U.S. Stock Sector Strategy: The Outlook for Tech Stocks from a Macro Perspective

Executive Summary

TradingKey - Against the backdrop of easing trade war tensions, sustained economic resilience, and the Federal Reserve's anticipated interest rate cuts, the U.S. stock market is expected to maintain its upward trajectory. At the sector level, we are optimistic about U.S. technology stocks, believing they are likely to outperform the broader market over the next 12 months.

At the sub-sector level, Sub-Sector One (Software): Benefiting from easing tariff tensions starting in mid-to-late April 2025, the U.S. software sector has demonstrated strong fundamental resilience in the first half of the year. Performance in cybersecurity and foundational software has been particularly standout. If macroeconomic expectations continue to improve, demand for software companies is likely to rebound further, with suppressed IT spending from the first half of the year expected to be unleashed in the second half, driving enhanced performance in this sub-sector. We recommend focusing on key stocks such as Microsoft, CrowdStrike, and Salesforce.

Sub-Sector Two (Semiconductors and Hardware): Investment opportunities in this sub-sector are primarily driven by two key trends: high growth in the AI sector and a cyclical recovery in traditional segments. We forecast that the global AI server market will experience significant growth in 2025, substantially boosting demand for semiconductors. Additionally, after two years of inventory destocking, global AI chip demand has bottomed out and is rebounding. If consumer electronics demand strengthens in the fourth quarter or progress is made in Samsung’s HBM4 certification, this sub-sector is poised for further upside. We recommend focusing on key stocks such as NVIDIA, TSMC, and Micron Technology.

Sub-Sector Three (Internet Services): Investment opportunities in this sub-sector centre on the recovery of e-commerce and online advertising, growth in cloud services, and emerging business areas. As NVIDIA’s supply chain constraints ease, computational power limitations for North American cloud giants are gradually alleviated. Coupled with the release of enterprise IT budgets following stabilised macroeconomic expectations, revenue growth for North American cloud platforms is expected to accelerate significantly in the second half of 2025. Additionally, the mature operation of Robotaxi services could reduce ride-hailing operating costs by over 50%, driving expansion in the shared mobility market. We recommend focusing on key stocks such as Alphabet, Meta, and Uber.

Sub-Sector Four (Stablecoins): The U.S. government holds a supportive attitude toward stablecoins, with its core objectives summarised in three points: first, to consolidate the U.S. dollar's global dominant position; second, to boost market demand for U.S. Treasury bonds; third, to enhance its leading voice in the cryptocurrency sector. Trump has rolled out a series of initiatives in the cryptocurrency domain, among which the Genius Act has caused significant shocks in the stablecoin market. Affected by this Act, compliant stablecoin issuers like Circle have gained capital favour due to their transparency advantages, with their stock prices surging sharply after going public. Similarly, exchanges such as Coinbase have also seen notable stock price increases driven by the surge in stablecoin trading volumes. As stablecoins continue to develop rapidly, it is recommended to focus on stocks related to Circle, Coinbase, and other relevant entities, including PayPal and Robinhood.

Source: Mitrade

1. U.S. Broad Stock Market and Technology Sector

1.1 Tariffs Eased

As trade negotiations progress positively, the U.S. stock market has shown strong performance recently, with the S&P 500 and Nasdaq indices hitting record highs. On 22 July, the U.S. secured several significant agreements with the Philippines, Indonesia, and Japan. The U.S. implemented varying degrees of tariff reductions for these three countries, while they, in turn, committed to lowering tariffs on U.S. goods, expanding investment in the U.S., and increasing purchases of American products.

On 28 July 2025, the U.S. and the EU reached a trade agreement. The U.S. set tariffs at 15% for most EU goods, a significant reduction from the previously threatened 30%. The EU committed to $600 billion in direct investments in the U.S. and pledged to procure U.S. energy products over the next three years. On 29 July 2025, U.S.-China trade negotiations concluded with both sides agreeing to extend the existing truce. The U.S. will maintain its 30% tariffs on Chinese goods, while China will keep its 10% tariffs on U.S. goods unchanged for the time being.

1.2 Earnings Improving and Capital Expenditures Increasing

Beyond the U.S.'s trade negotiations with other countries, robust corporate earnings have been a key driver of investor confidence, propelling U.S. stocks to new record highs. Among companies that have released their Q2 earnings, most have surpassed market expectations. The most eye-catching is Alphabet, one of the "Magnificent 7" tech giants, which recently reported standout second-quarter results, with both revenue and earnings per share (EPS) exceeding analyst forecasts. The company also announced a significant increase in its 2025 capital expenditure. Fuelled by this series of positive developments, the Nasdaq index reached a new all-time high.

Looking ahead, with easing trade war tensions, sustained economic resilience, and the Federal Reserve initiating an interest rate cut cycle, the U.S. stock market is expected to maintain its upward trend. At the sector level, we remain optimistic about U.S. technology stocks, anticipating they will outperform the broader market over the next 12 months. The following sections provide a detailed analysis of the growth prospects for various sub-sectors within the technology sector.

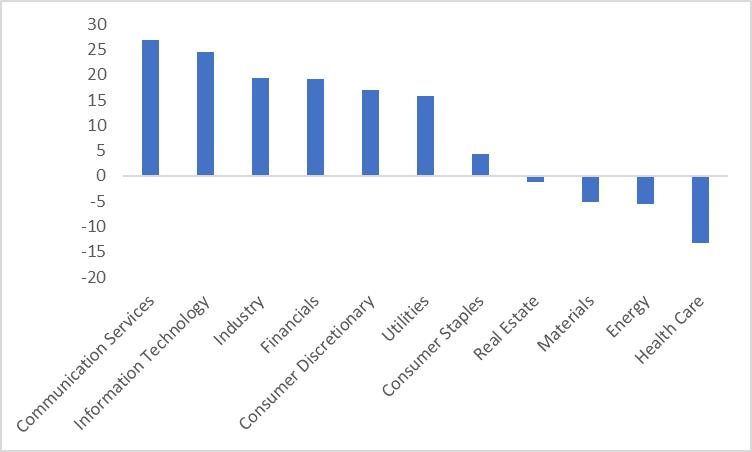

Figure 1: Performance of Sectors as of 3 August (%, 1-Year)

Source: Refinitiv, TradingKey

* For related information, refer to the article published on 29 July 2025, titled “How to Assess the U.S.-EU Tariff Deal? A Relief for European Firms, But a Slap to EU Sovereignty”

2. Sub-Sector One: Software

2.1 Strong Fundamentals

The software sub-sector is driven by both strong fundamentals and AI advancements. The easing of tariff tensions in April 2025 has provided market support. This has enabled the U.S. software sector to maintain steady growth in the first half of the year. For instance, companies like CrowdStrike and ServiceNow are projected to see continued high revenue growth in the third quarter. If macroeconomic expectations remain stable, enterprise IT spending is expected to grow by nearly 10% in the second half of 2025, driving increased demand for companies such as Microsoft and Salesforce.

2.2 AI Advancements

Based on the current progress of AI Agent development, AI’s financial contributions to U.S. software companies are expected to become increasingly evident starting in the second half of 2025, with an even more significant impact in 2026. For example, Adobe is poised for substantial growth in its Creative Cloud subscription revenue driven by AI, while Datadog is likely to see increased revenue from AI-optimised cloud monitoring in the latter half of 2025. The recovery of enterprise IT spending, the practical implementation of AI applications, and the onset of an interest rate cut cycle will collectively enhance the performance of the entire software sector.

The U.S. software sector is likely to emerge as one of the most reliable investment opportunities in the second half of 2025. Within the sub-sector, application software is expected to present significant investment prospects following the release of third-quarter earnings, with companies like Salesforce and Workday benefiting from growing enterprise digitisation needs. In the foundational software space, Microsoft and Oracle maintain strong competitive advantages through their cloud infrastructure and database services. Meanwhile, in the cybersecurity segment, escalating cyber threats are expected to keep CrowdStrike and Palo Alto Networks in the spotlight as market favourites.

3. Sub-Sector Two: Semiconductors and Hardware

Since the start of 2025, the performance of U.S. semiconductor and hardware stocks has been shaped by several key factors, including the impact of tariffs, macroeconomic expectations, advancements in AI algorithms, and progress in NVIDIA’s supply chain. Investment opportunities primarily revolve around two areas: high growth in the AI sector and the cyclical recovery of traditional segments.

3.1 High Growth in the AI Sector

Against the backdrop of rapid AI growth, taking the GPU sector as an example, the market previously rotated along the AI value chain—from software and data to applications (e.g., Palantir Technologies). However, following the disruption caused by DeepSeek, the industry has advanced to a new phase. The market focus has shifted back to hardware (e.g., NVIDIA), forming a new cycle with heightened market enthusiasm.

Additionally, we forecast that the global AI server market will experience significant growth in 2025, substantially boosting demand for semiconductors. Improvements in the yield rates of NVIDIA’s downstream rack assembly have enhanced supply chain efficiency, while AI ASIC shipments are rapidly increasing, serving as a key source of medium-term investment opportunities. This trend is expected to benefit the following areas:

· ASIC Chips: AMD’s MI300 series AI chips are projected to achieve significant revenue growth in the second half of 2025. Meanwhile, AMD's cyclical CPU business has also shown a positive trend.

· HBM Chips: As an anti-cyclical HBM chip, Micron Technology is expected to benefit from strong demand for HBM3.

· AI Networking Equipment: Cisco is expanding its market share with AI-optimised networking solutions.

· Advanced Process Foundry: TSMC’s CoWoS packaging capacity is anticipated to double in 2025.

· Server ODM: Quanta Computer, a key NVIDIA partner, will see gains from increased AI server orders.

3.2 Cyclical Recovery of Traditional Segments

Starting in Q1 2025, global semiconductor inventories have gradually normalised. Limited new production capacity, coupled with increased precautionary stockpiling, has tightened the supply-demand dynamics for memory chips since Q2, driving price increases. This price upcycle is expected to persist at least through Q3. For instance, Micron Technology is poised for significant revenue growth in 2025 due to rising prices for its DRAM and NAND chips. Following two years of inventory destocking, global AI chips have bottomed out and are rebounding. Should consumer electronics demand recover in Q4 or Samsung achieve progress in HBM4 certification, related stocks are likely to see further upside.

Overall, the high growth in the AI sector and the cyclical recovery of traditional segments present significant investment opportunities for the semiconductor and hardware sub-sectors in the second half of 2025. We recommend focusing on companies such as NVIDIA, TSMC, Micron Technology, AMD, Cisco, Texas Instruments, and Qualcomm. However, investors should remain vigilant of potential risks stemming from tariff policies and supply chain bottlenecks.

4. Sub-Sector Three: Internet Services

Since 2025, tariff policies, macroeconomic expectations, NVIDIA’s supply chain developments, and the growth of emerging business areas have been key drivers of stock performance in the U.S. e-commerce, cloud services, and related sectors. Investment opportunities primarily focus on the recovery of e-commerce and online advertising, the expansion of cloud services, and emerging business segments.

4.1 Recovery of E-Commerce and Online Advertising

Due to tariff-related volatility, the U.S. e-commerce and online advertising sub-sector experienced a brief decline in April 2025, with significant drops in the stock prices of companies like Amazon and Meta. However, starting in May, the market quickly rebounded, with Amazon reporting notable e-commerce revenue growth and Meta seeing substantial increases in advertising revenue in Q2. From Q3 onward, improving macroeconomic expectations, coupled with supportive fiscal policies and accommodative monetary measures, are expected to be key drivers, providing a favourable environment for leading companies such as Amazon, Meta, and Alphabet.

4.2 Expansion of Cloud Services

Improvements in NVIDIA’s supply chain, particularly the enhancement of U.S. domestic chip production capacity, have gradually alleviated computational power constraints for North American cloud giants like Microsoft and Amazon’s AWS. Combined with the release of enterprise IT budgets following stabilised macroeconomic expectations, revenue growth for North American cloud platforms is expected to accelerate significantly in the second half of 2025. For instance, Microsoft Azure and Amazon AWS are projected to achieve year-over-year revenue growth of 20%-30% in Q4. Additionally, Google Cloud is steadily expanding its market share through AI-optimised services.

4.3 Emerging Business Segments

Since 2025, the development of Robotaxi has accelerated significantly, with positive progress made in both core algorithm technologies and industrial policy supervision. In the second quarter of 2025, the test mileage of Tesla's Robotaxi increased substantially, and Waymo, a subsidiary of Google, obtained a fully autonomous driving license in California. Once Robotaxi operations mature, it is expected to reduce the capacity cost of ride-hailing services by more than 50%, thereby stimulating the expansion of the shared mobility market. This continues to benefit platform-based companies such as Uber.

In 2025, investment opportunities in U.S. stock sectors such as e-commerce, cloud services and emerging businesses will be prominent, driven by tariffs, macroeconomic expectations and technological advancements. It is recommended to pay attention to Alphabet, Meta, Amazon, and Uber.

5. Sub-Sector Four: Stablecoins in the Cryptocurrency Space

5.1 Goals of U.S. Government Backing for Stablecoins

The U.S. government’s endorsement of stablecoins centres on three key goals: first, to maintain the U.S. dollar’s global prominence; second, to increase demand for U.S. Treasury securities; and third, to assert greater authority in the cryptocurrency domain. Specifically, as global “de-dollarisation” trends gain traction, the dollar’s peg to most stablecoins helps bolster its international role. Additionally, short-term U.S. Treasuries form a significant portion of stablecoin reserve assets. Bessent forecasts an eightfold expansion of the stablecoin market by 2028, which could drive demand for short-term Treasuries past $1 trillion, significantly boosting the Treasury market. Moreover, with growing demand for cryptocurrencies and continuous innovation in related technologies, the U.S. government is adopting a proactive stance by regulating and embracing cryptocurrencies. This strategy aims to establish a strong presence in this emerging sector, safeguard the dollar’s status as the world’s reserve currency, and enhance U.S. leadership in the crypto industry.

5.2 The GENIUS Act

Trump has taken bold steps in the cryptocurrency arena. In January, he championed the Enhancing U.S. Dominance in Digital Finance Act. By March, he integrated confiscated Bitcoin into the U.S. Strategic Crypto Reserve. The GENIUS Act, however, has caused the most significant ripples in the stablecoin market, with lasting implications for related U.S. market sectors and stocks. Notably, regulated stablecoin issuers like Circle have attracted significant investor interest due to their transparency, resulting in sharp stock price gains after going public. Likewise, platforms like Coinbase have enjoyed substantial stock price increases fuelled by booming stablecoin trading volumes. Although these stocks might face short-term consolidation or corrections following their rapid climbs, the projected sustained growth of the stablecoin market should continue to bolster Circle and Coinbase in the medium to long term. As stablecoins maintain their rapid expansion, other connected stocks, including PayPal and Robinhood, are also worth watching.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.