Netflix Q4 Earnings Preview: Ad Business May Lead Growth Engine, Warner Bros. Deal Is Key Stock Variable

AI Podcast

Netflix is set to report Q4 earnings with projected revenue of $11.97 billion. However, market attention is focused on the potential acquisition of Warner Bros. Discovery assets, with speculation of an all-cash offer to counter competition. While this deal's strategic importance is high, an all-cash acquisition could pressure 2026 EPS and stock price. Despite past declines, analysts remain optimistic, citing strong advertising growth as a key driver and anticipating a diversified revenue structure by 2026. Upward estimate revisions for EPS and revenue reflect analyst confidence, with an average price target of $124.39.

TradingKey - Streaming Giant Netflix (NFLX.US) is scheduled to release its fourth-quarter earnings after the market closes on January 20. However, the market's focus may no longer be limited to the quarterly performance itself, but is gradually shifting toward the latest progress and long-term strategic implications of the company's proposed acquisition of certain Warner Bros. Discovery (WBD) assets.

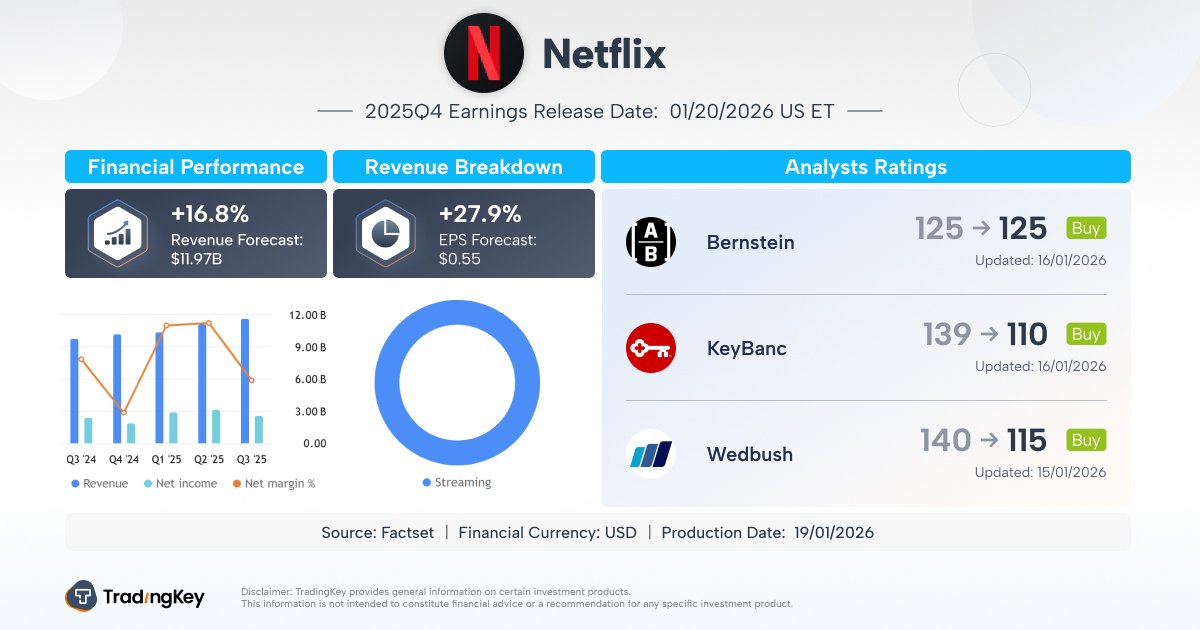

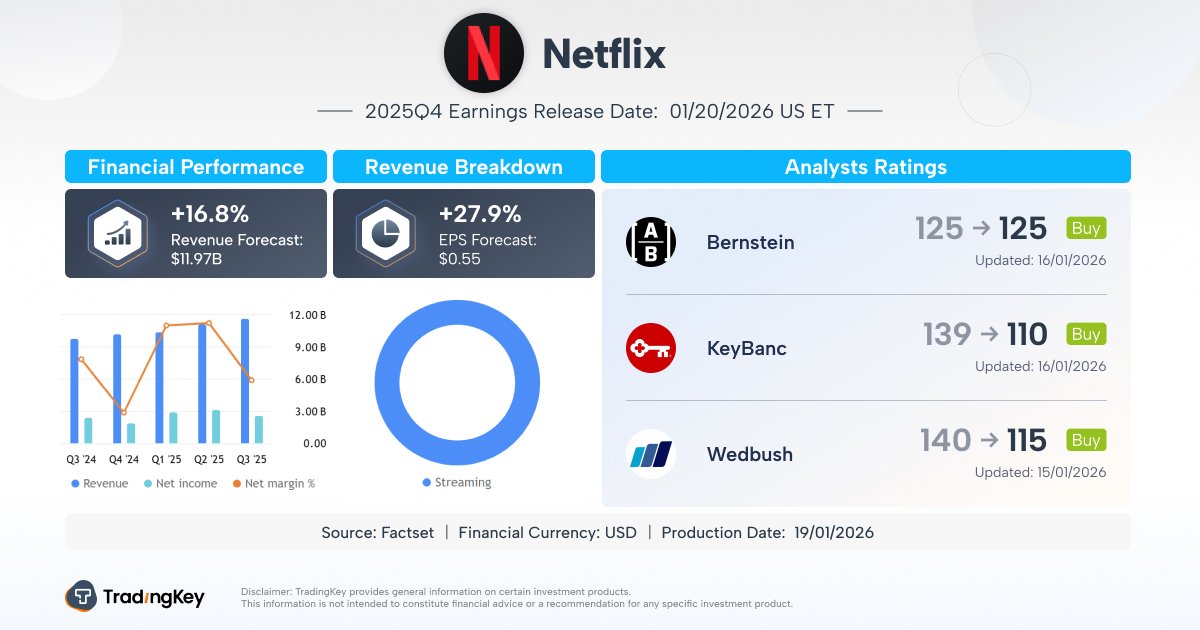

According to FactSet data, analysts expect Netflix's Q4 revenue to be $11.97 billion, a year-over-year increase of 16.8%, with earnings per share (EPS) of approximately $0.55.

[Netflix Q4 Earnings Forecast, Source: TradingKey]

Faced with hostile takeover competition from Paramount Skydance (PSKY), market rumors suggest that Netflix (NFLX) may pivot from its initial cash-and-stock acquisition model to an all-cash offer to enhance its competitiveness.

Market analysis suggests that the strategic significance of this potential deal is, to some extent, overshadowing the importance of the earnings data itself. Although the company's long-term growth positioning is clear, a shift to an all-cash acquisition of Warner Bros. Discovery (WBD) could weigh on earnings per share in 2026, thereby exerting significant downward pressure on the stock price.

Notably, due to weakening guidance, earnings misses, and uncertainties surrounding the Warner Bros. acquisition, the stock has fallen more than 34% from its 2025 highs.

Excluding the uncertainties brought by the acquisition, most market analysts believe that the significant acceleration in advertising business growth within subscriptions remains the primary driver for Netflix (NFLX) stock, particularly as subscriber numbers recover steadily following a relatively flat third quarter.

In terms of content supply, the final season of "Stranger Things," live NFL games during the Christmas window, and the third installment of "Knives Out" starring Daniel Craig are all classic "traffic-driving" productions. This has led Wall Street to generally believe that Netflix's fourth-quarter revenue performance is likely to be even more impressive than the previous three quarters.

Wedbush analyst Alicia Reese believes the market may be underestimating Netflix's (NFLX) progress in its global advertising layout. As the advertising ecosystem takes shape, this segment is entering a true scaling phase.

The firm expects advertising revenue to become Netflix's core revenue engine by 2026 and further unlock greater commercial potential in 2027. This signifies that Netflix is steadily transitioning from a single model heavily dependent on subscription fees to a more diversified revenue structure.

[Most analysts remain generally optimistic, issuing "Buy" ratings or higher, Source: TradingKey]

According to TradingKey's stock rating tool, Wall Street analysts are generally optimistic, maintaining a "Buy" rating. The average price target is $124.39, representing a potential upside of up to 41.35%.

Looking at earnings revision trends, over the past three months, EPS estimates have seen 18 upward revisions against only 9 downward revisions; revenue estimates have seen 25 upward revisions compared to just 6 downward revisions, reflecting confidence in Netflix's (NFLX) outlook.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.