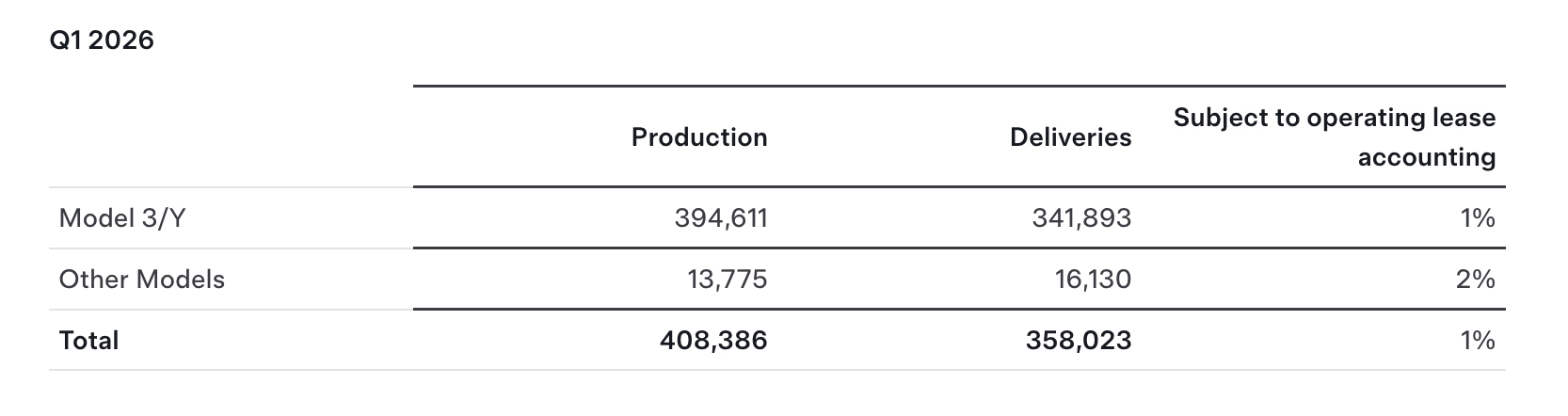

[Tesla Q1 Delivery Performance, Source: Tesla Investor Relations ]

In the first quarter of 2026, Tesla's global deliveries were only 358,023 units, which not only fell below the Bloomberg analyst consensus of 372,160 units but also marked the worst level in a year.

Furthermore, production reached 408,386 units in the first quarter, resulting in a gap of over 50,000 units between production and deliveries—the most severe quarterly production-delivery mismatch in Tesla's history.

Performance in the energy storage business was equally disappointing. Q1 energy storage deployment was only 8.8 GWh, a 15% year-over-year decline and a miss of over 40% compared to JPMorgan's forecast of 15.1 GWh. This marks the first year-over-year decline for the energy storage business since Q2 2022, signaling a temporary stall in the "second growth engine" that the market had previously pinned high hopes on.

Following the release of delivery data, sell-side firms Goldman Sachs, HSBC, and UBS almost simultaneously pivoted to more cautious stances, lowering ratings or price targets. JPMorgan was the most aggressive, slashing its Q1 2026 earnings per share estimate from $0.43 to $0.30 and full-year EPS from $2.00 to $1.80 while maintaining a $145 price target, suggesting more than 50% downside from the current share price.

Loss of political endorsement premium: "Turning against" Trump hammers Tesla's valuation.

Between 2025 and 2026, political disagreements and Elon Musk’s public declaration regarding the formation of a new political party directly intensified his conflict with Donald Trump, who subsequently attacked Musk for continuing to profit from government subsidies.

The electric vehicle subsidy policy officially ended on September 30, 2025, a move orchestrated by the Trump team to dismantle the Biden administration's green energy subsidies. Although Musk had previously indicated the decision would favor a return to healthy competition in the automotive industry and claimed to support it, the impact of this policy shift was fundamentally structural for an automaker that relied heavily on subsidies to drive sales in the North American market.

Although media reports later suggested a thawing of relations between Trump and Musk, the premium from his political endorsement remained insufficient to sustain the company's high valuation.

Furthermore, Musk’s public support for Germany’s AfD in early 2025 caused Tesla’s sales in Europe to plummet. Throughout 2025, Tesla’s new vehicle registrations in Europe reached 238,700 units, a 26.9% year-on-year drop, with an even steeper decline across the European Union; research indicated that 60% of potential European buyers opted against purchasing a Tesla due to Musk’s political stance.

This political alignment has dealt a lasting blow to the Tesla brand; even a year later, the rhetoric from such posturing continues to cause irreparable damage to the company.

Falling behind in the AI boom, the market is no longer buying the Tesla narrative.

The core driver of the Nasdaq's 10-day winning streak is a broad recovery in risk appetite amid expectations for the resumption of U.S.-Iran peace talks, with capital pouring into sectors like AI chips, optical communications, and semiconductors.

However, Tesla falls precisely outside this narrative framework. When investors discuss "AI infrastructure," they think of NVIDIA’s GPUs, Broadcom’s custom chips, and TSMC’s foundry capacity, rather than Tesla’s FSD or Dojo supercomputer.

UBS analyst Joseph Spak also pointed out when upgrading Tesla to "Neutral" on April 14 that the stock trades more on sentiment, narratives, and trends than on fundamentals; recent market concerns regarding soft EV demand, energy business shortfalls, and slow progress on Robotaxi and Optimus have exerted sustained pressure on the share price.

Notably, UBS expects Tesla to produce only about 5,000 Optimus robots by 2027 and just 30,000 by 2030—far below Musk's publicly stated goal of 1 million units annually—meaning the valuation premium for "humanoid robots" will increasingly lose market favor.

What Should Tesla Investors Watch?

Tesla is currently facing severe fundamental challenges, as both electric vehicle delivery and energy storage data fell short of expectations, while the removal of policy subsidies is eroding the demand foundation in its core markets.

Even as Cathie Wood spent nearly $28 million last week "buying the dip" , it failed to reverse the slump in Tesla's stock price.

The Nasdaq's ten-day winning streak is essentially a concentrated market repricing driven by the AI narrative and expectations of easing geopolitical risks. Tesla being "forgotten" in this rally demonstrates that as the market shifts from "concept" back to "performance," no company can remain independently priced while being detached from its fundamentals for long.

Tesla will release its full first-quarter 2026 earnings report after the bell on April 23. Whether it can provide better-than-expected earnings guidance or substantive progress on Robotaxi will determine if this former "trillion-dollar club" member can return to the radar of investors.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.