Memory Giant Micron Delivers Stellar Q4 FY2025 with Explosive DRAM and HBM Growth

TradingKey - Micron Technology, Inc. (NASDAQ: MU) delivered a stellar Q4 FY2025 earnings report, exceeding expectations on revenue, earnings, and margins. The company reported total revenue of $11.32 billion, up 46% YoY and 22% sequentially, surpassing the consensus forecast of $11.1 billion. Non-GAAP diluted EPS came in at $3.03, beating estimates by 5.6% and reflecting 157% growth from the prior year. Following the earnings release, Micron's stock initially rose about 5% in after-hours trading, reflecting investor enthusiasm over strong AI-driven demand and margin expansion, but later down to nearly flat versus the prior day's close, likely reflecting a blend of profit-taking, valuation considerations following a strong run.

Source: TradingKey

Key Financial Results

Metric | Q4 FY2025 | Q4 FY2024 | Beat/Miss | Change (YoY) |

Total Revenue | $11.32B | $7.75B | Beat | +46% |

Adjusted EPS | $3.03 | $1.18 | Beat | +157% |

DRAM Revenue | $9.0B | $5.33B | Beat | +69% |

NAND Revenue | $2.3B | $2.37B | Miss | -3% |

Non-GAAP Gross Margin | 45.7% | 36.5% | Beat | +9.2 pp |

Operating Cash Flow | $5.73B | $3.41B | – | +68% |

Source: Micron, TradingKey

Segment and Strategic Performance

Micron’s Q4 FY2025 results demonstrate a clear strategic pivot toward high-margin products geared to AI and data center demand, markedly driving revenue growth and margin expansion.

DRAM and AI Infrastructure: DRAM revenue reached a quarterly all-time high of around $9.0 billion, representing roughly 80% of total revenue. This growth was fueled by a combination of double-digit average selling price (ASP) increases and moderate bit shipment growth amid tight supply conditions. HBM, critical for AI GPUs and accelerators in hyperscale data centers, generated nearly $2 billion in revenue for the quarter, translating into an annualized run rate approaching $8 billion. HBM revenue growth contributed significantly to DRAM growth. Production ramp of next-generation HBM4 products is progressing, supporting Micron’s competitive positioning relative to SK Hynix and Samsung.

NAND Performance under Market Pressure: NAND revenue remained steady at approximately $2.3 billion in Q4, accounting for around 20% of total revenue. Sequential growth stemmed mainly from ASP gains and a shift toward higher-value enterprise storage products; partially offsetting bit shipment declines due to ongoing market oversupply. Margins in NAND trailed DRAM expansion due to pricing pressures, but the ramp of advanced 3D NAND technology and emerging storage-class memory development aim to improve mid-term returns.

Mobile, Client, and Automotive Segments: The Mobile and Client segment rebounded with a 15.5% sequential increase in revenue to approximately $3.8 billion, underpinned by stable PC demand and normalized inventory levels, improving gross margins to 36%. The Automotive and Embedded segment grew 27% sequentially to about $1.43 billion, driven by increased adoption of AI-enabled memory solutions in automotive and industrial applications.

Financial Performance and Capital Outlook: Non-GAAP gross margin rose to 45.7%, driven by favorable product mix and scale, resulting in operating income of $3.96 billion. Operating cash flow totaled $5.7 billion, while capital expenditures of $4.9 billion for the quarter limited adjusted free cash flow to $0.8 billion, with $3.72 billion generated for the full year. Internal AI-based productivity tools enhanced manufacturing efficiency by 30-40%, improving yields and process control. Guidance for fiscal 2026 anticipates increased CapEx to be near $18 billion, primarily focused on DRAM fabs and equipment. The company ended the year with strong liquidity of approximately $12 billion in cash and investments and continues to make shareholder returns.

Competitive Landscape: Micron’s sustained price strength in DRAM and specialty memory contrasts with weaker NAND pricing due to oversupply. However, competition intensifies, especially with Samsung’s recent Nvidia qualification of advanced HBM3E chips, which could pressure Micron’s market share and margins in HBM. Ongoing innovation and process advancements, including the 1-gamma node achieving faster mature yields, remain critical to preserving Micron’s competitive advantage in AI-driven memory markets.

Guidance and Management Commentary

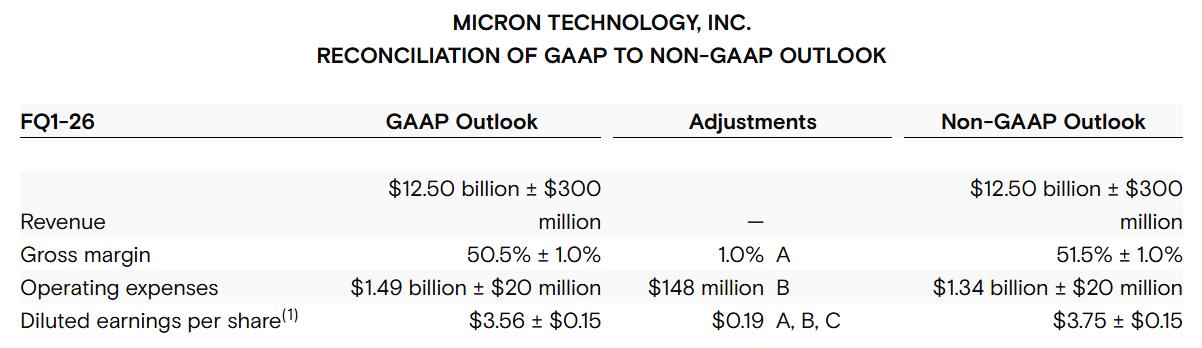

Q1 FY2026 Outlook: Micron projects Q1 FY2026 revenue of $12.5 billion ± $300 million, with gross margins near 50.5% and non-GAAP EPS around $3.75 ± $0.15, indicating confidence in ongoing AI-driven demand.

Source: Micron

Management Comments: Management expects sequential revenue growth and significantly higher free cash flow year-over-year, driven by AI infrastructure demand, positioning Micron as the sole U.S. memory maker. CFO Mark Murphy highlighted that DRAM supply constraints, including low inventories and high costs for new capacity, will support pricing. The ramp of HBM4/HBM4E products targets even higher margins by 2027. Risks include GPU shortages and export controls on China, but broad AI adoption across industries (e.g., robotics, drug design) provides strong tailwinds.

Conclusion and Outlook

Micron’s Q4 FY2025 results affirm its position as a leading U.S.-based memory supplier uniquely positioned to capitalize on AI and data center growth. Exceptional DRAM revenue growth, robust margins, and accelerating HBM adoption offset NAND softness and competitive pressures. The company’s substantial investment in advanced manufacturing nodes and expanded HBM capacity lays a solid foundation for sustained revenue and margin growth as AI workloads multiply. With HBM capacity fully booked through 2026 and expanding partnerships with key AI players like Nvidia, Micron is poised for promising revenue growth and margin expansion throughout the ongoing AI infrastructure buildout. Given these strengths, confidence remains high in Micron’s long-term growth trajectory and leadership in the trillion-dollar AI memory market.

Micron Technology Q4 FY2025 Earnings Preview: Leveraging DRAM Strength and Accelerating HBM Growth

TradingKey - Micron Technology, Inc. (NASDAQ: MU) will report Q4 FY2025 results after the market close on Tuesday, September 23, 2025, with the webcasted conference call scheduled for 4:30 PM EDT. As a leading global supplier of memory chips, including DRAM, NAND flash, and advanced memory like High Bandwidth Memory (HBM) used in AI accelerators, Micron plays a key role in fueling the growing demand from data centers powering generative AI and large language models. Shares have rallied about 90% year-to-date, driven by improving memory pricing and strong AI-driven demand.

This quarter will be a key test of Micron’s ability to sustain growth and margin expansion amid intensifying competitive pressure. Counterpoint Research data for Q2 2025 shows Micron holds about 21% of the HBM market, while SK Hynix leads with 62% and Samsung trails at 17%, down from 41% a year prior. However, Samsung’s recent technological advances and Nvidia qualification could shift market dynamics, making competition more intense.

Source: TradingKey

Market Forecast

Metric | Q4 FY2025 Forecast | Q4 FY2024 Actual | Change (YoY) |

Total Revenue | $11.1B | $7.75B | +43.2% |

Adjusted EPS | $2.87 | $1.18 | +143.2% |

DRAM Revenue | $8.69B | $5.33B | +63% |

NAND Revenue | $2.33B | $2.37B | -1.7% |

Non-GAAP Gross Margin | 44.5% | 36.5% | +8pp |

Key Investor Focus Areas

AI Infrastructure and HBM: HBM is a specialized stacked DRAM that delivers ultra-fast data access crucial for AI GPUs and accelerators, powering training and inference in models like those from Nvidia. Micron is one of the top three HBM suppliers alongside SK Hynix and Samsung. Its HBM production is sold out through 2026, with HBM revenue expected to significantly boost DRAM growth in Q4, contributing to mid-60% year-over-year gains. The ramp-up of HBM production, including next-gen HBM4 development, will be closely watched.

Supply-Demand Dynamics and Pricing: After years of excess inventory, the memory market has tightened, driving up DRAM prices and supporting Micron’s gross margins. Market participants will be keen on Micron's guidance regarding FY2026 pricing trends, bit shipments, and whether AI demand can offset cyclical softness in PCs and mobile segments.

NAND and Emerging Segments: Despite stable demand for client solid-state drives (SSDs) and growing demand for enterprise storage upgrades, NAND margins remain under pressure due to market oversupply. Looking ahead, Micron's R&D of next-generation 3D NAND technology and advancement of its emerging storage-class memory business are key to achieving sustained mid-term growth.

Backlog and Capacity Expansion: Micron's remaining performance obligations (RPO) are expected to provide it with strong revenue coverage for multiple quarters, reflecting strong market demand for its storage products. Capital expenditures for fiscal 2025 are projected at approximately $14 billion, primarily focused on advanced process nodes and expanding HBM fabrication capacity. This significant investment supports future growth as AI infrastructure buildouts continue to drive memory demand. Commentary on fab expansions in the U.S., Taiwan, and Japan, as well as utilization rates, will indicate how quickly new capacity can convert into revenue amid robust AI infrastructure buildouts.

Margins, Cash Flow, and Capital Allocation: Micron expects operating margins in the low 40% range for Q4, supported by stronger DRAM pricing and improved scale efficiencies. Capital expenditures remain elevated for fiscal 2025, primarily targeting advanced DRAM nodes and HBM fabs, which may limit free cash flow in the near term. The company continues its share repurchase program with over $7 billion authorized and maintains dividend payments, while emphasizing cost control in a competitive memory market.

Recent Events and Regulatory Trends

Guidance Raise: In August 2025, Micron raised its Q4 guidance due to stronger DRAM pricing and solid execution. This reflects strong AI-driven demand despite sensitivity to market cycles.

Competitive Pressures: Samsung’s recent clearance of Nvidia’s quality tests for advanced 12-layer HBM3E chips briefly pressured Micron’s stock, down about 3-4%. While Micron’s HBM production is qualified and ramping with key customers, this milestone highlights fierce competition among the top suppliers, which could impact pricing and market share, particularly in Nvidia’s ecosystem.

Regulatory Environment: Micron benefits from a $6.1 billion U.S. CHIPS Act grant to support domestic fab expansion. However, export controls on advanced semiconductors to China could limit certain revenue streams. Additionally, AI-related data privacy and sovereignty regulations may favor Micron’s enterprise-grade memory products in regulated sectors, although compliance adds complexity and may extend lead times.

Conclusion

Micron’s Q4 FY2025 report will be a pivotal read on memory market pricing dynamics and demand resilience, largely powered by data center and AI-related spending, offsetting competitive pressures in high-performance memory sectors like HBM. Sustained DRAM pricing improvements and solid volume growth could drive upside to consensus, while margin pressures or increased specialty memory competition warrant caution. Investors should watch guidance and management commentary closely for signs of durable industry improvements or emerging risks.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.