CoreWeave’s Q2 FY2025: AI Surge Drives Record Revenue, but Profit Challenges Persist

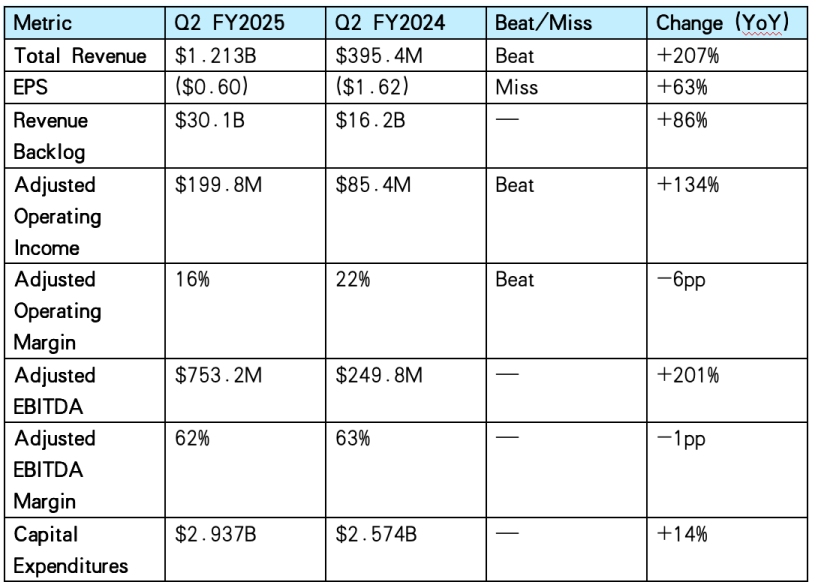

TradingKey - CoreWeave, Inc. (NASDAQ: CRWV) Q2 FY2025 earnings delivered strong revenue growth but missed earnings expectations, which led to a roughly 10% stock price drop in after-hours trading. Revenue surged 207% year-over-year, driven by robust demand for its GPU-intensive AI cloud platform.

However, the company posted a net loss of $291 million, or -$0.60 EPS, wider than the consensus forecast of -$0.20, highlighting ongoing challenges in turning rapid growth into profits. Despite this, CoreWeave’s revenue backlog expanded significantly, and the company raised its full-year revenue guidance, signaling confidence in long-term momentum amid high capital spending and acquisition integration risks.

Source: TradingView

Key Financial Results

CoreWeave’s Q2 performance was marked by exceptional revenue growth, fueled by its GPU-centric AI cloud platform and key contracts. However, significant operating expenses and interest costs, driven by aggressive infrastructure investments, contributed to a wider-than-expected net loss.

Source: CoreWeave, TradingKey

Segment and Strategic Performance

AI Cloud Platform: CoreWeave’s growth is driven by its vertically integrated, GPU-intensive AI cloud platform, with key wins including a $4 billion expansion deal with OpenAI and a new hyperscaler contract. The company reported a $30.1 billion revenue backlog, up 86% YoY, reflecting strong demand from AI labs (e.g., Cohere, Mistral), enterprises (e.g., BT Group, Woven by Toyota), and verticals like healthcare (Hippocratic AI) and media (Moonvalley). Dependence on NVIDIA for GPUs poses supply chain risks, though domestic data centers mitigate tariff concerns. The adoption of NVIDIA’s GB200 NVL72 systems and the integration of Weights & Biases’ observability tools enhanced CoreWeave’s appeal for high-performance AI workloads.

Infrastructure Expansion: CoreWeave scaled its infrastructure significantly, ending Q2 with 470 MW of active power and 2.2 GW of contracted power, up 600 MW from Q1. Capital expenditure reached a record $2.937 billion, supporting 33 data centers and plans to deliver over 900 MW by year-end. The proposed $9 billion acquisition of Core Scientific, announced in July 2025, aims to add 1.3 GW of power capacity, potentially saving $10 billion in lease costs by 2027, though integration challenges may pressure margins.

Financial Strategy: CoreWeave bolstered its balance sheet with a $2 billion senior unsecured notes offering and a landmark GPU financing deal, reducing its cost of capital by 900 basis points. CFO Nitin Agarwal emphasized robust capital market access, with plans to leverage lower-cost debt to fund $20–23 billion in 2025 capital expenditures. However, a current ratio of 0.39 and a Q2 cash decrease of $464 million highlight liquidity constraints amid heavy investment.

Guidance and Management Commentary

Q3 FY2025 Guidance: The company forecasts Q3 revenue of $1.26–$1.30 billion, adjusted operating income of $160–$190 million, and interest expenses of $350–$390 million, signaling continued investment in infrastructure to meet demand.

FY2025 Guidance: CoreWeave raised its full-year revenue guidance to $5.15–$5.35 billion from $4.9–$5.1 billion, reflecting confidence in sustained AI demand. Adjusted operating income is projected at $800–$830 million, with capital expenditures expected at $20–$23 billion.

CEO Mike Entrater stressed CoreWeave’s leading position as the AI Hyperscaler, with demand exceeding current capacity and strong growth prospects. CFO Nitin Agarwal highlighted robust customer demand but warned of margin pressure from stock-based compensation and acquisition integration costs. The company remains focused on scaling efficiently while leveraging proprietary software tools to maintain a competitive edge.

Conclusion and Outlook

CoreWeave’s Q2 FY2025 results demonstrate strong revenue growth and a significant contract backlog but ongoing margin pressure and liquidity constraints. The next steps include closely tracking the integration of Core Scientific, focusing on achieving cost synergies and controlling margin impact, while accelerating efforts to diversify the customer base beyond hyperscalers to reduce concentration risk. Maintaining disciplined capital spending is essential to preserve financial flexibility during aggressive infrastructure scaling. Growth will depend on expanding enterprise adoption and realizing acquisition benefits. Performance on these fronts over the coming quarters will determine CoreWeave’s ability to sustain growth and move toward profitability.

TradingKey - CoreWeave, Inc. (NASDAQ: CRWV) will report its Q2 FY2025 earnings on Tuesday, August 12, 2025, after the U.S. market closes. The earnings call is scheduled for 5:00 p.m. Eastern Time.

Since its IPO in March 2025 at $40 per share, CoreWeave has experienced significant volatility. The stock soared to a high of $187 in June 2025, reflecting investor enthusiasm for its AI infrastructure leadership, before sliding approximately 35% to around $121 as of August 7, 2025, amid market caution, analyst downgrades, and concerns over its proposed $9 billion acquisition of Core Scientific (CORZ).

Despite the pullback, CoreWeave trades at a relatively high forward sales multiple of 19.6x, supported by a substantial $25.9 billion revenue backlog from Q1, indicating strong confidence in long-term demand for its GPU-centric cloud platform.

Market Forecast

Metric | Q2 FY2025 Estimate | Q1 FY2025 Actual | Change (QoQ) |

Total Revenue | $1.08B | $981.6M | +10% |

EPS | ($0.20) | ($1.49) | +86% |

Adjusted Operating Income | $140M–$170M | $162.6M | -14% to +5% |

Adjusted Operating Margin | 13–15% | 17% | -2pp to -4pp |

Source: CoreWeave, Yahoo Finance, GuruFocus, TradingKey

Key Investor Focus Areas

AI Infrastructure Demand and Client Diversification: CoreWeave’s growth is fueled by its GPU-intensive cloud platform, serving major clients including OpenAI (backed by an $11.9 billion contract), Microsoft (72% of Q1 2025 revenue), Meta Platforms, and IBM. Updates on client diversification efforts to reduce concentration risk, as well as adoption of CoreWeave’s AI Object Storage (CAIOS) and NVIDIA AI Enterprise software, will be key. Broader enterprise uptake or new long-term contracts would support sustained revenue growth.

Core Scientific Acquisition Progress: Announced July 7, 2025, CoreWeave’s $9 billion all-stock acquisition of Core Scientific adds approximately 1.3 gigawatts of power capacity, significantly expanding CoreWeave’s infrastructure footprint. This deal is expected to generate up to $10 billion in cumulative lease cost savings by 2027, improving CoreWeave’s long-term cost structure. However, the integration of Core Scientific’s lower-margin colocation business is projected to compress CoreWeave’s operating margins. Progress on integration timelines, realization of synergies, and margin management will be critical to CoreWeave’s near-term financial performance and execution of its growth strategy.

CapEx and Financial Sustainability: CoreWeave plans an aggressive $20–23 billion capital expenditure for 2025 to expand its data center capacity and support AI workload demand. This is partly funded by a $2.6 billion debt facility and $1.75 billion in senior notes. The company’s current ratio stands at 0.39, indicating tight liquidity. Management projects breakeven by 2026. Monitoring cash burn, vendor terms, and interest expense remains critical to assessing CoreWeave’s balance between growth investment and financial sustainability.

Recent Events and Regulatory Trends

Strategic Acquisitions and Partnerships: Beyond the $9 billion Core Scientific deal, CoreWeave’s acquisition of Weights & Biases and a $4 billion post-Q1 contract with OpenAI highlight aggressive AI ecosystem expansion.

Regulatory and Trade Considerations: CFO Nitin Agrawal has indicated that proposed tariffs by President Trump are unlikely to materially affect operations due to CoreWeave’s reliance on domestic data centers. However, global trade uncertainties could impact GPU supply chains, notably with Nvidia as a key supplier. Supply chain resilience and diversification efforts are important to watch.

Industry Trends: The AI infrastructure market is projected to grow at 30%+ CAGR, driven by GPU-accelerated computing demand. CoreWeave’s vertically integrated model, owning power, data centers, and GPU fleets, positions it to capture significant share though competition from AWS, Google Cloud, and Microsoft Azure is intense. Key differentiators will include proprietary software like Fleet Lifecycle Controller and Tensorizer.

Conclusion

CoreWeave’s Q2 FY2025 earnings will be a key moment to gauge growth sustainability amid AI infrastructure demand. The outlook hinges on client diversification, Core Scientific integration progress, and capital expenditure management. Revenue beyond expecations and signs of broader enterprise adoption could drive upside, while margin pressure and customer concentration remain risks. The sizable revenue backlog and strong market positioning support long-term potential, but near-term volatility calls for caution.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.