The Dilemma of Investing in U.S. Stocks: Will You Ride the Bubble or Risk Missing Out?

TradingKey - Since Nvidia became the first company worldwide to surpass a $4 trillion market capitalization, its shares have continued to climb, rising more than 9% over several trading sessions. This momentum has propelled the S&P 500 and Nasdaq indices to consecutive record highs. As earnings season unfolds, major U.S. companies have been reporting their quarterly results, with the widely watched Big Seven showing an increasingly pronounced divergence in performance this quarter.

This divergence marks a clear split of the Big Seven

The current performance of the “Magnificent 7” can be summarized as a tiered pattern: three strong, two steady, and two weak. (for detailed stock reports, please refer to TradingKey analysis; the following is a brief summary):

- Nvidia: Expected to sustain strong growth and exceed market expectations this quarter, buoyed by TSMC’s exceptionally strong performance and robust capital expenditure plans across the broader technology sector.

- Google: Continues to outperform market expectations, driven by rapid growth in advertising and cloud services.

- Tesla: Stands out as this fiscal year's underperformer, with auto sales plunging amid political headwinds and intense price competition from Chinese EV makers. However, its ventures into robotics, autonomous driving, and new low-cost models represent long-term growth potential.

- Facebook: Surprised again this quarter, with limited tariff impact. Strong growth in advertising revenue notably boosted its results.

- Microsoft: Cloud segment grew rapidly, fueled by AI advancements that have driven significant enterprise demand for Azure AI.

- Apple: Experienced a short-term surge in iPhone demand in emerging markets due to tariff-related uncertainties; however, these tariffs are also weighing on the company’s gross margins.

- Amazon: Retail and advertising revenues posted strong results, but its closely watched AWS cloud division saw profits slightly miss expectations due to rising expense ratios.

Data Sources: Reuters, TradingKey As of: July 31, 2025

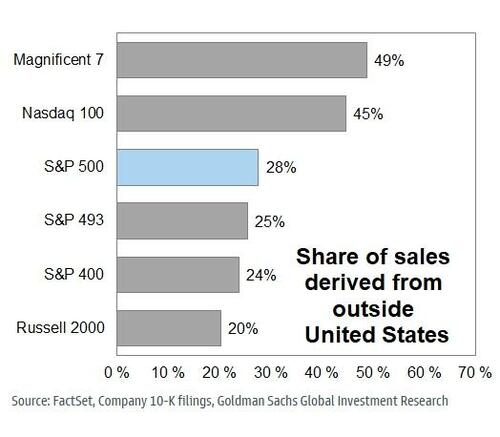

Beyond these company-specific factors, the rapid depreciation of the U.S. dollar this quarter has both enhanced the competitiveness of American goods and services abroad and improved the conversion of foreign currency revenue into U.S. dollar earnings. Data shows that for every 1% decline in the dollar, the earnings per share growth rate of S&P 500 constituents increases by about 0.6 percentage points. This dynamic has indirectly contributed to the generally positive earnings reports among the tech giants this quarter.

Data Sources: Goldman Sachs, TradingKey As of: July 31, 2025

The earnings each company reported are also reflected in their respective valuations. For example, Google and Facebook, which significantly beat market expectations this quarter, show a reasonable alignment between their forward P/E ratios and expected future growth, making their valuations appear justified. However, for several other tech giants, P/E ratios exceeding 30 times — and in some cases even 100 times — on such massive market capitalizations suggest investors may be overly optimistic about their future prospects.

Artificial Intelligence Faces Potential Short-Term Bottlenecks

The global investment market is currently saturated with bullish sentiment and optimism toward technology and artificial intelligence (AI). In fact, institutional investors who fail to allocate capital to AI-related sectors or companies risk being labeled as “uninformed.” This phenomenon is not confined to U.S. market, but is also evident across China, Singapore, and most other active markets worldwide.

While it is undeniable that AI technology could become a transformative tool to significantly boost human productivity — often regarded as the “fourth industrial revolution” — there remains a critical caveat. At present, only a handful of leading companies worldwide are poised to capture meaningful profit growth from AI advancements; the majority of firms and individuals still merely serve as “nutrient providers” feeding the ecosystem.

1. High Barriers to Technology and Capital Access

Currently, only a handful of global tech giants have the capacity to develop large-scale AI models, while local deployment remains prohibitively expensive for most companies and individuals. Advancing AI technology requires vast amounts of high-end inference chips and significantly increased power consumption. Yet, investing hundreds of millions in capital addresses only one piece of the puzzle — computing power. Beyond this, algorithms and data are two other critical factors influencing AI effectiveness. For instance, Deepseek has optimized algorithms to achieve ChatGPT-level functionality at a lower computing cost. A new challenge now is that much of the historically available effective data may already have been used to train large models, raising concerns about a future shortage of quality data for AI training.

2. Closed-Source Monopolies Hinder Technology Diffusion

Past industrial revolutions were characterized by widespread adoption and diffusion of new technologies. By contrast, U.S. AI development has gradually shifted from open-source collaboration to closed-source monopolization. This shift is driven partly by leading firms’ commercial imperatives and the need to recoup investments. It is also propelled by government-imposed competitive barriers.

Technology competition stands as a central battleground in the ongoing U.S.-China rivalry, with neither side willing to concede defeat. Measures such as restricting chip sales to China and closing off large-model communities inhibit Chinese challengers but also sharply limit the broader dissemination of AI technologies. This, in turn, indirectly increases per-unit training costs and slows industry-wide progress.

3. Structural Unemployment Risks

More companies and individuals are harnessing large AI models to improve work and learning efficiency. Yet as machine learning advances, anxieties around job displacement are intensifying. This fear is already materializing in major tech firms; Microsoft, for example, announced plans to cut nearly 15,000 jobs this year alone. The mantra of “invest in AI, reduce headcount” has become more than a slogan.

Although new technologies ultimately generate fresh employment opportunities, each industrial revolution has triggered waves of short-term, large-scale unemployment. These structural job losses disproportionately affect workers unable to adapt or whose skills mismatch evolving demands. Moreover, such disruptions have significant negative repercussions on local economies.

The Stock Market Has Officially Entered Into a Bubble Phase

That said, this is not to dismiss the vast future potential of artificial intelligence technology. On the contrary, we are highly optimistic and firmly believe AI will reshape industries, significantly boost human productivity, and ultimately transform lifestyles. However, there is no denying that the current extreme optimism around AI, combined with the tech-driven momentum in capital markets, has pushed the U.S. stock market into a bona fide bubble.

.jpg)

Data Sources: Reuters, TradingKey As of: July 31, 2025

First, the technology sector’s weighting in the S&P 500 has surged back to levels approaching the peak of the 2000 dot-com bubble.

.jpg)

Data Sources: CurrentMarketValuation, TradingKey As of: July 31, 2025

Second, the Buffett Indicator makes it clear that U.S. equity valuations are more than two standard deviations above the mean. In over 70 years of data, this threshold has only been breached three times before, with each episode lasting fewer than two months.

.jpg)

.jpg)

Data Sources: CurrentMarketValuation, TradingKey As of: July 31, 2025

From a valuation perspective, both the P/E ratio and P/S ratio for the S&P 500 currently stand above the +2 standard deviation mark. Aside from the few major tech giants, many smaller-cap stocks are trading near historic highs.

Data Sources: CurrentMarketValuation, TradingKey As of: July 31, 2025

The current spread on high-yield (junk) bonds is at an all-time low, illustrating elevated investor risk appetite despite diminishing returns.

.jpg)

Data Sources: CurrentMarketValuation, TradingKey As of: July 31, 2025

Finally, the well-known “Sam Rule,” a leading indicator for economic recessions, signals caution. This rule is triggered when the three-month moving average of the unemployment rate rises by at least 0.5 percentage points above its lowest level in the past 12 months. Historically, it has accurately and promptly predicted U.S. recessions. At present, the index has climbed to 0.4%, inching closer to that critical threshold.

Epilogue

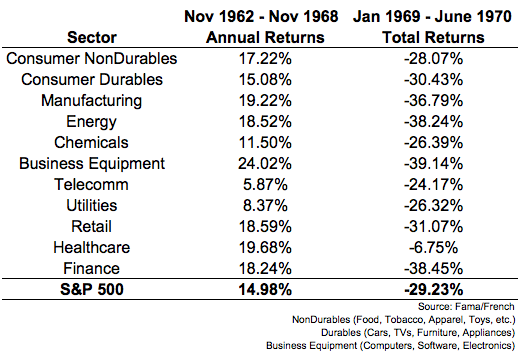

In 1969, Warren Buffett wrote to his partners announcing the decision to close his partnership fund. At the time, the U.S. stock market was deep into the famed “Go-Go Era,” a period marked by rampant speculation and concept-driven frenzy.

Data Sources: Fama/French, TradingKey As of: July 31, 2025

Coincidentally, since 2022, Berkshire Hathaway has been a net seller of stocks for 11 consecutive quarters, hoarding significant cash reserves. Yet, despite this cautious stance, the three major U.S. indexes have continued to push to new highs amid mounting pressures from various fronts. Investors repeatedly tell themselves, “This time is different,” and institutional investors often choose to shoulder enormous bubble risk rather than face the anxiety of missing out.

While it is impossible to predict market turning points with precision — and there is a strong possibility that the U.S. market’s rally may persist — the lesson remains clear: history may not repeat itself exactly, but it often rhymes.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.