SpaceX and Tesla’s Strategic Convergence: Why Musk Must Push for a SpaceX IPO Now

AI Podcast

The SpaceX IPO aims to fund its ambitious Mars colonization by tapping into global liquidity, not traditional private equity. This move will liberate Tesla from serving as Musk's primary capital source, potentially allowing for share buybacks. SpaceX's core businesses—launch services, Starlink, and Starship—are projected for significant growth. Starlink is pivotal for Tesla's autonomous systems, while Starship enables space data centers. This synergy, powered by the IPO, enhances Tesla's AI computing capacity by overcoming ground-based energy and data gravity limitations, offering a light-speed communication advantage. Ultimately, this positions Tesla as an "Interstellar Infrastructure Supplier." Short-term risks include capital diversion to SpaceX and unresolved technical challenges for orbital data centers.

Will the Tesla stock in your portfolio be abandoned because of SpaceX’s listing? This is likely the source of the most intense anxiety for secondary market investors recently. After all, when investors are given the chance to bet directly on the "stars and the universe," who would still linger on electric vehicles down on Earth?

However, within Musk's grand chessboard, this "either/or" mindset is precisely the greatest misreading of the battlefield. SpaceX’s IPO is by no means a bloodletting of Tesla’s capital; on the contrary, it is the booster rocket for Tesla to complete its final evolutionary form. If SpaceX is responsible for building the physical skeleton leading to the future, then Tesla is responsible for injecting the intelligent soul. The strategic convergence of the two constitutes the complete closed loop of Musk’s business empire.

1. Why is the SpaceX IPO Worth Watching? When Private Equity Can No Longer Support Musk’s Ambition

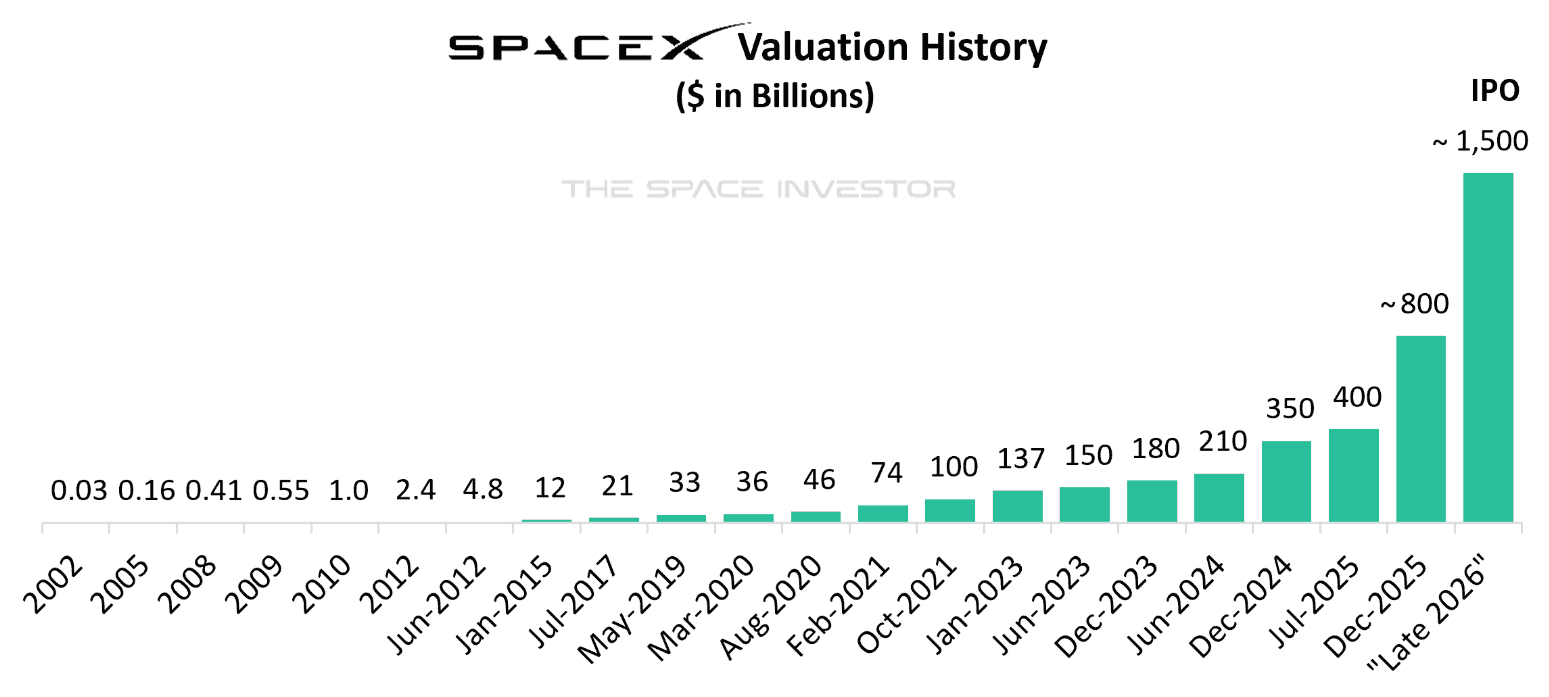

Source: the space investor

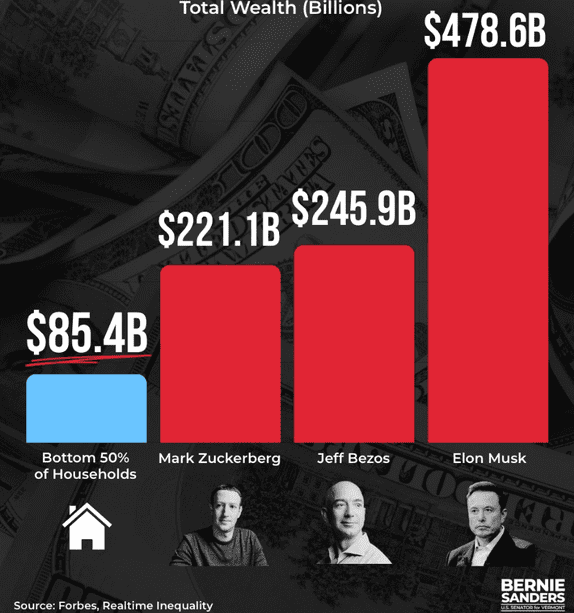

SpaceX’s current valuation in the private market has reached astonishing levels, with rumors suggesting an IPO target valuation as high as $1.5 trillion. Simultaneously, Musk’s personal net worth is approaching $500 billion. It seems he is already "wealthy enough to rival nations," so why reach out to the public for money?

Source: Forbes

Because in the face of the Mars Plan, these figures are still a drop in the bucket. According to Musk’s public vision, establishing a self-sustaining city on Mars requires transporting at least 1 million tons of materials to the Martian surface. Based on the current design payload of "Starship," this implies a fleet of approximately 1,000 ships. Including the need for orbital refueling, the total number of launches for round trips would be at least 10,000. Even if Starship can drive the cost of a single launch down to $100 million (a fraction of the current industry average), the launch costs alone would amount to $1 trillion.

There is a huge cognitive error here: Market Cap does not equal Cash. Although Nvidia has a market cap of $4 trillion and the US GDP forecast for 2025 is about $31 trillion, this does not mean $1 trillion is a small number. A cash expenditure (CapEx) of $1 trillion exceeds the US Department of Defense's total annual budget (approx. $850 billion) and far surpasses the cash reserves on the books of any tech giant.

The conclusion is obvious: Relying on Musk’s personal wealth, the limited private equity (PE) market, or even the traditional terrestrial economic system cannot support this ambition. SpaceX chooses to IPO not for traditional shareholder cash-outs, but to initiate a "crowdfunding" campaign targeting humanity's excess liquidity, thereby completing the most expensive engineering project in human history.

For Tesla shareholders, this massive capital requirement is no longer a nightmare, but a relief. In the past, Tesla actually played the role of the "donor heart" for Musk’s empire. Whenever SpaceX R&D hit a snag or Twitter (now X) urgently needed funds, Tesla’s stock price would often fluctuate violently due to Musk’s large-scale sell-offs, leaving shareholders trembling.

After the IPO, SpaceX will possess an independent financing platform with strong "blood-making" capabilities. Tesla will no longer be Musk’s ATM, but a protected core asset. Furthermore, as SpaceX’s liquidity is released, Musk could potentially use his personal SpaceX holdings for collateral or monetization to repurchase Tesla shares, thereby increasing his control and ensuring Tesla’s AI development direction isn't swayed by short-term capital.

2. SpaceX Business Core Analysis: Building the "Space Backend" for Tesla

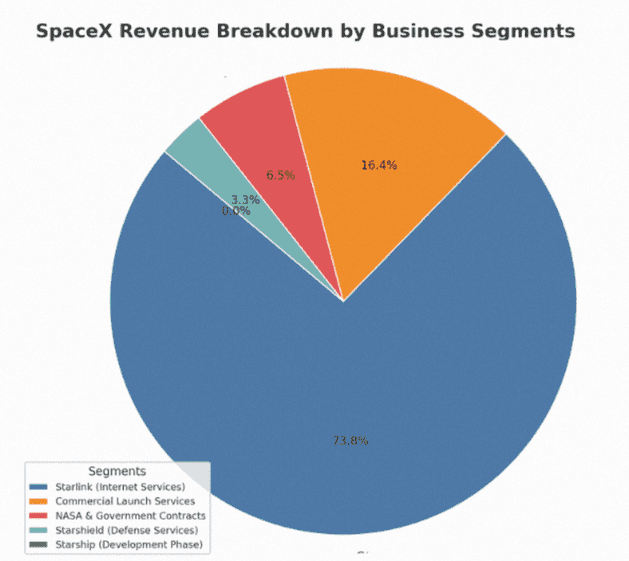

Before discussing Mars, we need to understand SpaceX’s current money-making logic. According to estimates by the authoritative space media outlet Payload, SpaceX’s revenue is expected to reach $22 billion to $24 billion in 2026, with a year-over-year growth rate exceeding 50%. This is not just a rocket company; it is a massive commercial ecosystem taking shape. We can break down its business structure through the following three core pillars:

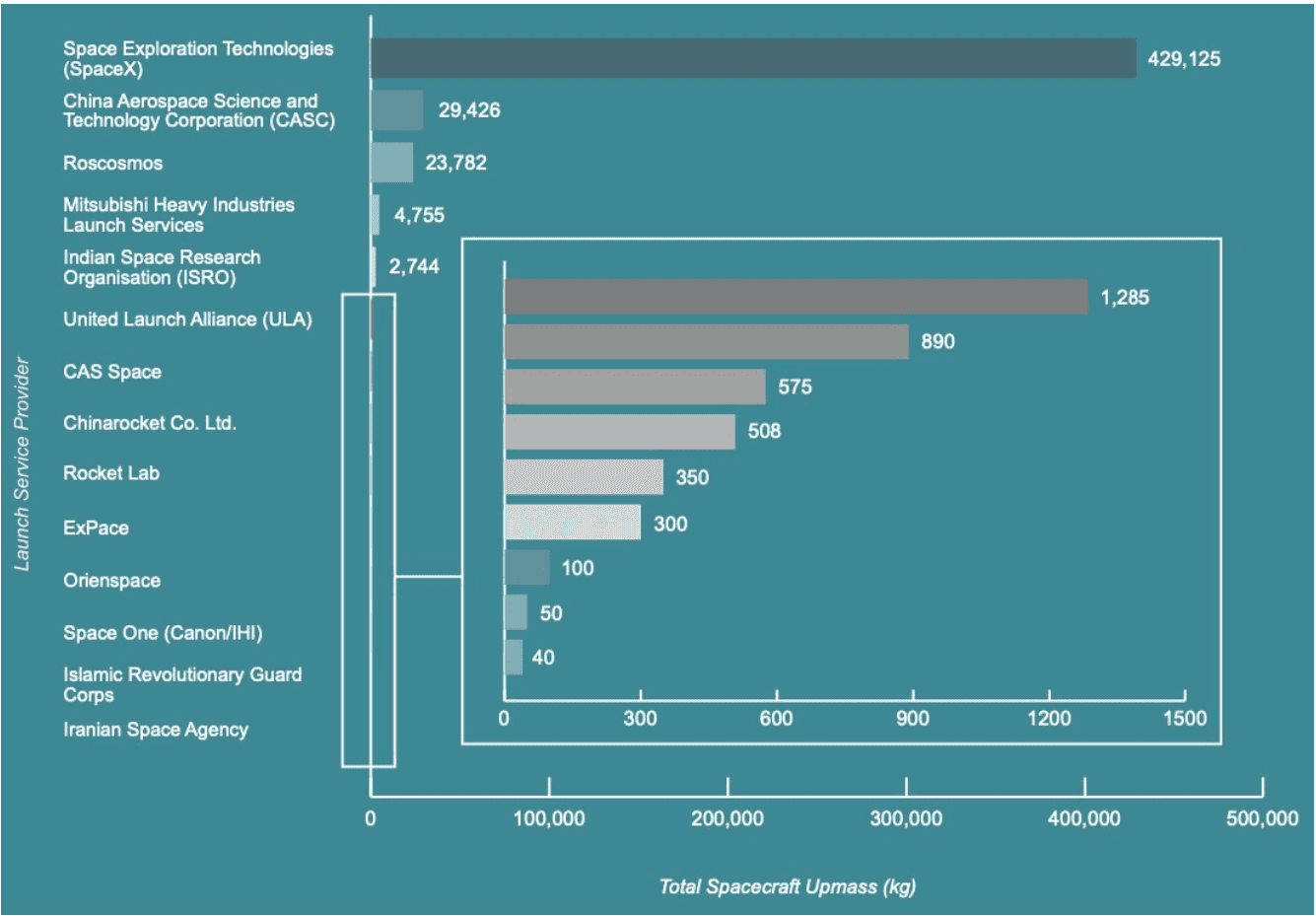

- Launch Business—Absolute Monopoly on Global Capacity: SpaceX’s Falcon 9 and Falcon Heavy currently dominate the US launch market. The data point that best illustrates this monopoly is: in 2024, SpaceX alone accounted for over 90% of the total upmass (payload mass sent to orbit) globally, while the sum of all other countries and companies was less than 10%. This means SpaceX holds the pricing power for access to space. With the commercialization of Starship, this segment will gradually transform into an "internal logistics department," shifting its core mission from serving external clients to serving Musk’s own Starlink deployment and Mars transport.

Source: Bryce Briefing

- Starlink—From Broadband to Global Neural Network: This is SpaceX’s current growth engine, estimated to contribute over 70% of the company's revenue. As of now, the number of Starlink satellites in orbit exceeds 9,000. How terrifying is this figure? It accounts for over 65% of all active satellites currently orbiting humanity. Starlink is not just about providing broadband to millions of users globally; essentially, it is a low-orbit communication constellation wrapping the Earth. For Tesla, Starlink’s significance goes far beyond broadband service. Since ground base stations have massive blind spots in oceans, deserts, and airspace, Starlink will become the global neural system for Tesla’s Robotaxi fleet and Optimus robots. It ensures that whether it's a robot mining in the Sahara or a logistics ship crossing the Pacific, they remain online in real-time. This is a distributed data center network with extremely high barriers to entry.

- Starship—The Scalable Physical Carrier: Although Starship is currently in the testing phase and has not generated large-scale revenue, it is the physical foundation of the entire strategy. The core value of Starship lies not in its "size," but in its "volume" (quantity/scale). Only with Starship’s hundred-ton payload capacity and extremely low unit cost is it possible to send thousands of tons of GPU servers, cooling equipment, and energy modules into orbit. It is the sole prerequisite for the future construction of space data centers.

Source: retirewithrohit

3. Logic Upgrade: SpaceX’s "Brain" is Actually Tesla

This is the logic most easily overlooked by the market, yet it holds the most explosive potential: The money raised by the SpaceX IPO is essentially expanding Tesla’s "brain capacity."

Musk has mentioned multiple times that while building data centers in space faces huge engineering challenges regarding heat dissipation and radiation, from the perspective of First Principles of Physics, this is not only "feasible" but perhaps an "inevitable path" for the development of AI civilization. As AI model parameters expand exponentially, terrestrial computing power is facing the limit challenges of physics. The combination of SpaceX and Tesla is reconstructing the future of AI computing power through three dimensions, from shallow to deep:

- First, escaping the "Energy Gravity" of the ground. Currently, training L5 autonomous driving (FSD) and general-purpose robots (Optimus) consumes astronomical amounts of electricity. The reality on the ground is cruel: tech giants are even forced to restart nuclear power plants to scramble for power, grid connection queues for new data centers often last years, and the terrestrial grid is overwhelmed. In space, the rules of the game change. There is no night, no clouds; solar energy is uninterrupted 24 hours a day, and the intensity far exceeds that on the ground. Deploying data centers in orbit using Starship is equivalent to building a "never-setting" exclusive power plant for Tesla. This provides Tesla with an exclusive computing environment that doesn't need to compete for limited earth resources, completely solving the bottleneck of energy expansion.

- Second, breaking "Data Gravity" with space-based edge computing. Tesla’s massive fleet generates oceans of video data daily. Transmitting all raw data back to ground data centers for cleaning and processing not only incurs extremely high bandwidth costs but also huge latency. Future Starlink satellites will no longer be mere signal repeaters but edge computing nodes equipped with Tesla’s proprietary AI chips. Data can be uploaded directly to the nearest satellite, completing preliminary cleaning and inference in orbit, sending only high-value data back to Earth. This "In-Orbit Processing" model will vastly improve FSD iteration efficiency, allowing Tesla’s algorithm evolution speed to far outpace competitors.

- Finally, a physical "Dimensional Strike"—The Speed of Light Advantage. This is the point that excites Wall Street the most. Physical laws dictate that light travels 30%-40% faster in a vacuum than in optical fiber (glass). Current networks require passing through countless ground cables and undersea cables—slow and circuitous. The "Space Laser Network" SpaceX is building allows data to transmit in straight lines through a vacuum. For global Robotaxi scheduling and real-time command, this physical speed advantage is a moat that no competitor relying on ground fiber can cross.

It can be said that if Microsoft Azure is OpenAI’s cloud service provider, then SpaceX is Tesla’s exclusive, physically isolated, energy-infinite, and light-speed "Space-Based Cloud Service Provider."

4. The Ultimate Vision—Optimus: The First "Natives" of Mars

Once we straighten out the logic of computing power and energy, the Mars Plan is no longer a distant sci-fi novel, but a clearly visible supply chain order.

What is the most expensive cost of going to Mars? Not rocket fuel, but "sustaining human life." Humans are too fragile; we need oxygen, water, food, and extremely expensive radiation protection equipment. According to First Principles, the most economical colonization plan is straightforward: Robots first, humans later.

In this closed loop, SpaceX provides cheap interstellar transport services (Starship) and orbital computing/communication support (Starlink + Orbital Data Centers); while Tesla is responsible for manufacturing the labor force capable of working in harsh environments (Optimus) and ground energy storage systems (Megapack).

Once SpaceX IPO funds are in place and Mars base construction begins, Tesla will receive the largest hardware procurement order in human history. Millions of Optimus robots will be sent to Mars, utilizing solar energy and local resources to build bases, paving the way for the subsequent arrival of humans. At this point, Tesla’s valuation logic will completely detach from "automaker" and even "terrestrial tech company," evolving into a true "Interstellar Infrastructure Supplier."

5. Capital & Valuation—The Seesaw of Two Giants

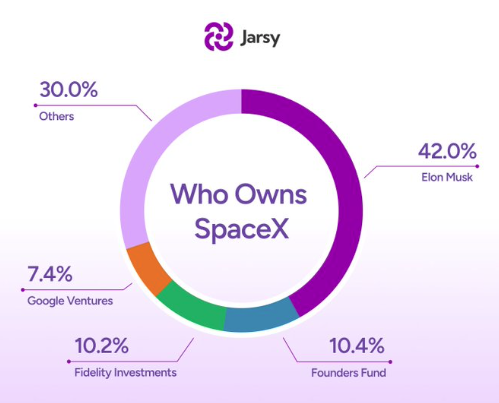

SpaceX does not need to look for cornerstone investors because global top-tier capital has already entered the game. From long-term financial capital represented by Fidelity to tech giants represented by Google and Oracle, they have already placed their bets with real money. For Google and Oracle, this is not just a financial investment, but a strategic hedge on space-based computing networks—they must ensure they are not excluded from the future physical infrastructure. However, even with giants gathering, Musk still locks down absolute control through a tight dual-class share structure. This sends a clear signal to all IPO participants: You are buying a ticket to the future, not the voice to steer the ship. This mechanism effectively isolates Wall Street’s pressure for short-term financial reports from Musk’s Mars vision spanning decades, ensuring the giant ship always sails according to the Chief Engineer’s will.

More importantly, if SpaceX lists with a $1.5 trillion valuation, it will become Tesla’s strongest "Value Anchor." Market logic will be forced to reconstruct: If SpaceX, as the company providing "Hard Infrastructure (Roads)," is worth $1.5 trillion, then the value cap for Tesla, the only entity in the ecosystem providing "Soft Intelligence & Labor (Cars/People)," will be blown wide open. As the "exclusive supplier" in Musk’s interstellar map, Tesla’s valuation logic will completely break away from "car manufacturing" and instead be viewed as a super-growth stock monopolizing the Martian economy. The more expensive SpaceX becomes, the higher the "gold content" of Tesla.

Source: Jarsy

6. Risk Warning

Despite the grand prospects, short-term risks remain. The most direct risk is capital diversion. In the short term, the market’s capital pool is limited, and institutional investors have caps on their allocation for "Musk concept stocks." SpaceX’s listing might siphon off some liquidity from Tesla, especially from passive funds that simply want "Musk exposure." Additionally, orbital data centers still face huge technical challenges; for example, how to solve the heat generated by high-density computing through radiative cooling in a vacuum remains an engineering problem that has not been fully conquered.

7. Conclusion: The Ticket to the Interstellar Age of Discovery

SpaceX’s IPO is destined to become a watershed moment in business history. It is not only to solve the funding gap for the Mars Plan but to break through the physical bottlenecks of Tesla’s AI evolution. We are witnessing an exciting positive feedback loop: The further SpaceX flies, the stronger orbital computing becomes; the stronger orbital computing becomes, the smarter Tesla’s FSD and robots get; the smarter the robots get, the lower the cost of building a Mars base.

For investors, this is no longer a choice between investing in the "Road" (SpaceX) or the "Car" (Tesla), but whether you are willing to bet on the next leap of human civilization. When Musk casts his gaze toward the stars, SpaceX and Tesla are the two wings in his hands. In this grand vision, pessimists are often right, but optimists are often successful. Are you ready for this ticket to the future?

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.