Palo Alto Networks Smashes Q4 Estimates, Riding AI and Platform Momentum

Palo Alto Q4 FY2025 Earnings Comment

TradingKey - Palo Alto Networks (NASDAQ: PANW) reported strong Q4 FY2025 revenue growth, driven by AI-enhanced cybersecurity and platform expansion. It beat revenue expectations and grew subscription revenue, though margins were pressured by investments in software and cloud efforts. Surpassing a $10 billion revenue run-rate and raising FY2026 guidance lifted confidence, pushing the stock up about 5% in after-hours trading.

Source: TradingKey

Key Financial Results

Metric | Q4 FY2025 | Q4 FY2024 | Beat/Miss | Change (YoY) |

Total Revenue | $2.54B | $2.19B | Beat | +16% |

EPS (Non-GAAP) | $0.95 | $0.75 | Beat | +27% |

Gross Margin | 73.2% | 73.8% | Miss | -0.6pp |

Next-Generation Security ARR | $5.6B | $4.22B | Beat | +32% |

Subscription & Support Revenue | $1.96B | $1.71B | Beat | +15% |

Product Revenue | $574M | $481M | – | +19% |

Remaining performance obligation | $15.8B | $12.7B | – | +24% |

Source: Palo Alto Networks, TradingKey

Segment and Regional Performance

Product Highlights: Next-Generation Security (NGS) ARR grew 32% YoY to $5.58 billion, beating the guidance range of $5.52 to $5.57 billion. This growth was driven by strong adoption of multi-product solutions including Secure Access Service Edge (SASE), Cortex XSIAM, and software-defined firewalls. Product revenue rose 19% to $573.9 million, fueled by a shift toward scalable, software-based firewalls and cloud-focused deployments, exemplified by a notable $60 million contract. Subscription and support revenue increased 15% to $1.96 billion, supported by demand for integrated cloud security subscriptions and new AI-powered offerings like Prisma AIRS.

Platformization Strategy: The platformization strategy is proving effective, with about 900 customers now deploying multiple Palo Alto products. This approach drove a strong 120% net retention rate, reflecting excellent cross-sell success and low churn. Expansion in the U.S. government sector, aided by new FedRAMP cloud security authorizations, improved pipeline visibility and positioned the company for growth in a highly regulated environment.

Geopolitical and Supply Chain: Direct revenue exposure to China remains limited at around 5%, reducing risk from U.S.-China trade restrictions, particularly on hardware sales. The company continues to diversify its supply chain and focus on cloud and software solutions to mitigate geopolitical risks. North America and Europe remain the main revenue drivers, supported by regulatory approvals and sustained market demand.

Financial Summary: Gross margin came in at 73.2%, mainly due to elevated investments in R&D and cloud infrastructure that support AI innovation and platform scalability. Operating expenses increased as Palo Alto fuels new product development and global expansion, yet the company delivered a non-GAAP operating margin of 30.3%, a notable achievement reflecting operational leverage and disciplined cost management. For the full fiscal year 2025, Palo Alto generated $3.51 billion in adjusted free cash flow, boasting a strong 38% free cash flow margin. This strong cash generation supports ongoing share repurchases, reinforces financial flexibility, and funds strategic initiatives including the announced CyberArk acquisition, adding scale and capability to Palo Alto’s portfolio.

Guidance and Management Commentary

Q1 FY2026 Guidance: Palo Alto Networks expects revenue of $2.45-$2.47 billion (+15% YoY), Next-Gen Security ARR of $5.82-$5.84 billion (+29% YoY), and non-GAAP EPS of $0.88-$0.90 (+13-15%).

FY2026 Guidance: Full-year revenue is projected at $10.475-$10.525 billion (+14%), Next-Gen Security ARR at $7.0-$7.1 billion (+26-27%), and non-GAAP EPS at $3.75-$3.85 (+12-15%). The company targets a 38%-39% non-GAAP free cash flow margin in FY2026.

Management Comments: CEO Nikesh Arora noted surpassing a $10 billion revenue run-rate, driven by platformization and AI. CFO Dipak Golechha highlighted strong operating efficiency and growing free cash flow, supported by deferred payments and a capital-light model.

Conclusion and Outlook

Palo Alto Networks delivered a strong Q4 FY2025, and drove robust revenue growth fueled by its AI-powered security platforms and platformization strategy. Looking ahead, the proposed CyberArk acquisition and innovations like Prisma AIRS position Palo Alto well for sustained growth, assuming effective navigation of competitive and geopolitical challenges. While the forward P/E of ~47x indicates a premium, strong free cash flow generation and market leadership offer a compelling long-term outlook. Continued government sector momentum, limited China exposure, and a deepening product portfolio further support Palo Alto’s growth prospects. Margin expansion and execution amid evolving macro conditions will be key to watch, but the company’s AI-driven platform strategy underpins a positive outlook.

.png)

Palo Alto Q4 FY2025 Earnings Preview

TradingKey - Palo Alto Networks, Inc. (NASDAQ: PANW) is slated to release its Q4 FY2025 earnings on Monday, August 18, 2025, after market close, followed by earnings call at 4:30 p.m. Eastern Time.

The stock has demonstrated robust momentum over the past year, supported by strong demand for cybersecurity solutions amid rising cyber threats in hybrid work environments and the accelerated shift towards cloud and AI-driven security platforms. Despite some margin pressure linked to investments in software and cloud transitions, PANW remains favored by investors banking on its leadership in zero-trust network security and platformization strategy. Heading into the Q4 report, shares trade with expectations of continued double-digit revenue growth, though cautious eyes remain on margins and execution risks amid industry competition and macro challenges.

Source: TradingKey

Market Forecast

Source: Palo Alto Networks, Zacks Investment Research, Yahoo Finance, TradingKey

Key Investor Focus Areas

AI-Powered Security and Platformization Growth: The company’s AI-centered offerings, including Cortex XSIAM and Prisma Cloud, are poised to continue fueling growth. The platformization approach aims to unify network, cloud, and security operations, with momentum expected to build on a strong pipeline of deals. Progress in Next-Generation Security (NGS) Annual Recurring Revenue (ARR) and expansion in multi-product engagements, particularly in Secure Access Service Edge (SASE) and software firewalls, are anticipated to be key revenue drivers in Q4 and beyond.

U.S.-China Trade Restrictions and Global Exposure: Although direct revenue exposure to China is limited (around 5%) relative to peers, U.S. export controls on advanced technology could indirectly affect supply chains and spending patterns worldwide. How trade policies are managed, and growth is sustained across North America, Europe, and other regions will influence business resilience amid ongoing geopolitical tensions.

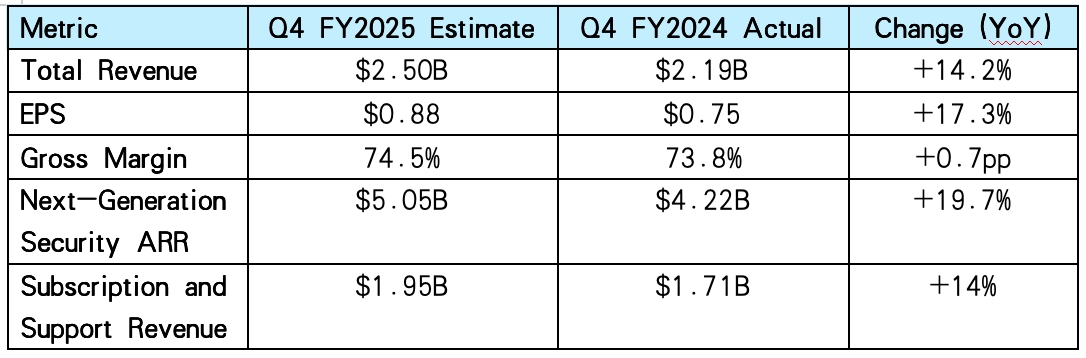

Margin Trends and Capital Allocation: The ongoing transition toward software and cloud solutions continues to exert pressure on margins due to scalability challenges and increased investment costs. However, the gross margin is expected to hold steady around 74.5% in Q4. The company’s strong cash flow generation supports active share repurchase programs and allows room for potential modest dividend increases. Capital allocation decisions, particularly regarding buybacks and balancing long-term profitability goals while funding innovation, will remain important.

Recent Developments and Regulatory Environment

Government Sector Expansion: Palo Alto Networks recently earned FedRAMP authorizations for several cloud security services, strengthening its position in the U.S. government sector. This approval enables greater adoption amid rising cyber threats and enhances regulatory compliance.

AI Innovation and Competitive Position: Advancements in AI within the Cortex suite, including automated threat detection and response, help Palo Alto address increasingly complex cyberattacks. Strategic acquisitions like IBM’s QRadar and tools such as CoPilot for automation reinforce its market leadership. Despite strong competition from cloud-native providers, Palo Alto’s comprehensive platform and loyal customer base remain key advantages.

Market Dynamics and Macro Factors: The cybersecurity market is projected to grow 15-20% annually, driven by AI, cloud adoption, and hybrid work trends. However, fluctuations in global IT spending and softer enterprise budgets may delay some large deals, potentially affecting near-term billings growth.

Trade and Supply Chain Risks: While U.S.-China trade restrictions could limit hardware sales, Palo Alto’s focus on software and cloud security limits direct exposure. The company continues to diversify its supply chain to manage potential disruptions.

Conclusion

Palo Alto Networks’ Q4 FY2025 earnings will demonstrate how effectively the company is leveraging AI-driven cybersecurity growth amid ongoing economic and geopolitical challenges. Continued strong growth in the Next-Generation Security (NGS) ARR and increased adoption of its integrated platform could drive positive market reaction if results surpass expectations. Attention will focus on margin performance and how trade-related risks are managed. With its leadership in AI-enhanced cybersecurity and platform solutions, Palo Alto Networks is positioned for sustained long-term growth, assuming it maintains disciplined cost control and successfully navigates global complexities.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.