Zeta Global (ZETA): Solid Data Moat Can Drive Value Up

Source: TradingView

Investment Thesis

TradingKey - Simply speaking, Zeta is a marketing tech company that leverages its high-quality, proprietary data and AI tools to automate a wide range of marketing tasks, helping marketers and brands conduct campaigns on various channels. The company’s solid moat is based on its high-quality proprietary data. With an unassuming market cap of $5 billion, 22% expected growth and an expected margin of 12%, Zeta’s stock price has 60-90% potential.

Company Overview

Source: Company Presentation

The main questions every business is asking themselves is “how to find my target customer” and “how to reach customers more effectively”, and this is what marketing is for - knowing more about the consumer. In the digital era, it has become even more essential to gather customer data so marketers can create the most appropriate marketing campaign.

However, a growing number of consumers are also concerned about the amount of information marketers retain about them and how it is used. This led to legislation in recent years (GDPR, CCPA, etc.) across the globe that is meant to regulate the storage and use of consumer information.

Overall, companies and marketing agencies have to strike a very delicate balance between acquiring the best quality consumer data without breaching the data privacy regulations. Zeta can be the company that can provide the support to achieve this balance.

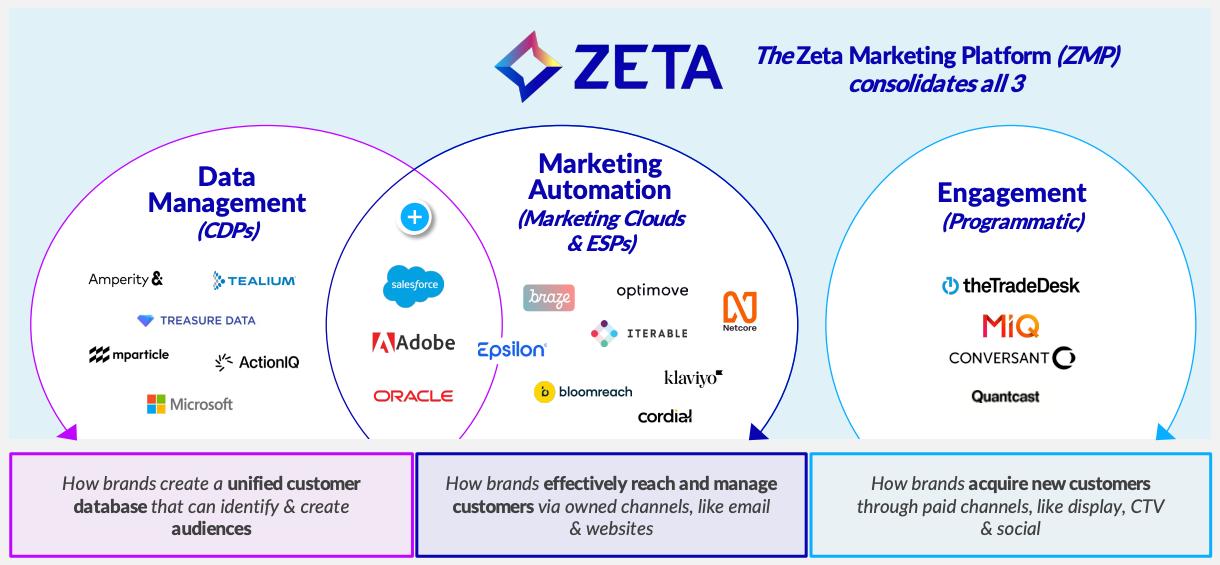

Zeta’s core technology offering, the Zeta Marketing Platform (ZMP), is an end-to-end omnichannel marketing automation platform that leverages a proprietary data set and artificial intelligence capabilities to enable enterprises to accelerate the growth of their businesses by acquiring, growing and retaining customer relationships.

With simple words, Zeta can be separated into two things: a giant pool of data plus a set of AI marketing tools. As a customer who wants to promote my own product, I can access the data for market insights, and I can use the various tools to craft a well-targeted marketing strategy and also automate some of the traditional marketing tasks such as email sending, content creation and customer engagement. Unlike other products, Zeta AI tools try to minimize the reliance on complex dashboards, making it simpler and more actionable for clients to use.

More important is the Zeta data advantage. The company owns some of the largest first-party data sets out there. Zeta allegedly has one of the richest first-party data sets, if we exclude the big tech players like Meta and Alphabet. Covering 240 million US consumers (70% of the country population) with more than 1 trillion monthly signals, including but not limited to behavior, transactions and location. The data is proprietary - they own it and it’s only theirs, which means it contains unique insights unavailable anywhere else.

First-party data is a keyword here. This is a type of information a company collects directly from its own customers, website visitors, and social media followers, through a company's own platforms like websites, mobile apps, or email correspondence. It is characterised by high accuracy, relevance, and reliability. It contrasts with third-party data, collected with cookies, which can be less reliable and bear more risk of breaching privacy data rules.

How did Zeta accumulate this vast amount of data? The company was founded in 2007, collecting data for 18 years. Zeta uses opt-in mechanisms (Zeta asks for explicit consent for data sharing), lowering the risk of being a target of data privacy regulatory crackdown. Zeta also acquires data from clients, and it has a long history of acquiring smaller data-valuable firms, enriching the company’s product even more.

Financials

Source: Bloomberg, Company Financials

Zeta generates revenue in two ways, recorded in two segments:

- Direct platform: This includes the direct provision of ZMP to customers, via subscriptions or licenses to the company’s customer data platform (CDP), marketing automation tools and analytics. The segment boasts high margins (70%+) due to lower variable costs and the ability to scale. It historically has represented 65%-75% of the total revenue, slowly increasing over the years

- Integrated platform: Providing ZMP but also executing marketing campaigns on behalf of clients. The segment has low gross margins (40%-50%) - more variable costs due to ad inventory buying and more labour-intensive campaigns. It represents the remaining 25%-35% of the total revenue

-39318b640fe54202addfc85f3b40e396.jpg)

Source: Company Reports

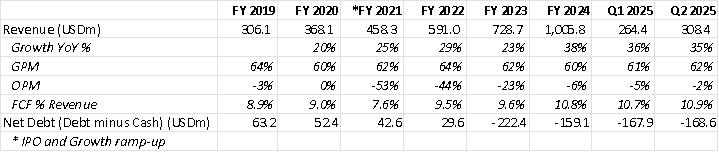

Gross Profit Margins stand at low-60s, which is lower than the majority of the SaaS firms, which can be explained by the following:

- Integrated platform segment is low-margin due to the need to buy ad inventory and run marketing campaigns;

- Costly to acquire and maintain the level of up-to-date first-party data;

- Throughout the years, Zeta has been constantly acquiring different companies, and the process of business integration often comes with increased expenses;

In terms of operating profit, the company IPO-ed in June 2021, which was accompanied by increased operating expenses and broad business ramp-up, leading to -53% OPM, but since then, the losses have been steadily narrowing, reaching close to breakeven, as we see from the table above.

In terms of cash flow and balance sheet, free-cash flow has long been positive, while net debt has been negative since 2023 (more cash than total debt, and also, the debt is from leases, not from bonds and loans).

Growth Potential

Firstly, we have industry-wide secular trends such as the shift from offline towards online marketing spending. Digital ad spend hit $300B in the US in 2024, growing 10% annually per eMarketer. Meanwhile, Zeta’s revenue for 2024 was just $1B, implying a huge room for growth. Marketing teams are increasingly evaluated on performance metrics such as ROI. Zeta can directly address this with its high-quality data and expanding AI tools. Finally, with the demise of third-party data, marketers will rely even more heavily on first-party data vendors like Zeta.

Source: Zeta Earnings Presentation

Source: Zeta Earnings Presentation

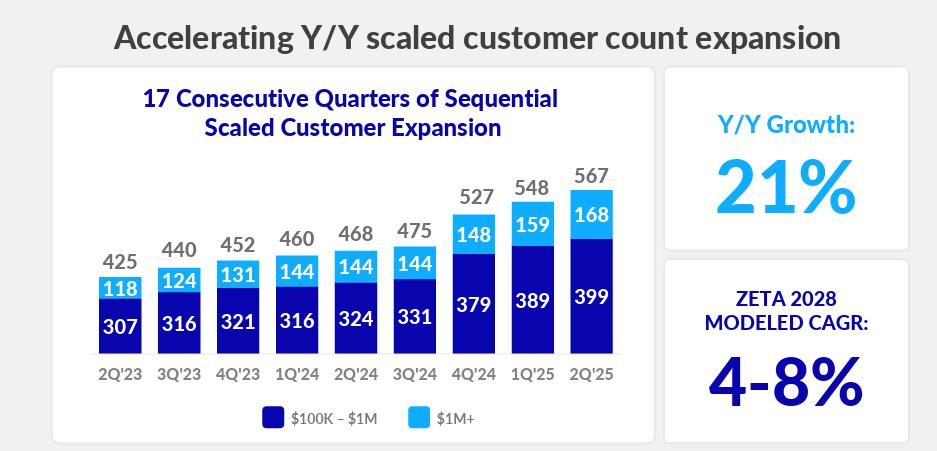

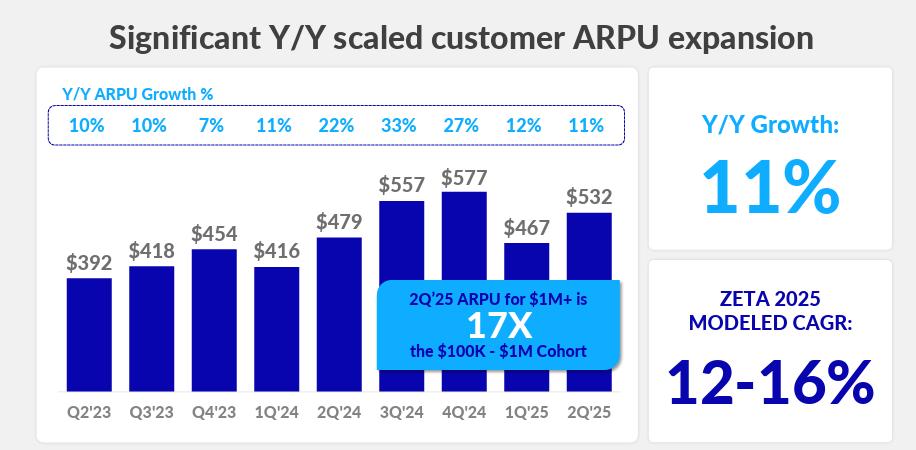

There are also company-specific growth drivers with both scaled customers ($100k-$1mln) and super-scaled customers ($1m+) growing at 20% or above. Also, growth can come from ARPU, as the high-quality, first-party data can serve as a bargaining tool for the products’ price hikes.

Currently, a large number of the clients are actually agents that work with many brands. Usually, agents are onboarded at a lower pricing, less favourable for Zeta (think about wholesalers selling large quantities at discount). However, the trend is towards more direct customers, which will allow Zeta to dictate higher pricing (margin accretive).

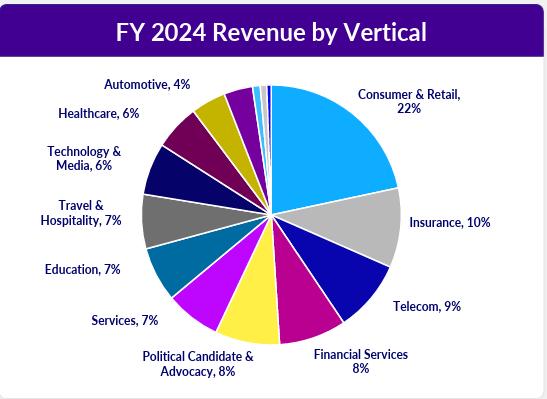

An aspect worth mentioning is the client base of Zeta being highly diversified among industries, providing a certain downside protection.

Source: Zeta Earnings Presentation

Competition

As Zeta is still not a household name, it is important to understand whether the moat is solid or not. For potential new entrants, replicating Zeta’s model is quite challenging. Accumulating Zeta’s level of data is extremely hard, unless it's one of the giant social media players. New entrants have to start from scratch, something Zeta has been building for nearly two decades. And also, at this point, the strict data privacy laws may play in favour of Zeta against potential entrants, as collecting data will become harder and harder.

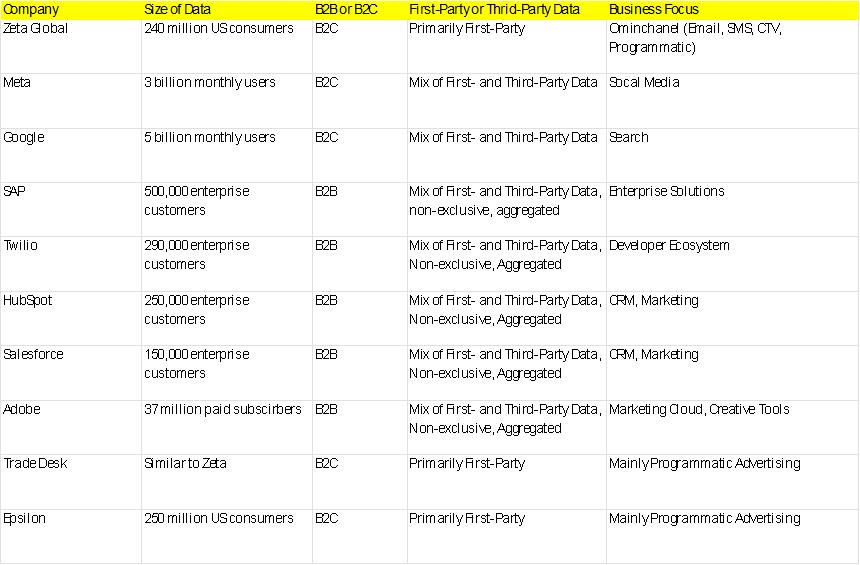

How about the current players? Meta and Google both have a much larger scale, but in terms of quality of data, Zeta is more heavily reliant on first-party data, while the other two are using a mix of first and third-party data.

Big cloud providers or ERP giants like Salesforce, SAP, Twilio, Hubspot, and Adobe have a lot of data and big budgets, but they are focusing primarily on company data suitable for B2B clients, not consumer data (B2C clients). Also, these players are more of data aggregators - data may not be exclusive or proprietary, and customers are not required to update the data regularly.

Trade Desk (TTD) and Epsilon may have similar scale and quality of consumer data to Zeta, however, they are currently more focused on inventory-type/programmatic marketing (advertising on media), while Zeta is more broad (includes this, as well as email, SMS, CTV). Trade Desk has $2.4B revenue (2024), 25% YoY growth, 95% gross margin (higher than Zeta’s 60-65% due to less reliance on managed services).

Overall, despite the different types of competitors, Zeta’s deep penetration of the US consumer, and high-quality in-time first-party data give the company a strong differentiation.

Source: Company reports

Valuation

In its investment presentation, Zeta guided a 20% CAGR in the coming years. We believe that is a rather conservative estimate because 1) the value proposition of Zeta’s data is quite strong, and 2) Zeta management has a historical tendency of providing conservative figures. Thus, a CAGR of 22% is more appropriate.

In terms of profitability, the most direct competitor, Trade Desk (TTD), has a profit margin of 16%, thus, assigning a target margin of 12% for Zeta in 2028 appears to be reasonable.

With these assumptions in mind, Zeta is traded at 18x times 2028 expected earnings, which is quite low for a SaaS player. With typical SaaS PE multiples ranging between 30x and 35x, a target price for Zeta is $33.00 to $39.00.

From another perspective, Zeta has a market cap of $4.9bn, compared to close peers of Trade Desk and HubSpot, which are above $20 billion of market cap, despite Zeta possessing as rich and perhaps even better-quality data than them.

Risks

Competition: Despite Zeta’s unique positioning on the consumer-data landscape, they are not the only one that collects first-party data. We saw from the previous section how other peers like Trade Desk and Epsilon have very similar business models, and despite their more narrow scope, they may pursue more of an omni-channel strategy, just as Zeta does.

Regulatory changes: Controlling the direction of the regulatory framework is beyond Zeta’s ability, and even though the first-party data they have is considered less risky, any dramatic changes in the data collection policies will reflect on the company. Previously, Zeta was accused by a short seller of using fake websites to collect data, and even though the claims were rebutted by the auditors, investors should have this risk in mind.

Zeta may lag in AI: We defined Zeta’s model as simply database+AI tools. As Zeta is still relatively small in terms of scale and resources, the AI tools used for marketing automation may actually be easily replicated and outdone by larger, more AI-savvy competitors, which may harm Zeta’s business in the long run.

Economy and election cyclicality: The ad spending is prone to economic cycles, and the current complex economic picture in America may discourage marketers and brands from spending.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.