The Battle for Warner Bros. Discovery Assets – More Entertaining than Any Show They’ve Got

AI Podcast

Netflix's proposed acquisition of Warner Bros. Discovery's Studio and Streaming assets for $82.7 billion transforms Netflix into a studio powerhouse, leveraging WBD's extensive IP. The deal, offering WBD shareholders $27.75 per share ($23.25 cash, $4.50 NFLX stock), excludes WBD's declining Cable Networks segment. Despite initial market skepticism and concerns over valuation and debt, Netflix's strong cash flow suggests manageability. Regulatory approval remains a hurdle, though subscriber overlap may mitigate antitrust concerns. Paramount Skydance's higher cash bid poses a challenge, but Netflix's superior financials and strategic asset focus present a more robust post-merger outlook.

The Deal – A Brief Recap

The announcement on December 6th, 2025, confirming the Board-approved agreement for Netflix (NFLX) to acquire the Studio and Streaming assets of Warner Bros. Discovery (WBD) for an enterprise value (EV) of $82.7 billion, fundamentally alters the landscape of the global media industry. This transaction is viewed by NFLX management not merely as an ordinary acquisition, but as a "once-in-a-lifetime opportunity", a necessary, almost existential move to secure foundational, generational intellectual property (IP) that is virtually impossible to replicate or acquire elsewhere in the market. The securing of these assets transforms NFLX from primarily a dominant distribution platform into a studio powerhouse.

The primary driver of the deal is WBD’s massive and unmatched content library. This includes globally recognized franchises such as DC Comics, Harry Potter, Game of Thrones, The Matrix, Lord of the Rings, and Looney Tunes. Control over this IP is the new currency of the streaming wars, offering durability and unique differentiation.

The deal structure offers WBD shareholders $27.75 per share, comprised of a significant cash component and equity: $23.25 in cash and $4.50 worth of NFLX stock. The equity component is a powerful signal, as it demonstrates NFLX’s belief in its own future stock performance while offering WBD shareholders continued upside exposure to the combined, strengthened entity.

Crucially, the deal is highly specific and targeted: NFLX is only acquiring the high-growth, IP-rich assets: Studio Business (Warner Bros. Pictures, TV, etc.) and the Streaming business (Max/HBO), while planning to divest WBD’s Cable Networks segment. This segment, which houses legacy assets like CNN, TNT, and Discovery, is slated for a spin-off into a separate, independent entity.

The reasoning is backed by stark financial data and clear market trends: the traditional cable business is in an obvious trend of decline due to audience preference shifting decisively toward streaming and short-video formats. The WBD Networks segment revenue was down 22% in Q3, highlighting the strategic necessity of shedding this decaying asset.

A Deeper Dive

The market's initial reaction was deeply skeptical, leading to a dip in NFLX's stock price. In fact, the first rumors of a potential NFLX-WBD deal emerged in late October, and since then, NFLX has erased 22% of its share price. This skepticism centered on some traditional M&A fears:

Overpaying: The $82.7 Enterprise Value translates to a valuation multiple of approximately 25x forward EBITDA. This places the deal at the higher end of the range for recent studio M&A transactions. This premium pricing leads to the common investor fear of the "Winner's Curse"—that NFLX is paying too much and will struggle to generate sufficient returns on this colossal investment. The assumption is that the value creation potential must be immense to justify such a high multiple.

Asset-Heavy Transition: Historically, the source of NFLX's high profitability and market dominance was its asset-light model, which relied on minimizing capital expenditure and operational complexity. The WBD acquisition forces NFLX into an asset-heavy model, requiring it to manage vast physical studio infrastructure and navigate the complexities of traditional Hollywood production cycles. This fundamental shift introduces new risks and demands different managerial expertise.

The most pronounced worry for investors is the massive infusion of debt required to fund the cash portion of the deal.

The Scale of New Debt: NFLX currently holds $14.5 billion in gross debt with $9.3 billion in cash and short-term investments. The acquisition will necessitate NFLX taking on approximately $50 billion more debt - a massive number compared to the current debt.

Despite the scale, the combined entity's cash flow provides a definitive counterargument, confirming the debt is manageable.

Firstly, NFLX maintains extremely high operating efficiency, reflected in an operating margin of around 30%. This profitability provides a wide buffer against business fluctuations. This strong profitability translates directly into massive cash generation. NFLX's operating cash flow (OCF) for the first nine months of 2025 was a significant $8 billion. This figure underscores the company’s ability to generate immediate liquidity.

Secondly, the market anticipates the combined company's annual interest rate payments to be in the range of $2.5 - 3.0 billion. The current NFLX OCF alone could easily cover this amount, demonstrating an immediate interest coverage ratio of approximately 3x.

Furthermore, the acquired WBD streaming business is expected to contribute approximately $1.3billion in EBITDA, adding another secure money stream. This high level of sustained profitability and predictable cash generation capacity fundamentally mitigates the risk often associated with large M&A debt.

Will the Regulators Intervene? Depends on How Good Netflix Lawyers are

Apart from the worries investors have, there is a significant degree of uncertainty whether the regulators will find the deal too anti-competitive and block it.

The theoretical subscriber base combines NFLX's 300 million subscribers globally with WBD streaming's 120million, totaling 420 million. Concerns over creating a streaming monopoly are addressed by the fact that the overlap between the two subscriber groups is quite significant. Therefore, the actual count of unique global users will be far less than 420 million, softening the antitrust argument against market concentration.

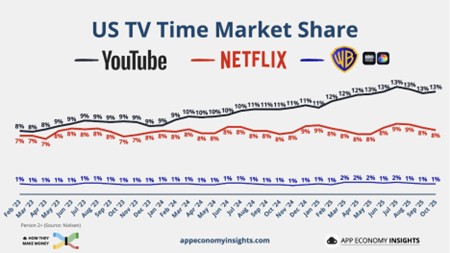

In fact, NFLX views its true competition as the platforms competing for minutes of user time—the "Attention Economy." NFLX is directly fighting YouTube, Reels, and TikTok for viewers' attention. The strategic focus is to encourage viewers to spend more time on their platform. Because YouTube is currently dominating this space, a successful WBD integration that leads to more in-demand, exclusive content is essential to increase NFLX’s share of US TV time and drive significant future ad revenue growth.

Also, from a consumer perspective, most probably Netflix may bundle their own streaming plan with the WBD’s HBO, so viewers will probably have to pay for a plan that is slightly more expensive but with much richer choice of content, which essentially is not so consumer unfriendly.

Overall, Netflix has a strong case to clear the regulatory check-ups, but they need to present the arguments in the best possible way, and of course, engage with top lawyers.

Source: appeconomyinsights.com

The Upside is Big

The deal's primary strategic justification lies in creating an unassailable content moat and enabling long-term revenue acceleration.

The integration grants NFLX massive production capacity and greater creative control, leading to a surge in in-house content. This control reduces reliance on unpredictable licensing deals, and by creating unique in-house content, NFLX can permanently differentiate itself from the competitors.

Also, the company will be able to leverage this massive evergreen content that Warner possesses and create new content based on it. Just imagine, a Harry Potter series or a new DC series.

The goal for NFLX is to gain more power to increase the subscription pricing with less risk of customer churn, which is the most reliable pathway to sustained, high revenue growth.

The management’s confidence is reflected in their willingness to use more cash than stock, demonstrating their belief that the current NFLX stock price is undervalued and will appreciate significantly post-merger. Furthermore, the commitment to a giant breakup fee of $5.8 billion, one of the largest ever, signals the highest level of conviction that NFLX can navigate all hurdles to successfully complete the transaction.

Post-Merger Risks

Despite the strong financial arguments, the NFLX-WBD faces several critical operational challenges:

Overestimation of Synergies: Historically, most mega-deals fail to meet the high synergy expectations set by management. What NFLX has promised is $2-3 billion of cost savings, primarily coming from the operating expenses.

Management Experience Gap: While NFLX management has an exceptional track record in growing and operating the streaming platform, they do not have solid experience with operating assets and legacy studio businesses like WBD. This lack of relevant operational expertise increases the risk of inefficient integration and poor resource allocation within the studio system.

Cultural Clash: The integration of a legacy, entrenched, creative Hollywood studio (Warner Bros.) with the highly data-driven, agile, Silicon Valley culture of Netflix will inevitably lead to a cultural clash. This friction can manifest as employee attrition, creative misalignment, and integration failures that erode the very value being acquired.

Brand Alienation: A critical risk is the potential for NFLX's creative decisions to be perceived by original fans as "ruining" their favorite franchises (e.g., Harry Potter, DC). Such backlash could diminish the intrinsic value of the IP, thus undermining the core strategic rationale for the acquisition.

Impact on the Cinema Industry

The deal has profound and lasting implications for the traditional cinema industry, a stakeholder currently not talked about, but directly impacted by WBD's studio decisions.

Warner Bros. is a major Hollywood studio, historically contributing an estimated 20-25% of annual U.S. box office revenue.

By having these studio assets under its control, NFLX will certainly prioritize the use for their own streaming needs, rather than “rent” the studio assets for third parties to produce their own movies. This means fewer movies are on at the cinema. Also, with streaming on their mind, NFLX will only put their movies in the cinema just for a short period of time before they put them on the streaming platform. This means the exclusive theatrical window will be reduced, diminishing the urgency for consumers to attend cinemas. It is expected that the window will shrink from the current 30-45 days to as little as 15-30 days post-2029, reducing the value proposition of cinema tickets and likely contributing to lower ticket prices and shrinking revenues across the whole cinema sector.

The Hostile Takeover: Paramount Skydance (PSKY) Challenge

The complexity of the NFLX-WBD deal was amplified by a rapid hostile takeover bid launched by Paramount Skydance (PSKY), which chose to bypass the WBD board and appeal directly to shareholders.

The deal between NFLX and WBD was board approved. A hostile takeover occurs when a bidder approaches the shareholders directly, often with a superior financial offer, as PSKY is currently doing. PSKY has been interested in the WBD assets for a while, and they were not happy with the fact that the WBD board prioritized Netflix over them. PSKY’s central argument is that the WBD board was not acting in the best financial interests of the WBD shareholders by accepting the lower bid; thus, in terms of a pure-money perspective, PSKY's offer appears to be better:

Source: Company Financials

Also, another focal point is that PSKY wants to acquire the whole WBD, including the cable assets (CNN, TNT, Discovery), unlike Netflix which is only interested in Streaming and the Studio.

The decision now rests on whether WBD shareholders prioritize the higher immediate cash return (PSKY) or the board-approved offer with long-term NFLX stock upside.

The Achilles' Heel of the PSKY Bid and Why NFLX has an Edge

Despite the higher price, the PSKY offer is heavily undermined by the company’s weak financial situation compared to NFLX. Netflix generates significantly more operating income, and it has lower net debt.

Source: Company Financials

The crucial question for financial viability is: "How can PSKY, with only $2.4 billion in TTM Operating Income, absorb WBD. NFLX, with $12.6 billion in operating income, is vastly better equipped to handle the resulting interest payments and service the debt load. The PSKY bid, while tempting, carries a much higher risk of financial distress post-merger.

Even PSKY market cap is the lowest among the three - $15.6 billion vs WBD ($67.5 bn) and NFLX ($441.9 bn).

As for the debt, the higher net debt compared to Netflix, almost certainly implies that PSKY has to borrow even more than what NFLX has to, making it even riskier.

Secondly, it is Strategic Sub-Optimality: PSKY is acquiring the entirety of WBD, including the declining Cable Networks assets. This is strategically inferior to NFLX's plan to strip away the bad assets and focus purely on high-growth streaming and studio assets.

Thirdly, even if the financial superiority of the NFLX bid convinces WBD shareholders, the deal faces significant external hurdles in the form of anti-trust scrutiny.

A PSKY-WBD merger would combine two major studios and two major cable network entities (Paramount/CBS + WBD's TNT/Discovery/CNN). This high degree of vertical and horizontal overlap in traditional media businesses could face fierce regulatory scrutiny than the NFLX streaming-focused deal.

The Political Wildcard and PSKY’s Influence

The PSKY bid also introduces a direct and complex political dimension to the M&A process, posing a significant non-market risk.

PSKY’s CEO is David Ellison, the son of tech mogul Larry Ellison. Larry Ellison is known to have close ties to President Donald Trump. This political proximity may play in favor of PSKY.

Also, WBD owns CNN, one of the most prominent news networks in the country and globally, that President Trump has historically disliked and publicly criticized. The prospect of CNN falling under the control of a close political ally could potentially make Trump even more in favor of PSKY instead of NFLX.

This variable makes the outcome less predictable than standard financial models would suggest, but PSKY winning the WBD due to political favoring may backfire badly.

Conclusion

Despite the higher, all-cash $30 per share bid from PSKY, all-in-all, the NFLX acquiring WBD appears to be the more logical move:

NFLX’s deal is strategically superior because it targets only the high-growth, future-facing assets (Streaming and Studio) while committing to strip away the declining Cable Networks.

NFLX possesses the unmatched profitability (30% operating margin) and cash generation ($9.5 billion TTM operating cash flow) required to service the massive debt load. PSKY's significantly weaker financials make it highly risky from a post-merger solvency perspective.

The inclusion of NFLX stock in the approved offer provides WBD shareholders with necessary exposure to the future upside of the streaming market leader, aligning their long-term interests far better than a pure cash exit.

Should We Buy NFLX stock now?

From what we have analyzed in this article, the upside potential for NFLX is big; however, we are talking about a very long timeframe. The battle with PSKY, the regulatory approval, will take months, and this long timeframe will be full of short-term noise, which is not worth betting on. However, ultimately, NFLX made the right strategic decision, rewarding the long-term investors.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.