Uranium Energy Corp. (UEC) Earnings Comment: Here Comes the Uranium!

_croped_889x500 (1)-666c3deec8f74a1d91bccfc0edb42909.jpg)

Uranium Energy Corp. (UEC) Earnings Comment: Here Comes the Uranium!

TradingKey - Uranium Energy Corp. reported fourth-quarter and full-year earnings on the 24th of September, before the opening bell. The market reaction was rather muted, with the stock dropping just 1% the day after the earnings release.

Financial Highlights

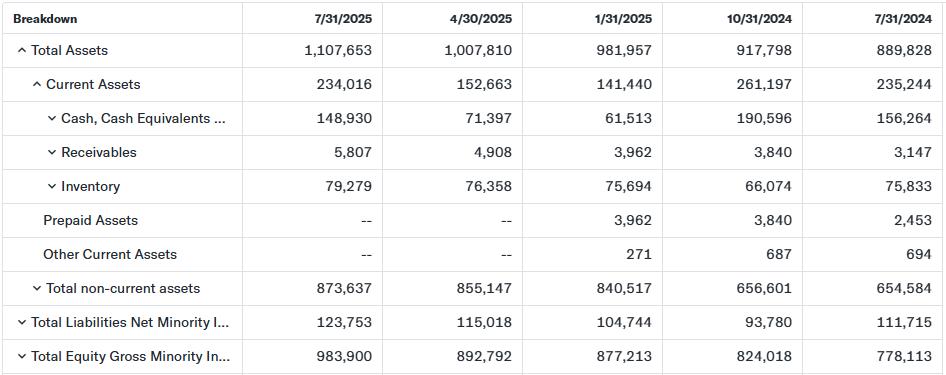

As we see from the financial summary above, the company delivered both revenue and EPS misses. However, this is not very meaningful for the current investment story of UEC at the moment, as the market acknowledges that UEC is still in a transitional period where the company is in an exploration stage, and it will take some time to see a full production capacity.

What’s worth taking a look at is the balance sheet. We do see a ramp-up in the cash position in Q4, with the current cash balance standing at nearly $150 million, compared with $71 million in the previous quarter. Inventory also remained stable at nearly $80 million. All this, without a significant increase in debt.

Source: Yahoo Finance

The healthy balance sheet gives UEC significant flexibility in pursuing further debt financing if needed. Also, the management mentioned ongoing discussions with various US government entities for potential grants and low-interest loans.

Operational Highlights

In Q4, UEC ramped up production at its Wyoming in-situ recovery mine. The company also completed an acquisition of the Sweetwater Complex.

The exact poundage of the Q4 production has not been disclosed, but the costs at this stage of limited production came in at $36.41 per pound, including cash costs of $27.63 per pound (if we exclude non-cash expenses like depreciation). These numbers are within the industry norms and well below the current ~$80 per pound spot price. We expect the costs per pound to go down with the increase in production, due to economies of scale.

In terms of the recent and near-term milestones, UEC formed a subsidiary called United States Uranium Refining & Conversion Corp, which will be focused on refining, implying that the company is pursuing an integrated strategy, beyond just production.

In addition, the Burke Hollow project located in Texas is 90% ready to start production (expectedly in December).

Management Outlook

The management of UEC reiterated their bullish view on Uranium, as the commodity is driven by all the tailwinds related to AI-driven demand, constrained supply (Kazakhstan production problems and Russia export restrictions) and favorable regulatory environment.

The good thing for UEC is that even if there is a downward pressure on Uranium prices, the low-cost production protects their expected profitability.

Conclusion and Risks

Q4 and the whole fiscal year 2025 are a transitional time for Uranium Energy Corp, with the real showdown expected to unfold in the coming quarters. The expectations for them are high, hence the stock rally. However, whether this rally is justified, we will find out very soon.

There are risks associated with UEC, such as 1) concerns over stock price overvaluation; 2) production of Uranium not being able to scale; and 3) potential equity financing that can dilute the current shareholders.

Uranium Energy Corp. (UEC) Earnings Preview: Is there any Uranium out there?

TradingKey - Uranium Energy Corp (UEC) will report fourth-quarter and full-year earnings on the 24th of September, before the opening bell. The company’s stock price has been performing very strongly, being up 61% on a year-to-date basis - a rally closely related to uranium as a commodity.

Uranium spot prices have been on the run in recent months, reaching $76/lb from this year’s bottom of $64/lb in March. The surge in the spot price is a result of a disbalance between demand and supply:

- The demand for nuclear energy is surging both due to efforts to meet the targets for low-carbon emissions and also further support the growing energy hunger of AI companies.

- Suppressed supply levels coming from Kazakhstan (a leading uranium exporting country) due to sulfuric acid shortages and delays of projects. Also, after the Fukushima accident (2011), the public perception towards nuclear energy across the world deteriorated significantly, which led to the closure of many Uranium mines.

- We should also not forget the regulatory blessing from Trump’s administration, which expedited reactor approvals in the country.

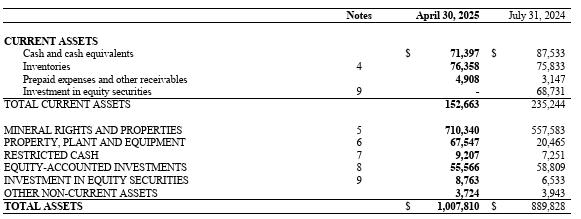

UEC is expected to report a revenue of $8.5million and a loss per share of $0.04. These financial metrics are largely symbolic and not in the investors’ focus. In fact, oftentimes the company does not generate any revenue, simply because UEC is in an exploration stage and has not yet established proven reserves. In other words, they produce little to no uranium as of now, as they are still exploring. As we can see from the table below, the majority of their assets are under “Mineral Rights and Properties”, which only stands for the right to explore, and it is an unproven reserve, recorded at a cost of acquisition, not at a real value.

Source: UEC Filings

The large majority of their uranium inventory that they currently possess is from purchases. UEC sells its inventory when the prices are high (technically, where the majority of the $8.5 million revenue comes from), acting more as a commodity trader than a full-scale producer. UEC does not have other business lines, but it operates assets in Texas, Wyoming and Saskatchewan (Canada). However, with time, the company is expected to ramp up production and revenue, primarily due to the spot price tailwinds mentioned just now.

UEC generates profit from royalties and equity stakes in other firms, however, this is not revenue, but a non-operating profit, recorded at the bottom of the income statement.

So what should investors look for in this quarter’s earnings?

- Any updates on the exploration and production activities in their key assets in the US and Canada would bring more clarity on where UEC is currently standing. This also includes any potential changes in the resource estimates and the time needed for transitioning to a full-production mode.

- The company is in a cash-burning mode, so will there be any further financing? Even without revenue, investors will closely examine the costs’ structure, the cash balance on the balance sheet, and any major cash flows. The management may discuss any potential financing options, such as debt financing or equity offering. Earlier this year, we saw the US government and Apple invest in MP Materials, which demonstrated the significant role of certain mining companies in the broad American economy. It is possible to see a similar scenario with UEC.

- What is the management outlook on macro factors such as nuclear energy, uranium supply, supply chains? As the company’s performance is very much tied to the price of Uranium, we would love to see the management perspective on these macro processes – uranium demand drivers, and supply chain challenges.

Conclusion and Risks

The company is still in the exploration stage, making the current financial metrics less relevant at this stage. However, progress in discovering any proven uranium reserves will be the centerpiece of the earnings call, combined with an outlook for the prospective Uranium demand globally.

The major risk for UEC is whether these rights to explore would actually materialize into proven reserves. Also, as a mining business, UEC is prone to production delays, hiccups and price volatility caused by geopolitical or supply chain issues.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.