Pre-Market Surge of Over 15%. What Oracle’s 2.8GW Fuel Cell Order Brings to Bloom Energy?

AI Podcast

Bloom Energy announced a strategic partnership with Oracle for up to 2.8 GW of fuel cell systems to power Oracle's AI data centers, driving Bloom Energy shares up 15%. The deal highlights the urgent need for rapid, onsite power solutions as data center expansion faces grid limitations. While Bloom Energy shows strong revenue growth and a substantial backlog, its valuation is extremely high. Analyst ratings are mixed, with a consensus "Hold," and insider selling raises caution. Oracle's deepening ties, including warrants for Bloom Energy shares, suggest a structural dependency beyond a single order, with future expansion likely.

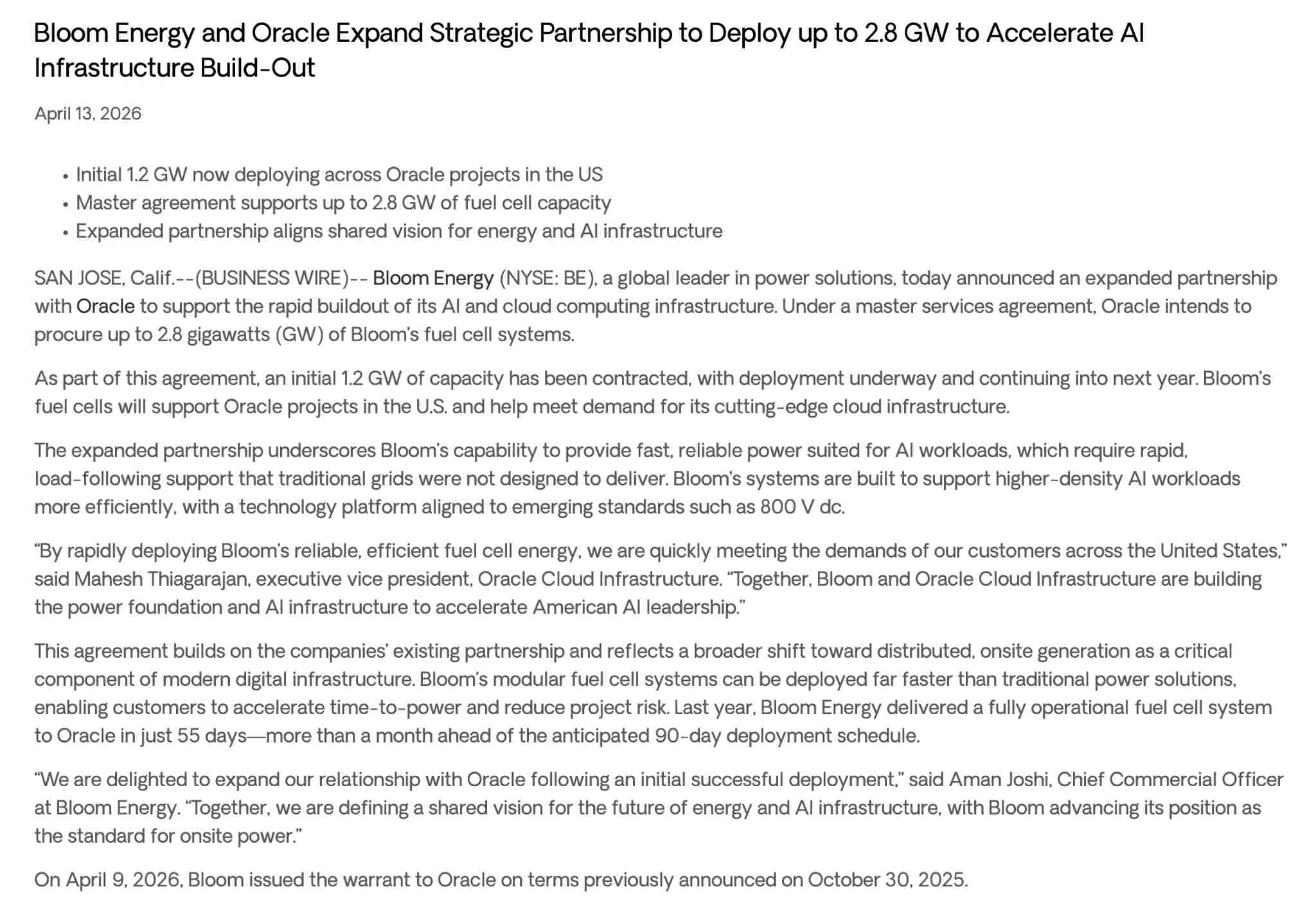

TradingKey - On April 13 local time, U.S. fuel cell company Bloom Energy (BE) announced it is working with Oracle to expand their strategic partnership, as Oracle plans to procure up to 2.8 gigawatts (GW) of fuel cell systems to support the massive power requirements of its artificial intelligence data centers.

[Bloom Energy shares surged 15% in pre-market trading; Source: Google Finance]

Driven by the news, Bloom Energy's pre-market shares surged over 15% to reach $203.90, not only breaking the record high of $180.90 set on Feb. 25 but also pushing its market capitalization above $50 billion.

Contracts for the first 1.2 GW of capacity have been signed for deployment this year and in 2027, with enough generation capacity to simultaneously power approximately 750,000 U.S. households.

What kind of company is Bloom Energy?

Bloom Energy, headquartered in San Jose, California, is a fuel cell technology company specializing in distributed power generation and hydrogen production. Its core technological path is modular solid oxide fuel cells (SOFC).

The essence of this technology is not an energy storage battery, but a solid-state energy conversion device: in a high-temperature environment of 600 to 1,000 degrees Celsius, fuel (natural gas or hydrogen) undergoes an electrochemical reaction with oxygen to directly output current without combustion or mechanical work. This design results in low carbon dioxide emissions, high power generation efficiency, and flexible fuel adaptability.

The company's core products include the Bloom Energy Server (a power generation platform) and the Bloom Electrolyzer. The former provides reliable, resilient onsite power solutions for data centers, utilities, and various commercial and industrial customers. To date, Bloom Energy has deployed over 1.2 gigawatts of Energy Servers across more than 1,200 locations in seven countries globally.

The primary reason SOFC is highly favored by tech giants like Oracle is its deployment speed. Traditional grid expansion requires an approval and construction cycle of 5 to 7 years, and gas turbine solutions take 2 to 3 years. In contrast, Bloom Energy's SOFC set a record last year by completing the installation and full commercial operation of a megawatt-scale power system for Oracle in just 55 days, significantly beating the 90-day expectation. In the urgent situation where AI data centers face downtime without power, this "plug-and-play" onsite generation model has become a necessity for tech giants.

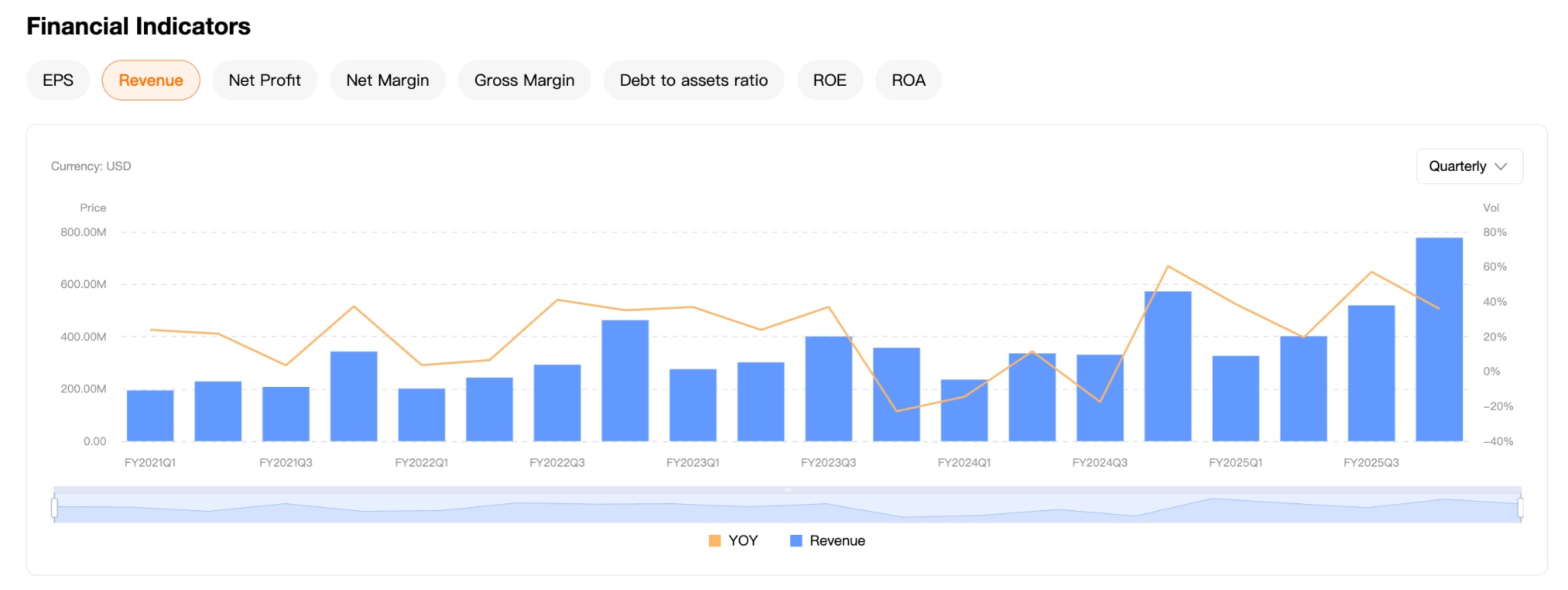

[Bloom Energy revenue shows quarterly growth; Source: TradingKey]

From a fundamental perspective, Bloom Energy is at an inflection point of accelerating performance. Fourth-quarter 2025 revenue reached $778 million, up 35.9% year-over-year; full-year revenue was $2.024 billion, up 37.3% year-over-year. Full-year non-GAAP operating profit reached $221 million, with full-year net operating cash inflow of $114 million, signaling a significant enhancement in earnings quality and self-sustainability.

The company's 2026 performance guidance indicates: expected year-over-year revenue growth of over 50%, non-GAAP gross margin of approximately 32%, and a doubling of free cash flow year-over-year. As of the end of 2025, the company's total backlog was approximately $20 billion, up 65% year-over-year, with product orders accounting for about $6 billion, up 140% year-over-year. Furthermore, 100% of all new product orders are tied to long-term service contracts, providing strong certainty for future performance realization.

Is Now the Right Time to Buy Bloom Energy?

Bloom Energy is currently in a sweet spot. The thirst for power in AI data centers has reached a point where "electricity has replaced chips as the number one bottleneck for expansion." The North American utility grid faces capacity shortages, with grid connection wait times for large data centers often stretching 5 to 7 years.

Bloom Energy's SOFC technology directly addresses this pain point. With its high energy conversion efficiency, rapid deployment, and low-carbon potential, SOFC is highly compatible with the power usage characteristics of data centers. Amid intensive data center construction in the U.S. and a simultaneous power gap, Bloom Energy, as a core industry leader, is expected to see future orders exceed expectations.

CEO KR Sridhar stated bluntly during an earnings call: "'Bring your own power' has become the motto for data centers and power-intensive factories."

From the perspective of customer diversification, the company's end customers from hyperscale and cloud-native data centers have grown from one a year ago to six. Notable clients such as Intel, CoreWeave, and American Electric Power have progressively adopted its SOFC technology. The order structure has also expanded from high-electricity-price regions to the entire U.S., with over 80% of the U.S. backlog now coming from low-price regions outside of California and the Northeast, proving the company's competitiveness across a broader cost spectrum.

However, significant risks that cannot be ignored also stand out.

First is the extremely high valuation and stock price. Over the past year, Bloom Energy's stock price has achieved a cumulative gain of more than 880%. Year-to-date, the stock had already doubled even before this latest massive order. Such a steep ascent has fully, or perhaps even excessively, priced in the market's high expectations for AI data center demand.

[Bloom Energy Analyst Ratings, Source: TradingKey]

Second is the divergence and skepticism among Wall Street analysts. According to research institution ratings, the average consensus rating for Bloom Energy is "Hold," with an average price target of approximately $144.61. Given Monday's closing price of $176.67, this implies an institutional consensus of roughly 20% downside potential from current levels.

This significant valuation gap indicates that professional institutions generally believe the current rally may be bubbly.

From an institutional perspective, Jefferies maintains an "Underperform" rating with a price target of only $102, citing insufficient transparency in the company's capacity expansion; Citigroup assigns a "Neutral" rating with a $162 target; while Morgan Stanley maintains an "Overweight" rating with a $184 target. The severe divergence among institutions is itself a risk signal.

At the same time, the cost of SOFC technology remains high, which is the core obstacle restricting its mass adoption. Although the long-term potential for cost reduction is substantial, significant uncertainty remains in the transition from high costs to economic viability, especially in the face of natural gas price volatility and technological iterations from competitors.

Furthermore, signals from insider selling are also sounding the alarm. Over the past 90 days, company insiders have sold a cumulative total of approximately 370,000 shares, involving roughly $61.4 million. This is often a signal for caution when stock prices are at historical highs.

Overall, Bloom Energy's AI data center demand thesis is solid, and the securing of a 2.8GW order further validates the company's strategy in the AI power supply sector. However, from a secondary market perspective, the nearly tenfold increase in stock price over the past year has already fully reflected most of the known positive catalysts.

For investors already holding positions, this massive order may represent the realization of a major positive; however, for investors on the sidelines, current valuation levels are quite expensive, and the analyst consensus price suggests potential correction risks. Any investment decision should be based on independent judgment according to one's own risk tolerance and investment horizon.

Will Oracle expand its partnership with Bloom Energy in the future?

Analysis suggests that Oracle's demand for Bloom Energy is not a one-time purchase but a structural dependency based on its strategic expansion of AI infrastructure.

First, Oracle's power capacity is far from meeting its demand. Oracle has initiated large-scale construction projects to build AI data centers for clients such as OpenAI and Elon Musk’s xAI, with capital expenditures expected to reach $50 billion for the fiscal year ending in May.

Oracle CEO Safra Catz has repeatedly emphasized in recent earnings calls: "Power, not chips, has become the number one bottleneck for the expansion of Oracle Cloud Infrastructure (OCI)."

Second, the tie between Oracle and Bloom Energy is moving from a "customer relationship" toward a "capital partnership." In this 2.8GW agreement, Oracle not only signed for the initial 1.2GW but also secured the right to purchase approximately 3.5 million shares of Bloom Energy through warrants, meaning Oracle is transforming from a simple procurement client into a potential controller of its energy supply chain. This deep integration at the capital level paves the way for future additional orders.

The trend of data centers evolving toward "going off-grid" is irreversible. Bloom Energy's research predicts that by 2030, about one-third of data centers will be 100% self-powered, a 22% increase from previous forecasts. As the U.S. grid load continues to approach its limit, demand for onsite power generation solutions will only further expand.

Oracle will not only continue to increase its procurement of Bloom Energy fuel cell systems but is also likely to pursue deeper strategic integration in joint technology development, power capacity reservation, and even at the equity level. Considering Oracle has planned a massive computing power blueprint for clients like OpenAI and xAI, subsequent follow-on orders are almost a certainty.

TradingKey's analysis suggests that the performance evaluation after the initial 1.2GW deployment in 2027, the disclosure of power solutions for Oracle's next round of data center site selection, and whether other hyperscalers follow Oracle's lead in establishing similar strategic partnerships with Bloom Energy will be key milestones for Bloom Energy investors and the market to watch.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.