Market Cap Erased, Successive Downgrades? Wall Street Is Re-evaluating Microsoft’s AI Future

AI Podcast

Microsoft's stock has declined over 12% year-to-date, falling below a $3 trillion market cap due to significant AI infrastructure investments. Investors are scrutinizing the balance between high capital expenditure and actual returns, questioning the sustainability of current valuations. The company's heavy reliance on OpenAI for cloud contracts and potential user adoption challenges for Copilot also raise concerns. This strategic pressure, coupled with competitive threats and slowing Azure growth, has led to recent rating downgrades, with analysts questioning the long-term profitability and business model under intense AI investment demands.

TradingKey - At the beginning of 2026, tech giant Microsoft ( MSFT) experienced a less-than-ideal start to the year. As of now, its stock price has fallen by more than 12% year-to-date, and its total market capitalization briefly dipped below the $3 trillion mark. The tech company, which once firmly held the title of the world's most valuable company, has now slipped to the third position globally.

Prior to this, driven by strong growth in its Azure cloud business, Microsoft's market value once surpassed $4 trillion, reaching an unprecedented peak of $4.15 trillion. This not only set a new historical record for the company but also made Microsoft the second technology firm in the world, after Nvidia, to cross the $4 trillion threshold.

As a former leader in technological innovation, why has Microsoft suddenly appeared to stumble in this wave of AI? What are the underlying issues?

Warning Signs Beneath the Valuation

In 2026, several tech companies announced ambitious capital expenditure plans, with AI infrastructure taking center stage. Microsoft, naturally, was unwilling to fall behind—but it is precisely this "heavy-handed" investment that has prompted the market to rethink the sustainability of tech giants' high valuations.

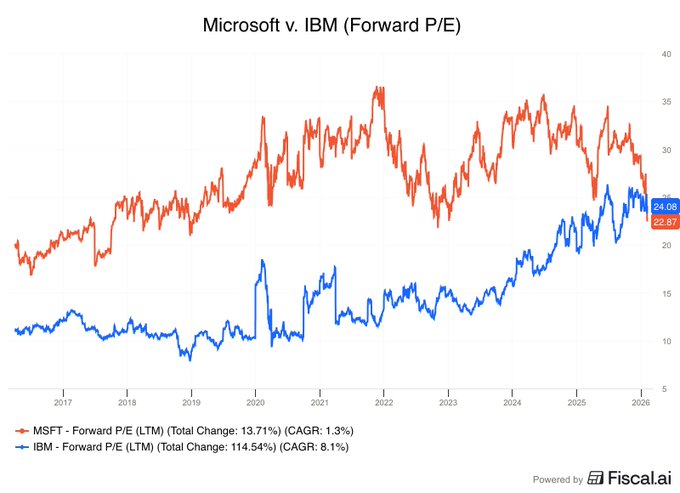

Data shows that Microsoft's forward price-to-earnings (P/E) ratio has dropped to 23.0x, lower than that of IBM ( IBM) at 23.7x. This valuation inversion is quite rare in the tech sector; the last time Microsoft's P/E ratio was lower than IBM's dates back to July 2013. From a certain perspective, Microsoft's valuation has been "discounted" by the market.

Several analysts pointed out that the core issue behind Microsoft's constrained valuation is not a loss of growth potential, but rather a new logic of scrutiny from investors regarding the balance between its AI spending and actual returns. Facing years of AI strategy and product rollouts, the market expects not just forward-looking narratives, but clearly visible monetization paths.

AI Investment Under Question?

According to market forecasts, the total capital expenditure for Microsoft and Alphabet ( GOOGL ), Meta ( META ), and Amazon ( AMZN )—the four hyperscale cloud service providers—in 2026 is expected to total $650 billion. This figure is not only 60% higher than in 2025 but also exceeds the market's initial expectations by $150 billion.

As an active promoter of AI implementation, Microsoft is also accelerating its investment. According to FactSet projections, Microsoft's capital expenditure in 2026 will reach $115 billion, with spending on data center construction increasing by 66% year-over-year. This trend is unlikely to reverse in the short term, and some believe that Microsoft's heavy investment could continue until 2028 or beyond.

Meanwhile, Amazon is expected to invest over $200 billion in 2026, Google's investment may range between $175 billion and $185 billion, and Meta plans to spend $115 billion to $135 billion. It is clear that this is an arms race focused on AI infrastructure, and no tech giant wants to fall behind.

However, the flip side of massive capital expenditure is sustained pressure on free cash flow, prolonged investment return cycles, and a fundamental shift from an asset-light to an asset-heavy model. Aaron Clark, portfolio manager at GW&K Investment Management, noted that this trend of intensified spending could lead to tech giants having heavier physical infrastructure, higher operating costs, less free cash flow, and a business structure more reliant on debt financing.

He further pointed out: "The current high-investment model is changing market expectations. In the past, these companies earned high valuations by relying on light assets, but as spending becomes a necessary 'permanent state,' investors are beginning to doubt whether the high-valuation framework can still hold."

Clark believes that what the market is currently grappling with is whether this round of investment belongs to the "land grab phase" of the AI era or has moved toward a permanent reshaping of cost structures. He warned that if these expenditures cannot be converted into stable returns, companies like Amazon and Meta could even see negative free cash flow in 2026.

Taking Microsoft as an example, its continuous investment in its flagship AI product, Copilot, is seen as a vital part of realizing its AI strategy. This feature has been embedded into core product lines such as Office, Windows, and Azure, with high expectations. However, in reality, the feedback has not been entirely ideal. Market observers point out that whether in terms of enterprise adoption rates or individual user stickiness, current performance has fallen short of expectations, and there is even a risk of losing some users.

Over-reliance on OpenAI

According to Microsoft's latest financial report, the company has explicitly disclosed for the first time its high degree of dependence on OpenAI in its cloud business—approximately 45% of its $625 billion in cumulative future cloud contracts come from OpenAI-related partnership orders. This proportion shows that although OpenAI's direct contribution to Microsoft's overall revenue remains limited, its share in cloud service contract backlogs and future procurement commitments can no longer be ignored.

In other words, despite the deeply integrated partnership between Microsoft and OpenAI, the high reliance on a single customer, especially concentrated in key business areas, is triggering a new round of discussion in the market regarding the stability of its business structure. Generally, any core business that leans too heavily on a few customers can create potential operational risks and is unhealthy in the long run.

It is not just Microsoft; since 2026, many large tech companies such as Oracle ( ORCL ), AMD ( AMD ), and others have also established various levels of partnership with OpenAI. However, as the market's assessment of the timing of AI investment returns has turned more cautious, these tech stocks have all seen varying degrees of adjustment this year.

In the past, OpenAI was a major force driving Microsoft's AI strategy, symbolizing its frontier deployment in the commercialization of AI scenarios. But now, OpenAI has also become an "uncertain variable" in terms of valuation for Microsoft and the entire tech industry. The market has begun to reassess this partnership, fearing hidden risks such as overly concentrated contracts, excessive betting on a single technological path, and limited future fulfillment capabilities.

Microsoft Ratings Downgraded Successively

As Wall Street begins to reassess the potential structural impact of artificial intelligence on the software industry, tech giant Microsoft has suffered two consecutive ratings downgrades in just one week.

The most recent downgrade came from Melius Research, which lowered Microsoft's stock rating from "Buy" to "Hold" on Monday. The primary reason is that the research firm expressed strong concerns over Microsoft's growing capital expenditure (CapEx) burden and the profitability of its AI productivity line, Copilot.

The week prior, Stifel also downgraded Microsoft, citing a slight slowdown in the growth of its Azure cloud computing business and market doubts about its growth resilience.

Melius analyst Ben Reitzes noted in the report that Microsoft is currently facing a situation where multiple challenges are overlapping. On one hand, alternative products (such as Cowork) from emerging AI companies like Anthropic are threatening Microsoft's dominance in the productivity suite market.

On the other hand, to maintain market competitiveness, Microsoft may be forced to bundle Copilot as a free component, which would erode revenue and profits in its core productivity division.

Reitzes further stated that high-intensity AI investment will also consume Azure resources that would otherwise be used for external customer services, potentially impacting the revenue performance of the cloud business. He stated frankly: "In this situation, Microsoft's most profitable business lines may face a marginal slowdown, and the synergy between the Azure and Office businesses has instead become a burden."

In fact, Microsoft's overall stock price weakness this year is related to the strong market reaction when its results were announced earlier in the year. Analysts generally expressed concern about the slowdown in Azure's growth and its overly aggressive AI capital expenditure plans, and these issues quickly became the catalyst for the release of stock price pressure.

Reitzes believes that Microsoft is caught in a market game where it is "hard to advance or retreat": if it wants to catch up with Alphabet and Amazon, it must invest heavily in AI infrastructure, thereby affecting free cash flow and reducing financial flexibility; but if it stays put, it might be seen by the market as lacking execution or failing to effectively seize AI transformation opportunities—both scenarios are potential negatives for its valuation framework.

此外,Reitzes还质疑当前AI商业化的可持续性。他指出,“我们愈发认为,客户为AI功能‘额外付费’的逻辑并不成立。若最终Copilot只能免费使用,不仅难以带来预期增长,还会在长期拉高运营成本。”

While maintaining a more cautious expectation for future profitability, Melius further lowered its price target for Microsoft to $430, becoming one of the more pessimistic calls among current public ratings on Wall Street.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.