Eli Lilly’s Q2 2025 Triumph: Soaring Revenue, Plunging Stock – What’s Behind the Paradox?

Eli Lilly FY2025 Second Quarter Earnings Comment

TradingKey - Eli Lilly released its Q2 2025 financial results, demonstrating impressive financial performance. However, despite the stellar results, its stock price plummeted by over 14%, closing at approximately $640, down more than 30% from its yearly high. Below is an in-depth analysis of the earnings report:

Earnings Highlight

Revenue: Eli Lilly’s total revenue for Q2 2025 reached $15.6 billion, surpassing market expectations of $15.0 billion, reflecting a 38% year-over-year increase (compared to $11.3 billion in Q2 2024). This growth was primarily driven by robust demand for core products Mounjaro and Zepbound, underscoring the company’s leadership in diabetes and weight-loss therapies.

Earnings Per Share (EPS): Adjusted EPS was $6.31, up over 60% year-over-year, exceeding market expectations. The gross margin improved from 80.8% in the same period last year to 84.3%, a 3.5 percentage point increase, indicating the company’s success in optimizing production costs and enhancing its product mix, thereby boosting profitability.

Core Product Performance

Mounjaro

Mounjaro (tirzepatide), Eli Lilly’s flagship product, saw global revenue surge by 68% to $5.2 billion. In the U.S. market, revenue reached $3.3 billion, up 37%, while international revenue soared from $680 million in the prior year to $1.9 billion, driven by volume growth and expansion into emerging markets such as Mexico and Brazil.

Despite strong demand, Mounjaro’s realized price in the U.S. market declined, partially offsetting the contribution of volume growth. This may reflect strategic pricing adjustments or increased rebates to ensure market access and competitive advantage. The rapid growth in international markets was fueled by strong demand for GLP-1 therapies, demonstrating Eli Lilly’s success in diversifying revenue streams through a global strategy, reducing reliance on the U.S. market and enhancing revenue resilience.

Zepbound

Zepbound’s performance in the U.S. market was particularly outstanding, with revenue surging 172% to $3.38 billion (compared to $1.24 billion in Q2 2024). This growth was primarily driven by soaring demand, though it was also constrained by a decline in realized prices. The price adjustment likely aimed to increase market penetration, particularly for self-pay patients or those with limited insurance coverage. However, not being included in the CVS formulary poses a challenge to short-term sales growth, increasing market uncertainty.

Verzenio

Verzenio’s global revenue grew 12% to $1.49 billion, with U.S. growth at 8% and international growth at 19%, driven by volume increases. Verzenio maintained its leading position in the U.S. breast cancer treatment market, with strong international performance further solidifying its global competitiveness.

Other Key Drug Performance

Trulicity: Revenue of $1.09 billion, down 12% year-over-year, reflecting intensified competition in the GLP-1 drug market squeezing its market share.

Jardiance: Revenue of $690 million, down 10%, facing similar market pressures.

Taltz: Revenue of $848 million, up 3%, showing stable performance.

Emerging Drugs: Jaypirca ($123 million, up 34%), Omvoh ($75 million), Ebglyss ($87 million), and Kisunla ($49 million) demonstrated early growth potential, laying the foundation for future revenue diversification.

Geographical Performance

U.S. Market

U.S. revenue grew 38% to $10.81 billion, with volume growth of 46%, primarily driven by Mounjaro and Zepbound. However, realized prices fell 8%, reflecting intense pricing competition and pressure from payer negotiations in the U.S. market.

International Market

International revenue increased 37% to $4.74 billion, with volume growth of 35% and a 3% favorable foreign exchange impact. Mounjaro was the core driver of international growth, with realized prices declining only 1%, indicating a relatively lenient pricing environment. Expansion into emerging markets (e.g., Mexico and Brazil) and targeted strategies in underserved markets highlighted the success of Eli Lilly’s global strategy. This approach not only reduced reliance on the U.S. market but also provided new growth engines through rapidly expanding international markets.

Future Outlook

Eli Lilly’s stock price decline was driven by investor disappointment with the Phase III trial results for its oral obesity drug orforglipron, which showed a weight loss rate of 12.4%, slightly below Novo Nordisk’s injectable semaglutide at 13.7%. Nevertheless, Eli Lilly’s management expressed strong confidence in the company’s future, raising its full-year 2025 revenue guidance to $60.0–$62.0 billion, up from the previous range of $58.0–$61.0 billion. Similarly, full-year EPS guidance was raised from $20.78–$22.28 to $21.75–$23.00. This adjustment reflects management’s confidence in the sustained dominance of Mounjaro and Zepbound in the GLP-1 market and the potential for future indication expansions for tirzepatide.

Currently, oral GLP-1 drugs (such as Orforglipron) remain positioned as a supplementary category in the obesity treatment field, while injectable GLP-1 drugs (such as Mounjaro and Zepbound) continue to dominate the market. Oral drugs attract specific consumer groups by improving accessibility, but their profit contribution may be limited due to lower pricing expectations, and clinical trials show their weight-loss efficacy is not yet comparable to injectable drugs. In contrast, Eli Lilly’s strong performance in the injectable GLP-1 market has significantly squeezed Novo Nordisk’s market share. Over the past three years, Novo Nordisk has shown a declining trend in both market competition and stock performance, highlighting the “seesaw effect” in the GLP-1 market. The current competitive landscape has limited long-term impact on Eli Lilly, which continues to maintain a competitive edge in the GLP-1 field, supported by its robust product pipeline and superior market execution.

Overall, Eli Lilly delivered outstanding financial performance driven by the strong performance of Mounjaro and Zepbound, volume growth, and operational efficiency improvements. Despite the short-term stock price correction triggered by orforglipron’s Phase III data, management’s upward revision of revenue and EPS guidance reflects confidence in long-term growth. By maximizing the potential of GLP-1 drugs, accelerating global expansion, investing in oral GLP-1 and cutting-edge fields like gene editing, and optimizing pricing and supply chains, Eli Lilly is executing a multidimensional growth strategy. Despite risks from FDA approvals and competition from compounded drug companies, Eli Lilly’s robust product portfolio and sound strategy solidify its leadership in the GLP-1 market, with strong long-term potential.

Eli Lilly FY2025 Second Quarter Earnings Preview

Market Expectations

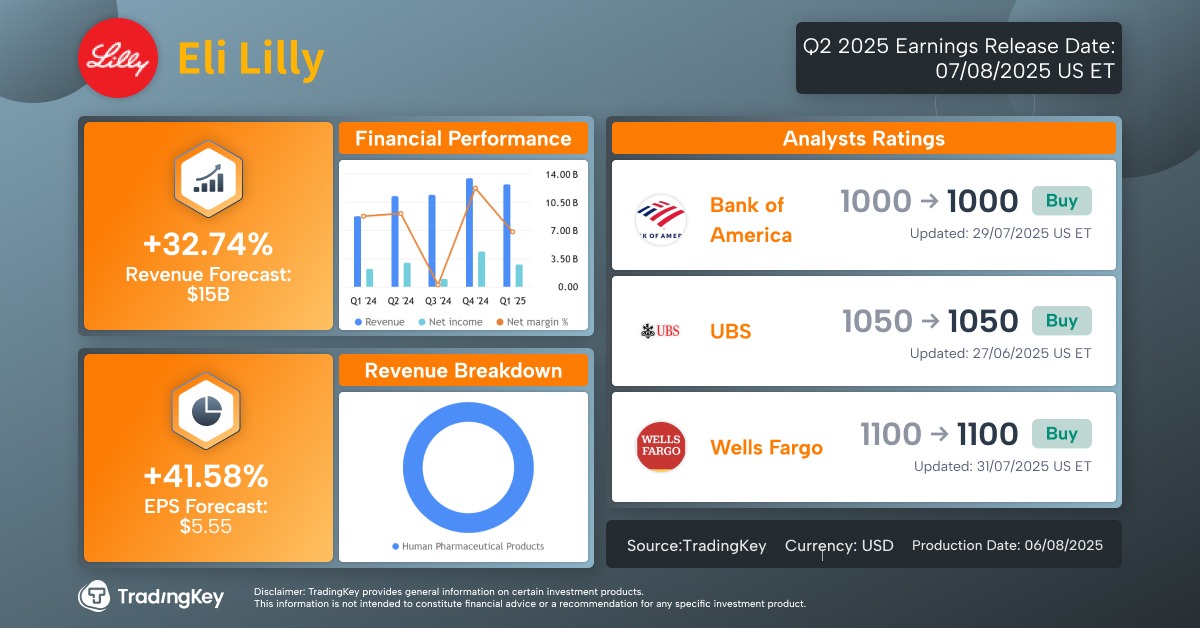

TradingKey - Eli Lilly’s Q2 2025 earnings report is expected to be released before the U.S. stock market opens on August 7. Below are the market expectations for Eli Lilly’s Q2 2025 revenue and earnings per share (EPS):

· Revenue Expectation: Eli Lilly’s total revenue for Q2 2025 is projected to reach $15 billion, representing an approximate 33% increase compared to $11.3 billion in Q2 2024. This reflects continued strong growth in demand for the company’s key products in the second quarter, particularly the weight-loss drug Zepbound and the diabetes drug Mounjaro.

· EPS Expectation: Eli Lilly’s earnings per share (EPS) for Q2 2025 is expected to be $5.55, a significant increase of nearly 42% compared to $3.92 in Q2 2024.

Key Investor Focus Areas

Key Drug Sales Performance: Mounjaro and Zepbound are the core drivers of Eli Lilly’s revenue growth, with GLP-1 receptor agonist drugs performing strongly in the diabetes and weight-loss markets. In Q1 2025, their sales reached $3.84 billion and $2.31 billion, respectively, accounting for nearly half of total revenue. Investors should focus on whether Mounjaro and Zepbound sales in Q2 meet or exceed expectations, particularly in the U.S. market amid competition with Novo Nordisk’s Wegovy and Ozempic, and whether demand sustains the 45% robust growth trend from Q1.

Production Capacity and Supply Chain Updates: Eli Lilly has previously faced supply chain challenges with Mounjaro and Zepbound production, impacting sales momentum. Investors should pay attention to whether new production facilities have come online and whether the company can meet global demand. Updates on production expansion or supply chain improvements will directly affect growth prospects for the coming quarters.

Pipeline Progress: The company’s research pipeline is critical to long-term growth. Investors should particularly focus on the progress of Phase 3 trials for the oral GLP-1 receptor agonist orforglipron and the multi-receptor agonist retatrutide. Positive trial results in 2025 could serve as significant catalysts for stock price growth.

Competition: Eli Lilly faces intense competition in the weight-loss and diabetes drug markets from rivals like Novo Nordisk. Investors should monitor how the company strengthens its market share, as well as management’s commentary on pricing strategies and market trends.

Tariffs and External Factors: The Trump administration may impose tariffs on imported drugs, and Eli Lilly mentioned in its Q1 2025 earnings report that this risk could impact its financial outlook. Investors should focus on the company’s response strategies, such as increased investment in U.S. production, and the potential impact of tariffs on international market revenue.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.