Duolingo (DUOL): Can the Green Bird Fly High Again

Source: TradingView

Investment Thesis

TradingKey - Duolingo is a great business, despite the stock price being down nearly 50% from its peak less than four months ago. However, the question is whether it’s worth buying it at a market cap of $12.5 billion. The answer is “not yet” because the traffic, even though healthy, will not grow at the levels seen before at 30-50%. Also, we do expect the competition (Google or OpenAI) to steal some growth for them as well. However, the AI will not be the end of DUOL, as they have the ability to adapt and protect their market share for the years to come. Right now, the stock is trading at 25x the expected 2030 earnings, but 20x will be more of a triggering point for buying.

App Overview

Duolingo is a leading mobile-first learning platform, providing its users and subscribers access to gamified learning courses in 40+ languages, math and music. The official mascot and symbol of Duolingo is the green owl called Duo, which often reminds users to use the app daily with witty and humorous remarks.

Gamification is the main aspect of the app. Users can collect experience points (XP), hearts/lives, gems, can go on quests and challenges, and there is also a leaderboard for achievements and performance tracking.

Duolingo operates a traditional freemium model with free-of-charge features and also three paid tiers catering to various needs:

Freemium Model: Users can access the lessons for free, allowing easy customer acquisition.

Paid Tiers: Currently, there are three paid tiers, which free customers can upgrade to:

- Duolingo Plus/Super: ad-free experience, unlimited hearts, extra lessons

- Duolingo Family Plan: up to six users sharing a single subscription with the perks of plus/super

- Duolingo Max: AI-powered functions like roleplay (AI-driven conversation practice) and Explain My Answer (detailed feedback)

Operating and Financial Metrics

Source: Bloomberg, Company Reports

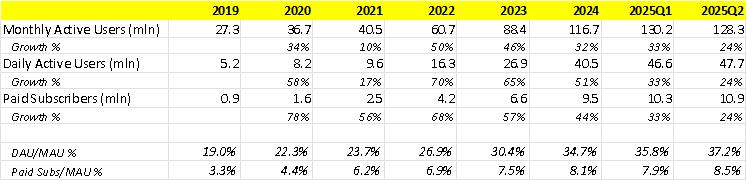

The operating metrics of Duolingo look impressive, at least. Within less than seven years, the MAU increased more than four times, the DAU – more than 9 times and the paying users - more than 12 times. Not only that, two important ratios paint an even more impressive picture:

- DAU/MAU ratio almost doubled, implying that DUOL has a strong ability not just to persuade people to download the app, but also to use it regularly

- Paid users/MAU ratio has also improved significantly over the years – a sign of a strong funnel towards monetization

Duolingo is among the apps with the highest DAU/MAU out there, better than X, Hinge, Tinder and ChatGPT.

-1fbc9b4da37046dc84c8373b5c5dd17f.jpg)

Source: Citigroup

This dynamic growth in user acquisition and engagement is reflected in the top line growth as well, which can be seen throughout the years:

![]()

Source: Bloomberg, Company Reports

Duolingo generates revenue mainly through its subscription offerings (~80% of revenue) & monetizes via advertising, its online English proficiency assessment exam (Duolingo English Test), & in-app purchases (IAPs).

Duolingo is a global company, with ~55% of revenue coming from customers located outside of the US. The US represented 46% & 45% of revenue in 2022 & 2023. The UK is DUOL’s second largest revenue market, contributing 9% & 8% of revenue.

The gross profit margin is rather stable at around 70%, mostly because DUOL has to pay a fixed percentage commission to Apple and Google for their store distribution.

On an operating level, DUOL is already profitable with current OP margins at around 13% as of 2Q2025. It is worth noting that, unlike other app companies that mostly spend on marketing, DUOL’s biggest operating expense is actually R&D (30% of the total revenue), and this can be viewed positively, as it shows a certain dedication to improve the overall quality of the product and its AI capabilities. Marketing expenses are just 12% of the revenue, as users join the app mostly organically. Also, the company is quite efficient with its marketing budget – doing promotions only during the start of the school year and New Year (as many people wish to learn a new language as a new year resolution).

Free Cash flow as a percentage of revenue is also strong, standing at 35%-45%. The fact that capex represents less than 3% of the revenue is a major contributor to this.

The balance sheet is also strong with over $1 billion of cash and equivalents and no interest-bearing debt.

Growth Opportunities

Similar to other successful tech companies, Duolingo tries to disrupt an industry that has mostly been online. It is estimated that around 1.5-2 billion people globally are learning languages, and the majority of language learning is still done in an offline setting. There have been efforts to digitalize the education system, but there is still a way to go. Currently, 128mn MAU is a significant user base (5-8%) penetration. Even though we do not expect 1.5 billion people to be playing this app, we do see this TAM fueling a growth of above 10% in the coming years.

Additionally, penetration will come from paid users as a percentage of total monthly users, as shown in the table above. So far, this number is around 8% but it can further go up. For instance, Tinder paying users represent around 15%, and people are willing to pay for education.

Furthermore, the AI-driven Duolingo Max is accretive to the overall monetization and revenue per user, as just 8% of the paying users are subscribed to this plan.

Apart from the subscription revenue, we have advertising, DET and IAP.

DUOL should not meaningfully ramp its ad load over time as they try to optimize the user experience and target deeper engagement and retention, However, DUOL will likely optimize its advertising capabilities to aim at users who are less likely to convert to paid subs.

IAPs are a bigger opportunity than ads over time, given that Duolingo will likely limit ad load to preserve the freemium experience.

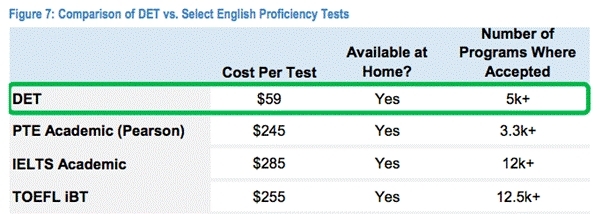

Duolingo English Test (DET) needs special attention here. An increasing number of schools are adopting DET, including elite institutions like Yale, UC Berkley, UPenn, NYU, and the penetration is still less than half of what IELTS and TOEFL have (5k for DET vs 12k for IELTS and TOEFL). DET is also way more cost-efficient, allowing the exam to grow further in popularity. Even though this may not be the main revenue driver in the future, DET provides a level of credibility and business moat to the company.

Source: Company Data

Competition as the Main Drag on the Stock Performance

As mentioned in the beginning, the stock dropped almost 50% in the last four months. There are a few reasons behind this, but the competition is the most urgent one. Google and OpenAI already have several initiatives in EdTech. We won’t dig too much into their respective products, but we would like to summarize the potential points that make these two AI giants a very serious threat:

· Unmatched AI capabilities: It is not really necessary to note how Google or OpenAI have superior capabilities when it comes to AI; thus, the edtech products they could offer would easily outpace Duolingo’s. Not only that, but Google can also afford to provide language tools absolutely free of charge, because of their scale and their cash flow/profitability comes from other businesses.

· Size and distribution channels: Google, with its vast scale, can easily penetrate educational institutions, providing its products to schools, hindering the recent Duolingo efforts to do so.

· Duolingo still depends on the Google app store: It is an extremely vulnerable situation when your competitor is also your vital distributor. If Google has an edtech app replicating Duolingo, they may prioritize it on the Google app store.

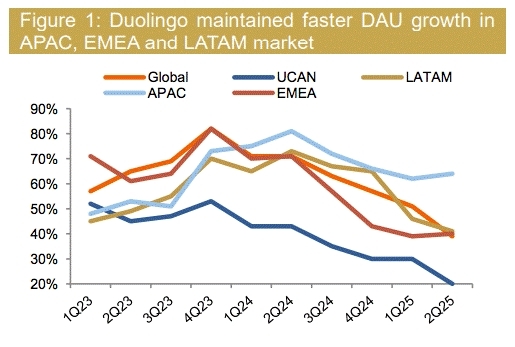

Another concern for investors is the maturing growth of traffic, as almost all geographies are exhibiting obvious growth slowdown (except APAC). Some may explain this with the rule of large numbers (as the size got bigger, it would be much harder to maintain a high percentage of growth). However, in Q2 the company’s MAU went down a bit, and the DAU increased by just 1 million sequentially.

Source: China Merchant Securities

But are the Risks Overestimated?

This is not the first time we have seen DUOL being sold off due to AI fears. What DUOL bears are missing in the whole picture is the fact that DUOL has already created a certain moat and mind share with its entertaining gamified approach.

The main value of DUOL is not to teach the language fluently, but to make the whole learning process fun and easier to digest. Thus, Duolingo’s core audience is casual learners, beginners, and younger users—values accessibility and fun over deep fluency, which aligns perfectly with its gamified, bite-sized approach.

It is true that it’s not the strongest moat out there, but it still exists.

Valuation

Currently, the stock is traded at roughly 50x the expected 2026 earnings, which is still not cheap, despite the major stock drop in recent months, and it is better to wait a bit longer for the price to drop further.

Even if we assume the revenue growing at high-teens percentage per year and profit margins reaching towards 20% (something closer to a subscription giant like Netflix), the 2030 expected net profit will be around half a billion, or a PE of 25 times the profit that year, also not so attractive.

We believe Duolingo has the ability to fend off the competition from Google and also expand into new businesses (tests, non-language subjects), however, valuation-wise, it is not yet in an attractive territory, and if it drops further, it will be great.

Ideally, we would love to see a valuation of 20x 2030E earnings or around $200 USD per share.

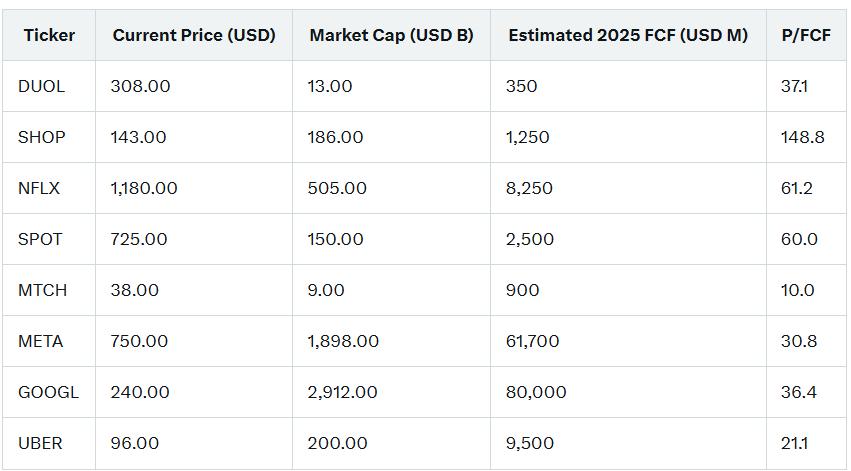

In terms of P/FCF, DUOL is traded at a comparatively reasonable level of 37x, much lower than SHOP, NFLX or SPOT, but higher than Mag 7 or Match Group.

Source: Yahoo Finance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.