Blue Owl Crisis: U.S. Private Debt Faces Risk of Subprime Crisis Repeat?

AI Podcast

The global private credit market, valued at $1.8 trillion, faces significant stress exemplified by Blue Owl Capital's redemption restrictions. Concerns over asset valuation and liquidity, particularly regarding software loans, have led to a sharp decline in Blue Owl's shares. Recent bankruptcies of highly leveraged borrowers have intensified fears of contagion in private credit and leveraged loan markets, with warnings from financial leaders about loose corporate lending. The Blue Owl situation is being closely watched as a potential signal of broader issues within the private credit industry, raising calls for increased scrutiny and stress tests to protect investors.

TradingKey - The global private credit market, valued at $1.8 trillion, is facing its toughest test to date. Recent bankruptcies, fraud allegations, and redemption freezes have exposed the vulnerabilities of this market, which grew rapidly under the low interest rates and loose liquidity following the 2008 financial crisis.

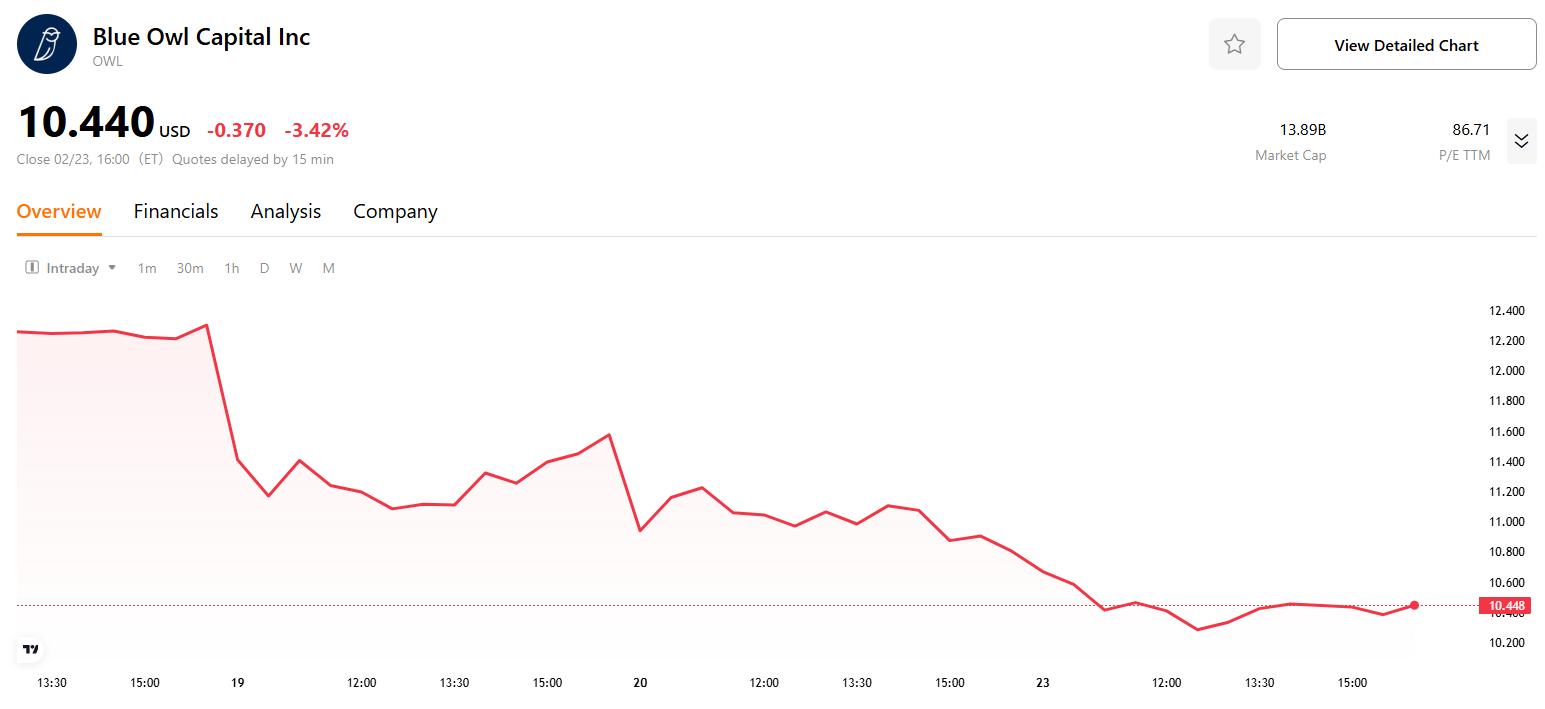

Last week, Blue Owl Capital ( OWL) announced permanent restrictions on redemptions for its OBDC II fund and plans to sell assets in tranches to return cash to investors quarterly. This change means investors can no longer choose their own redemption timing, and it cancels a previous arrangement that allowed for the withdrawal of 5% of the fund's cash each quarter.

According to a company statement, the OBDC II fund will sell $1.4 billion worth of loans at 99.7% of par value, primarily to four North American public pension funds and insurance investors. 97% of the assets sold are senior secured debt, covering 128 companies across 27 industries, with the internet software and services sector accounting for the highest proportion.

However, this news caused Blue Owl shares to fall sharply for several consecutive days, with a cumulative decline of over 15% in the past five days. Although top management emphasized that the assets were sold near book value, some analysts view the move as an "emergency liquidation" to cope with a wave of redemptions.

Valuation and Liquidity Challenges

Blue Owl's problems were initially triggered by valuations. Investors are concerned that the actual value of loans in the OBDC II fund may be lower than their book value, particularly since a large portion of its loans went to software companies. Another fund with a similar portfolio is trading at a significant discount to net asset value (NAV), indicating widespread market skepticism about the value of these assets.

Valuation issues further led to a liquidity crisis. To stop the outflow of funds, Blue Owl had attempted to merge OBDC II with a listed peer, but the move was terminated due to dissatisfaction, as it required investors to accept an actual impairment of assets in exchange for the right to sell shares.

Facing the dual challenges of valuation and liquidity, Blue Owl decided to sell a portion of its loans to other asset managers at prices close to par in an attempt to justify the value of its loans. However, the transaction failed to fully dispel market doubts, as one of the buyers was its own insurance subsidiary, raising concerns about the fairness of the deal.

Meanwhile, activist investor Saba Capital Management is acquiring shares of the Blue Owl fund at significant discounts, reflecting persistent market doubts about its asset quality.

Risk Exposure

In recent years, warning signs have frequently emerged in the private credit market, highlighting significant latent risks within the industry.

In September 2025, concerns over exposure to highly leveraged borrowers intensified following the successive bankruptcies of auto parts manufacturer First Brands and subprime lender Tricolor Holdings.

The collapse of these companies has heightened fears of risk contagion in the private credit and leveraged loan markets, as several banks—including UBS O'Connor and Jefferies Financial Group—had extended hundreds of millions of dollars in loans before their downfall.

JPMorgan Chase ( JPM) CEO Jamie Dimon warned that corporate lending has been too loose over the past decade, stating, "When you see one cockroach, there are probably many more."

These events triggered a wave of market selling upon the discovery that mainstream banks also held loans to these high-risk borrowers. According to Moody's data, major U.S. banks have extended approximately $300 billion in loans to private credit institutions, fueling the industry's expansion. During the Trump administration, private debt gradually expanded into millions of American brokerage and retirement accounts, increasing the likelihood of transmitting greater risk to other parts of the financial system.

Against this backdrop, the Blue Owl incident has garnered widespread market attention. There are concerns that it could be a signal of deeper underlying problems within the private credit industry.

Barclays ( BCS) analyst Ben Troisi noted that the Blue Owl transaction could serve as a model for other private credit firms. If similar deals occur frequently, they could deepen the interconnections between non-bank financial sectors, making risks increasingly difficult to track.

Jimmy Chang, Chief Investment Officer at Rockefeller Global Family Office, pointed out that the current question is whether this is an isolated incident involving a single company or a warning signal for the entire industry.

Former PIMCO CEO Mohamed El-Erian warned that Blue Owl's sale could be a warning sign of a larger crisis facing the market, similar to the precursors of the 2008 financial crisis.

U.S. Senator Elizabeth Warren also warned that Blue Owl's issues might be just the tip of the iceberg, calling for stress tests on the private credit industry to protect investors from high-risk assets.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.