Markets Bet on September Fed Cut: What's Next for U.S. Stocks?

TradingKey - US Stocks hit fresh record highs this week, just one day after a key inflation report showed that price growth is continuing to cool. CFRA’s Sam Stovall noted that markets have entered a full-blown relief mode in response to the “not-so-bad” CPI print.

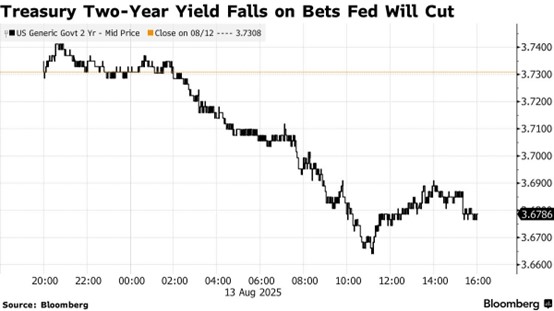

U.S. Treasury yields moved lower alongside equity gains. The 10-year yield dropped 5.62bps to 4.23%, and the 2-year fell 5.63bps to 3.67%, keeping the yield curve inversion (2s-10s) steady at 56bps.

What’s the Fed Thinking?

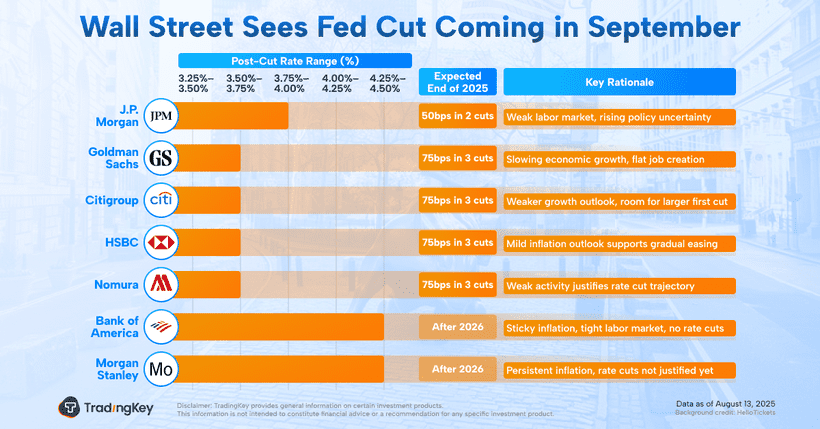

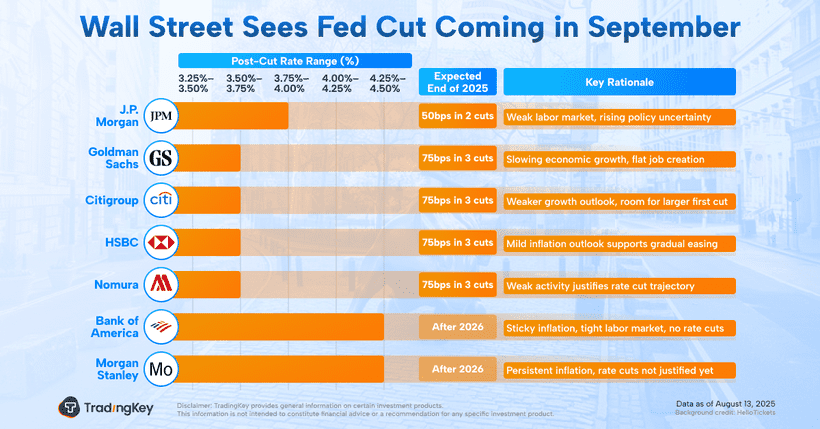

Markets briefly priced in a full 100% chance of a Federal Reserve rate cut in September following the CPI release. Softening labor data this summer has only sharpened expectations that the Fed will step in to ease.

But so far, Fed officials aren’t biting. Four different policymakers spoke this week — and none of them endorsed a cut. Their cautious tone reflects the internal debate at the Fed: do they stay on pause or open the door to cuts next month? So far, no one’s making promises.

Next week’s Jackson Hole symposium will be a key moment to watch. Chair Jerome Powell may use it to recalibrate expectations and avoid letting markets assume a cut is in the bag. He’s said repeatedly that there’s “no preset path” and that policy decisions will depend on the data.

While headline inflation in July came in softer than expected, core inflation is still persistently high — up 3.1% year-over-year, the fastest pace since February. Economists are also watching how sharply rising tariffs could feed into prices. Since February, the Trump administration has rolled out broad-based import duties, yet so far, consumers haven’t felt much pain. Falling gas prices have helped ease the squeeze too.

According to Goldman Sachs’ Elsie Peng, companies are likely to pass about 67% of those additional costs on to consumers eventually — although many are delaying price hikes with inventory stockpiles and hedged orders.

Thursday’s PPI report may have thrown some cold water on the recent rate-cut optimism. Producer prices jumped 0.9% month-over-month — well above expectations of 0.2% and June’s flat reading — marking the biggest increase since June 2022. Rising tariffs are adding to cost pressures for businesses; while some importers are currently absorbing the hit, the risk remains that these costs will eventually be passed on to consumers, potentially pushing future consumer inflation higher.

Whether or not the Fed actually makes a move in September could hinge on August's jobs report and the final inflation print before the meeting.

Bessent Wants an Aggressive Cut — But Markets Aren’t Convinced

U.S. Treasury Secretary Bessent added fuel to the debate this week, saying the Fed should cut rates by 50bps in September due to weaker jobs data. "Rates are too constrictive...We should probably be 150 to 175 basis points lower,” he said.

But investors aren’t buying it. "The more aggressive path laid out by Secretary Bessent isn't the baseline for markets," said Gennadiy Goldberg, TD Securities head of U.S. rates strategy, noting the Treasury would want to finance U.S. debt at the most advantageous levels as possible.

Fund managers are skeptical too. Daniel Siluk, Head of Global Short Duration and Liquidity at Janus Henderson, cautioned that a 50-basis-point rate cut could rattle markets, noting that the current macroeconomic environment differs significantly from last year. While the Fed previously held its policy rate as high as 5.5%, it has already lowered rates by 100 basis points in 2024, maintaining a target range of 4.25% to 4.5% throughout the year. At the same time, a surge in tariffs has introduced additional inflationary pressures that the central bank cannot ignore.

How Much Further Can U.S. Stocks Run?

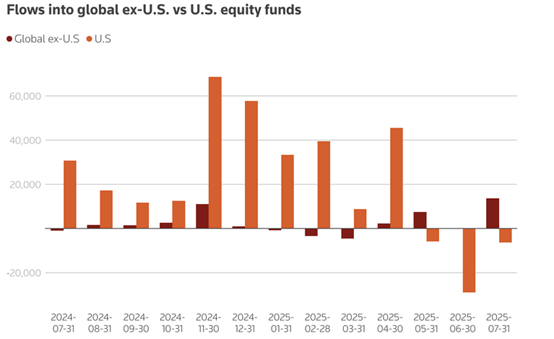

Even with all-time highs being set, a good chunk of investors are getting more cautious under the hood. Data from LSEG Lipper shows that global (non-US) equity funds attracted a 13.6billion net inflow in July—the strongest in over two years. Meanwhile, U.S.−focused equity funds saw 6.3 billion in outflows, their third month in a row of redemptions.

Part of the shift is political. Since the beginning of 2025, the Trump administration has doubled down on protectionist economic policy — slapping new tariffs on foreign goods and reigniting global trade tensions. "Liberation Day" duties, unpredictable negotiations, and rising friction with trade partners are all adding to market nerves.

Shelton Capital Management CIO Derek Izuel pointed out that the positive impact of tariff de-escalation seen in Q2 may fade, with unresolved trade talks and upcoming policy deadlines in Q3 adding to investor concerns. He cautioned that if macro uncertainty persists — coupled with narrowing growth advantages or a still-hawkish Fed — outflows from U.S. stocks could resume.

Global investors are rotating toward diversification again — especially into Europe and emerging markets. Cheaper valuations, dovish central banks, and better growth stories are drawing fresh inflows.

The forward 12-month price-to-earnings ratio of the MSCI U.S. index stood at 22.6, much higher than MSCI Asia's 14.4, MSCI Europe's 14.2 and MSCI World's 19.7.

Here Are the ETF to Watch

Vanguard FTSE Emerging Markets ETF(VWO) : Low-cost, broad-based fund suitable for long-term EM exposure

iShares MSCI Emerging Markets ETF(EEM) : Liquid and widely used EM gateway for institutional and retail investors

iShares Core MSCI Emerging Markets ETF(IEMG) : Broad EM exposure covering large/small caps and China A-shares

KraneShares CSI China Internet ETF(KWEB) : Focused on China internet leaders like Tencent, Alibaba, JD.com

KraneShares Hang Seng TECH Index ETF(KTEC) : Tracks China’s top tech innovators

Global X MSCI Argentina ETF(ARGT) : Reflects Argentina’s transformation story

iShares MSCI China Small-Cap ETF(ECNS) : High-growth Chinese small caps

iShares Emerging Markets Equity Factor ETF(EMGF) : Multi-factor strategy for balanced EM equity exposure

WisdomTree China ex-State-Owned Enterprises Fund(CXSE) : Excludes SOEs, focuses on China’s private-sector growth

KraneShares Emerging Markets Consumer Technology Index ETF(KEMQ) : Exposure to EM e-commerce and tech mix

SPDR EURO STOXX 50 ETF(FEZ) : Tracks 50 blue-chip companies in the Eurozone; core EU exposure

iShares MSCI Eurozone ETF(EZU) : Broad Eurozone equity exposure; includes France, Germany, etc.

WisdomTree Europe Hedged Equity Fund(HEDJ) : Hedged against euro weakness; plays European equities with FX protection

iShares Core MSCI Europe ETF(IEUR) : Covers developed Europe broadly, including UK and continental markets

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.