AI’s Next Battlefield: Broadcom’s TPU-Backed ASICs Challenge Nvidia’s GPU Dominance

Executive Summary

TradingKey - Broadcom (NASDAQ: AVGO) recently secured a landmark $10 billion deal with OpenAI to supply custom AI accelerators, solidifying its leadership in the booming AI semiconductor market. Alongside its longstanding Google TPU partnership, this positions Broadcom to capture significant growth in the AI custom silicon market. In Q3 FY2025, Broadcom reported $15.95 billion in revenue, with AI-related sales up 63%. The company maintains a strong balance sheet, robust profits, and impressive free cash flow.

Broadcom is expected to grow its revenue rapidly, driven by increased shipments of Google’s TPU chips and rising demand for AI products. Based on projected EPS of $9 in FY2026 and a forward PE of 40 to 45x, the stock’s target price is estimated to be between $360 and $400. This reflects Broadcom’s strong technology, diverse product lineup, and steady leadership under CEO Hock Tan.

Source: TradingKey

Company Introduction and Business Overview

Broadcom Inc. is a global semiconductor powerhouse headquartered in California, well-known for its wide range portfolio spanning semiconductor products and infrastructure software. Established in 1961, it has evolved through strategic acquisitions and innovations to penetrate various critical sectors including data center infrastructure, networking, broadband, wireless communication, and storage segments.

Source: Broadcom

The company’s Semiconductor Solutions segment, the heart of its operations, caters especially to high-growth markets such as hyperscale data centers, cloud infrastructure, and the rollout of 5G networks. Broadcom’s advantage lies in its extensive product range, strong relations with hyperscale customers like Google, and its sophisticated supply chain, which includes tightly integrated relationships with major foundries such as TSMC.

This deep integration across products and customers has allowed Broadcom to ride the wave of AI-driven demand, particularly for accelerated compute and high-speed networking capabilities, becoming an indispensable supplier in the AI semiconductor ecosystem.

Broadcom and Google Partnership

A significant pillar of Broadcom’s growth is its longtime partnership with Google centered around the development and manufacture of Google’s Tensor Processing Units (TPUs). These TPUs are custom ASICs finely tuned for AI workloads, covering multiple generations built on state-of-the-art 3nm process technology.

Financially, this partnership is a cornerstone for Broadcom, with AI revenue from Google’s TPU program expected to surpass $10 billion (~15% of total revenue) in 2025. This surge is propelled by the insatiable demand for AI acceleration fueling Google’s data centers worldwide, which processes massive neural networks and large language models. These TPUs enable efficient AI inference and training, enhancing Google’s AI capabilities while offering integration and cost efficiencies compared to off-the-shelf GPU solutions.

However, despite their critical role, Broadcom’s ASICs generally lag behind leading AI GPUs like NVIDIA’s H200 in raw throughput and computational efficiency.

In recent developments, Google has sought to diversify its TPU supply by partnering with Taiwan’s MediaTek for upcoming TPU iterations, particularly to handle I/O modules and peripheral functions. This strategy helps spread supply chain risks and reduce costs. While MediaTek focuses on producing high-volume, less complex components, Broadcom remains central to Google’s TPU ecosystem due to its expertise in designing and manufacturing the high-tech, complex ASIC cores. This complementary partnership balances scalability with technical sophistication, maintaining Broadcom’s pivotal role alongside MediaTek’s production strength.

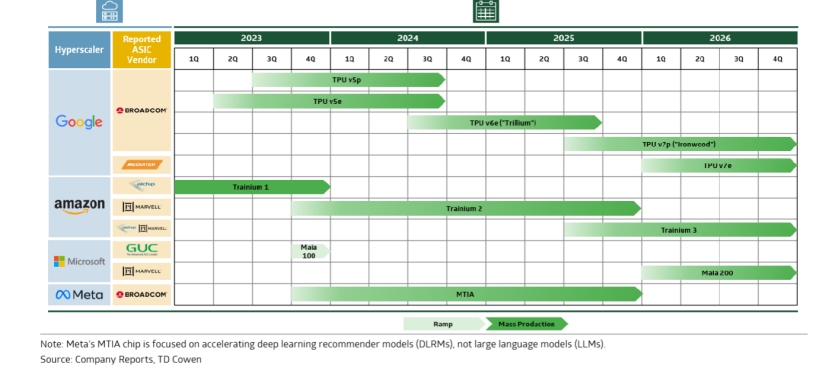

The chart below provides an illustrative timeline of Google TPUs development milestones.

Source: TD Cowen

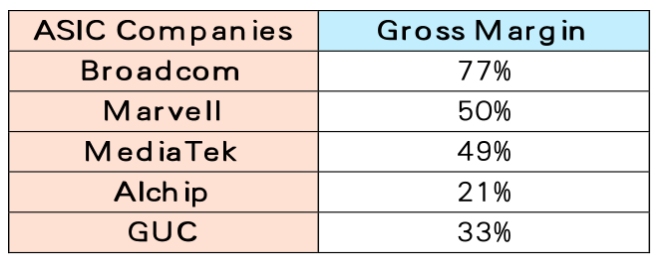

Yet, this evolving landscape presents a clear challenge as hyperscale operators increasingly push to lower ASIC vendor margins to maximize their own investment returns. This is driven by the need to compensate for any performance gaps compared to versatile general-purpose GPUs, which puts significant downward pressure on prices. Despite these headwinds, Broadcom is well-positioned with greater bargaining power over margins relative to many other ASIC suppliers, thanks to its advanced technology, scale, and deep customer relationships. This advantage should help Broadcom navigate margin pressures while sustaining its leadership in the custom AI silicon market.

Source: Broadcom, Marvell, MediaTek, Alchip, GUC Financial Statements

ASIC Versus GPU

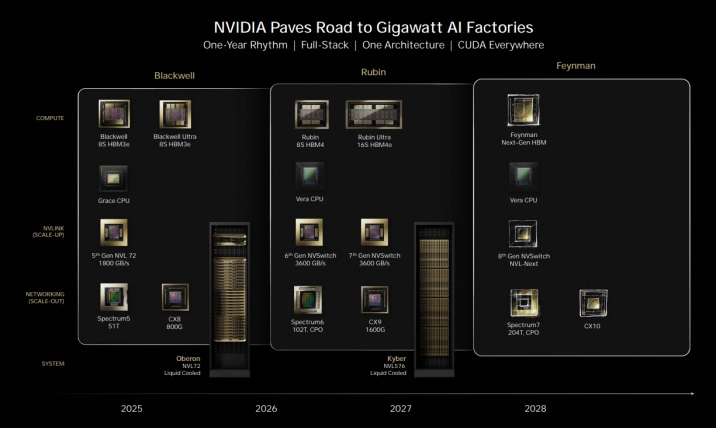

The lines between ASICs and GPUs in AI acceleration are increasingly blurred. Modern data center GPUs have evolved far beyond their original role as general-purpose graphics processors and are now highly specialized ASIC-like chips designed specifically for demanding AI workloads. A prime example is Nvidia’s Rubin CPX GPU, purpose-built to handle massive-context AI inference, such as million-token software coding and generative video applications. Rubin can perform up to 30 petaflops of computing power using a specialized low-precision floating-point format optimized for AI tasks. This high compute capability allows Rubin to handle complex AI inference and training workloads very efficiently.

This innovation broadens the competitive landscape: Nvidia is not just a GPU merchant but also a formidable ASIC designer. Rubin architecture demonstrates that GPUs can be highly application-specific, further dissolving the traditional binary between ASIC and GPU. For companies like Broadcom, this convergence means that they compete not only against other custom ASIC vendors but also against Nvidia’s cutting-edge GPU platforms that incorporate ASIC-like specialized hardware, such as tensor cores optimized for matrix multiplication, the core mathematical operation in deep learning models.

Source: Nvidia

GPUs usually provide a better return on investment because they offer higher performance, have well-developed software support, and can be used in many places. Custom ASICs, including those created with Broadcom, can also be profitable with returns around 20% when used at a large scale. However, for these custom chips to be worthwhile, they need to perform at least half as well as the best GPUs. If their performance is much lower, it becomes hard to justify using them for big projects.

This competitive dynamic put considerable pressure on ASIC vendors to innovate rapidly and ensure cost-efficient designs, while also juggling evolving margin pressures from hyperscale customers who seek the best trade-off between cost, performance, and flexibility.

Financial Performance

Broadcom’s Q3 FY2025 results reflect strong growth driven by AI semiconductor demand. The company reported total revenue of $15.95 billion, a 22% increase YoY. The Semiconductor Solutions segment, which includes ASICs and AI chips, grew 26% to $9.2 billion (~58% of total revenue), while AI-specific revenues surged 63% to $5.2 billion, marking ten consecutive quarters of steady growth. Infrastructure software revenue also contributed $6.8 billion, up 17% YoY.

-9e1b6ce6985645e28053efe16502227c.jpg)

Note: The drastic Infrastructure Software revenue growth in 2024 comes from acquisition of VMware.

Source: Broadcom, TradingKey

Margins dipped slightly in Q3 FY2025 due to a shift in product mix toward higher volumes of lower-margin AI accelerators (XPUs) and wireless products, as well as continued softness in non-AI semiconductor segments. This mix dilution temporarily pressured profits despite robust revenue growth from AI and software segments. Broadcom expects margins to partially recover in Q4 as product mix stabilizes.

-f72f5c044218407c9b55c074c43a5b89.jpg)

Source: Broadcom, TradingKey

GAAP EPS is $0.85, a significant recovery from previous losses. Broadcom generated $7 billion in free cash flow, representing 44% of revenue, supporting its strong capital return strategy through dividends and share repurchases.

-28803e876cfb42379896c9bdf7b8f529.jpg)

Source: Broadcom, TradingKey

From a balance sheet perspective, Broadcom maintains moderate leverage with total debt standing near $64 billion and a debt-to-equity ratio close to 0.9. The company’s interest coverage ratio of 7.5 remains strong, indicating ample earnings to cover debt interest obligations.

-0a12179210cf46e2aa5009093fdef94c.jpg)

Source: Broadcom, TradingKey

Broadcom's inventory has been building up slightly. As of Q3 FY2025, inventory stood at approximately $2.18 billion, up about 8% sequentially from Q2, reflecting preparation for expected revenue growth in the next quarter. Despite this increase, days of inventory on hand slightly improved to 52 days, indicating controlled inventory management amid growing demand.

-6b202b80fa2b460783069e8732b8162c.jpg)

Source: Broadcom, TradingKey

Looking ahead, Broadcom forecasts AI semiconductor revenue to accelerate further to $6.2 billion in Q4 FY2025, reinforcing its position as a core engine of growth amid cloud infrastructure expansion. Despite some pressures in non-AI segments, the company’s diverse portfolio and financial strength position it well for sustained momentum.

CEO Hock Tan, who plans to lead Broadcom through 2030, has a compensation package tied to the company’s AI revenue growth. He was granted performance stock units (PSUs) that vest only if Broadcom hits specific AI revenue targets between fiscal 2028 and 2030, and if he remains with the company during this period. This structure aligns Tan’s rewards directly with aggressive AI growth, reflecting the board’s belief that AI-related sales are central to Broadcom’s future success.

Source: Broadcom

Strategic Outlook and Valuation

Broadcom is well positioned to capitalize on the growing ASIC chip market, expected to reach about $50 billion by 2030 according to Grand View Research, making up roughly 15% of the broader accelerator market.

Thanks to its strong multi-year contracts and advanced technology, Broadcom is set to capture a significant share of this growth. Its comprehensive IP, manufacturing strength, and wide customer base create strong barriers against competitors like MediaTek.

Broadcom is expected to grow its revenue at a high single-digit CAGR in the coming years, driven by continued TPU ramps and rising AI infrastructure demand. Considering stable margin assumptions and growing AI exposure, a forward P/E around 40-45x on a consensus FY2026 EPS of $9 supports a target price range of $360-400. This reflects a moderately aggressive view on sustained growth, robust free cash flow, technological leadership, and structural expansion in AI semiconductor solutions.

-24e47cf298934762bbe7aa3ad153994e.jpg)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.